- TACO is backo. The world got a taste of “Greenlandic tacos” this week as Trump backed away from his threatened European tariffs after agreeing to what he called “the framework of a future deal” with NATO’s secretary‑general.

- Vol pops and drops. Even though no details of the deal have been released, the latest bout of nerves now sits firmly in the rear‑view mirror, with the VIX completing a neat roundtrip from 16 to 20 and back again, underscoring how quickly sentiment and volatility has stabilised.

- The JGB lesson. One development that may leave a more lasting imprint on the investment landscape was this week’s meltdown in Japanese government bonds (JGBs). The large sell-off in JGBs dragged global bond markets lower on the back of pre-election fiscal giveaways.

- Haven halo. Despite cooling risk aversion, the Swiss franc held onto its gains, emerging as the clear standout safe‑haven hedge against geopolitical risk.

- Aussie rules, yen drools. JPY remains one of the weakest performers, sitting near record lows versus the euro and pound. By contrast, AUD and NZD continue to lead G10 gains this year, helped by their geopolitical insulation and steadier fiscal outlooks, with AUD/USD hitting its highest since October 2024.

- Fed in focus. The USD has tracked the relief rally in risk assets, but the dollar index is still on course for its first weekly decline of 2026. That comes ahead of an upcoming politically charged Fed meeting, where we don’t expect a rate cut.

Global Macro

Relentless bid

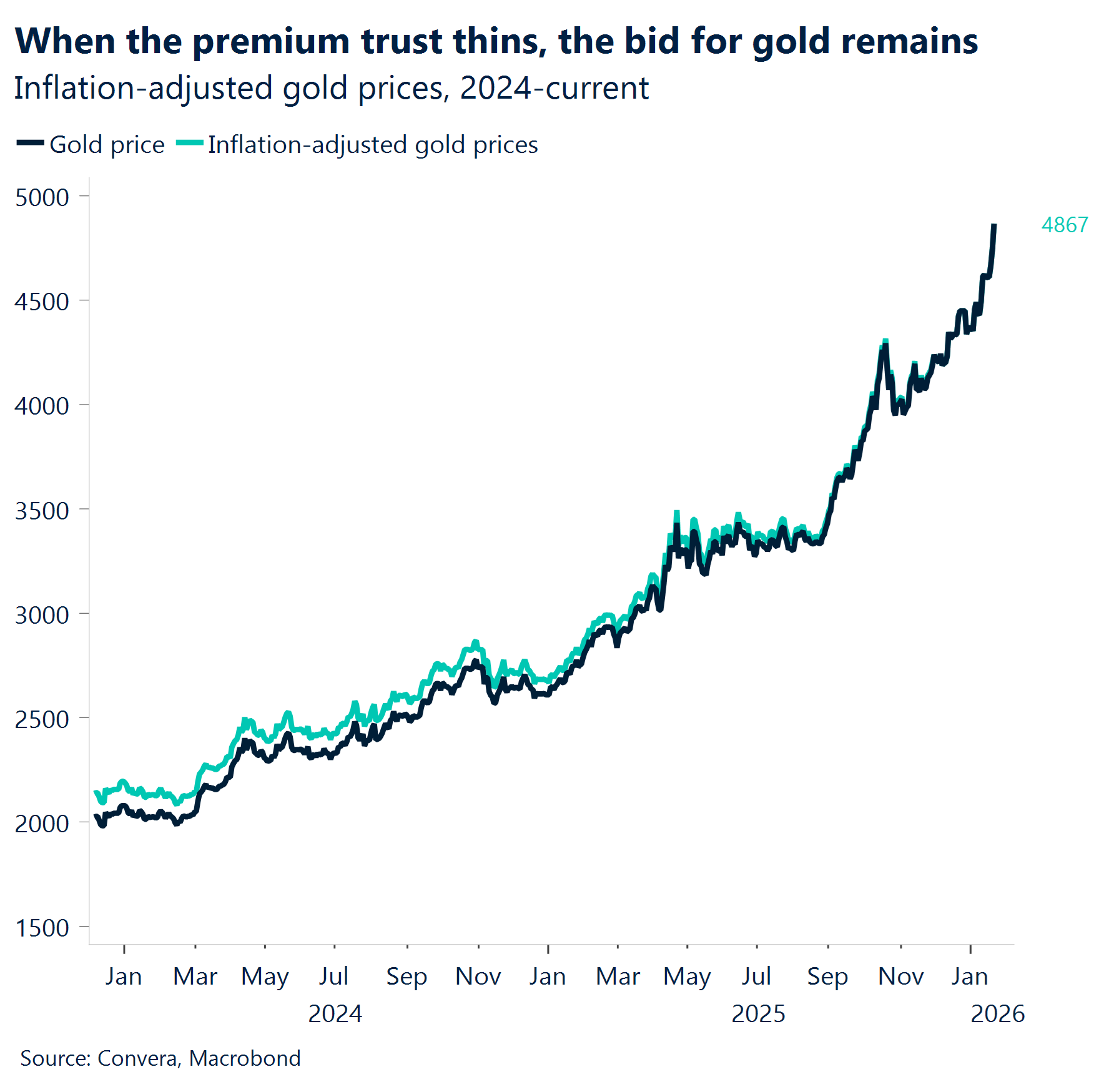

In Gold we trust. Three full trading weeks into the year, and in the middle of significant geopolitical turbulence, Gold continues its record-breaking run, climbing nearly 13% year-to-date to hit fresh all-time highs. $5,000/oz looks just around the corner.

“Goldilocks“ economy continues. US Q3 growth final reading came up at 4.4%. Growth was the strongest in two years, led by consumer spending and AI-sector investments.

“Low-hire, low-fire“. US Initial Jobless Claims came at 200K vs 210K expected. This Reinforces a “low-hiring, low-firing” labor market that remains disconnected from surprising growth.

CPI week. Sterling jumped initially on the hotter-than-expected headline. Gains were capped as core inflation remained stable at 3.2%, suggesting the BoE may stay on hold. In Canada, while the headline number came up hotter, the CAD saw limited gains because core measures (Trim/Median) actually cooled. It was viewed as a “messy” print distorted by base effects. In Europe, inflation fell below the ECB’s 2% target for the first time since mid-2025.

Tariffs. No SCOTUS decision on IEEPA tariffs. Decision has been postponed until late next week/early February. In Davos, after another tariff scare and pivot, President Trump and European leaders are working on a framework deal around increased defense in Greenland and the arctic.

Week ahead

Policy pause expected

Steady Fed in focus. Next week the first Fed policy meeting of the year will take place. Markets expect a steady Fed, leaving the policy corridor unchanged at 3.50–3.75%. Data releases have returned to a normal rhythm after the shutdown‑related disruptions, and investors are beginning to form a more unified view of the US economy: the labour market remains soft but shows no further deterioration, economic activity is firm, and inflation is benign.

AI tailwinds for disinflation. On the inflation front, there is growing discussion about rising productivity and falling unit labour costs in the US, largely linked to AI adoption, and their role in easing inflation pressures. Upcoming final releases on these themes will therefore be closely scrutinised.

Eurozone Q4 check-up. With early signs and high expectations that the eurozone may face a brighter economic outlook in 2026, attention will turn to the preliminary Q4 GDP estimates for France, Germany and the eurozone to gauge how the bloc exits 2025 and enters the new year.

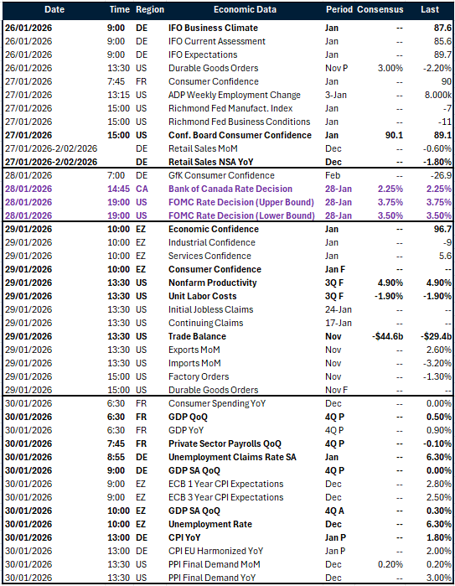

Confidence gauges on deck. Several sentiment indicators – the IFO Business Climate for Germany, the Conference Board Consumer Confidence for the US, and the European Commission’s sentiment surveys for the eurozone – will also be in focus as we assess different stakeholders’ views – from consumers to business owners – at the onset of 2026.

FX Views

Geopolitics steal the spotlight

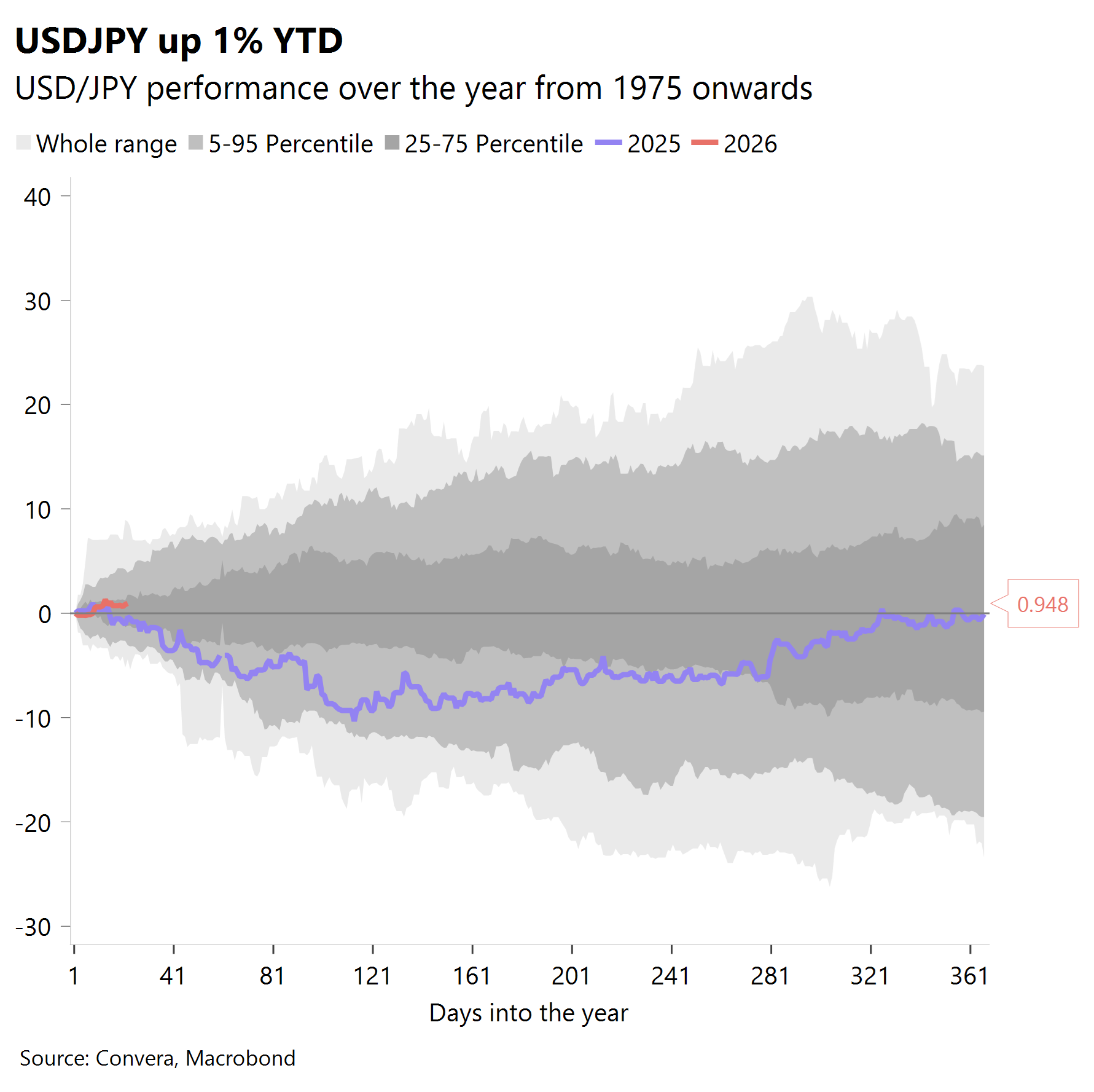

USD Hit by geopolitics. The dollar index (DXY) heads toward the week’s close almost 1% lower, reversing earlier‑month gains and leaving it only 0.1% higher month to date. The cautious bullish narrative building for the greenback, supported by positive January seasonality and a resilient macro backdrop, ran into sentiment‑driven selling as geopolitical tensions flared, with President Trump threatening tariffs on eight European economies that opposed his attempts to assert authority over Greenland. The sharp escalation, amplified by a more forceful European response, revived sell‑America fears and triggered broad selling across the dollar, US equities and Treasuries. A swift de‑escalation followed, with an apparent framework for a deal secured that helped calm markets. Yet the dollar struggled to shake off the geopolitical risk, closing lower for a third day on Thursday. As the Fed meeting approaches next week, and with data this week pointing to a strong macro backdrop alongside still‑elevated inflation, we expect the dollar to pare back some of its geopolitically driven losses.

EUR Setup still fragile. EUR/USD is ending the week just above 1% higher, lifted by renewed euro demand as geopolitical tensions around Greenland pressured the dollar. Aside from the undisputed winner in such risk‑off environments, the Swiss franc, the euro continues to benefit when the risk‑off is US‑centric and triggers de‑dollarization concerns, positioning the common currency as the second‑best alternative. Before this flare‑up, however, the pair was leaning bearish, trading near the 200‑day moving average and seeing hedge‑fund positioning turn negative for the first time since November. A poorly negotiated outcome on Greenland could quickly revive that setup, sending the euro lower on softer sentiment tied to a cornered Europe with limited bargaining power, echoing July’s trade‑deal dynamics. For now, the familiar 1.15–1.18 range still holds, and without a more dovish Fed, sentiment‑driven dollar selling alone looks insufficient to fuel a sustained break above resistance. The base case remains a return to the 1.16 handle as macro dynamics re-gain influence and geopolitical risk continues to diffuse.

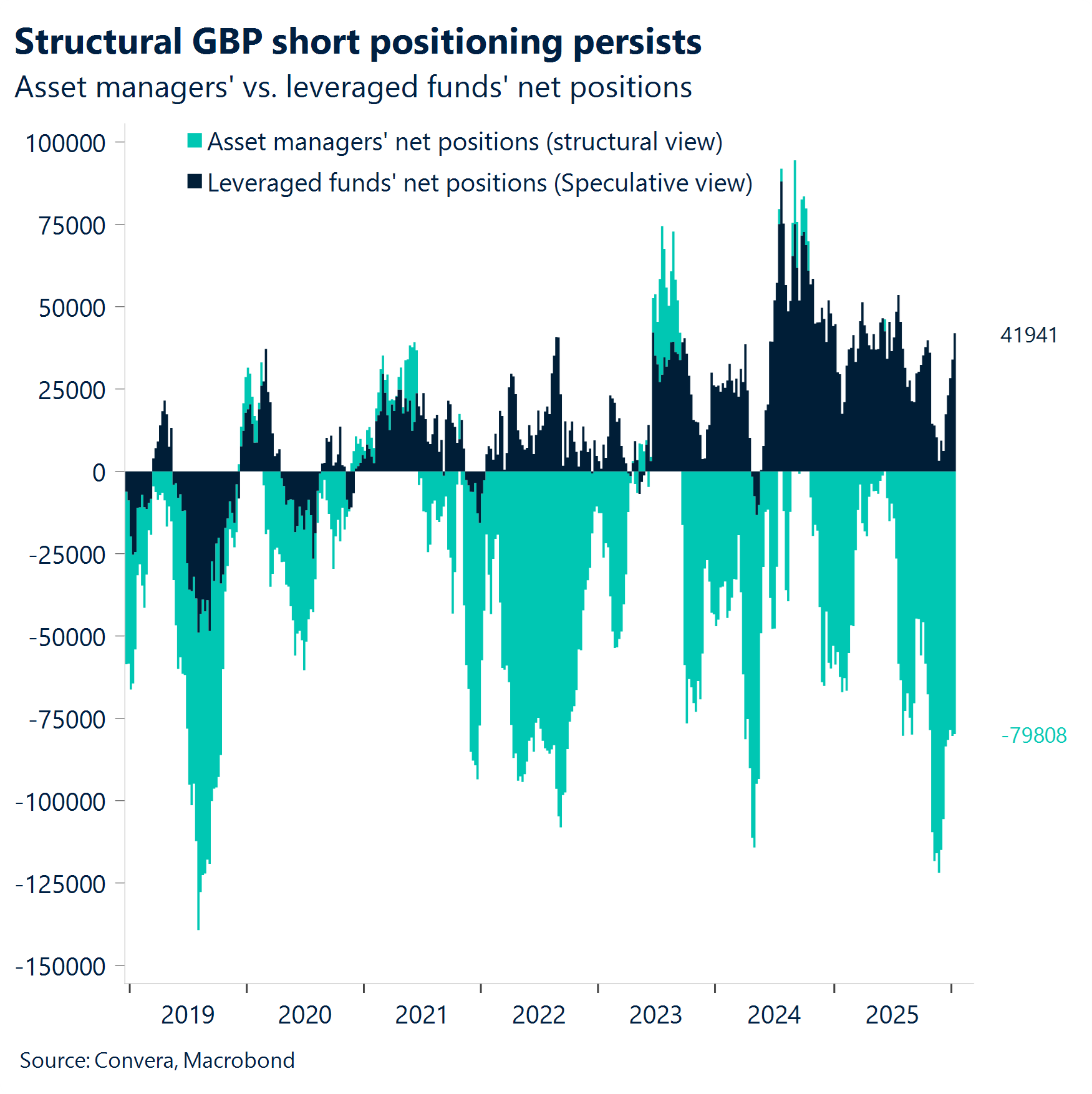

GBP Macro gloom eases. Sterling spent the week trading at the mercy of shifting global risk sentiment and dollar dynamics. The dollar’s tone flipped from cyclical bull to something closer to a structural bear as geopolitics revived USD sellers — at least temporarily — bringing the $1.35 handle into view. GBP/USD has scored its first weekly rise of 2026 and is trading above all of its key daily moving averages in a sign that momentum is shifting favourbly for the pound. True, the UK domestic backdrop is anything but desirable, but markets may be leaning too far into pessimism. With inflation cooling and rate cuts approaching, there is room for a surprise rebound in aggregate demand and stronger growth in the second half of the year (if the labour market steadies). That raises the risk that relative growth differentials ultimately prove more supportive for the pound than currently assumed. Positioning also matters: asset‑manager shorts reached a five‑year extreme ahead of the November budget and have since been steadily unwound. Underweight exposure still dominates, but that asymmetry now works in sterling’s favour, offering a positioning tailwind should sentiment turn.

CHF The Alpine anchor. The Swiss franc has been one the standout performers of late as it emerged the preferred safe‑haven hedge against geopolitical risks. Switzerland’s exemption from the list of European nations that faced potential US tariffs reinforced the franc’s appeal. The key uncertainty now is how the Swiss National Bank responds. The SNB has a long history of discomfort with excessive franc strength, and the currency has rarely traded much higher against the dollar outside of the brief surges seen in 2011 and 2015. Yet despite the nominal exchange rate approaching those historical highs, Switzerland’s real‑effective exchange rate does not point to an overvalued currency. That gives the SNB more room to tolerate further appreciation. Recent data on sight deposits and foreign‑exchange reserves also indicate that the central bank has largely stayed out of the market. Taken together, the backdrop suggests the franc’s strength may have further to run.

CAD Relief week. Having punched below the 20‑day SMA (1.3812) and 200‑day SMA (1.3836) in a single wide‑range candle while also exiting beneath the Ichimoku Cloud base, a sequence that typically marks a transition from distribution into trend, the USD/CAD is poised to hold onto weekly gains. With price now below all the major moving averages—including the 50‑day (1.3864) and 100‑day (1.3907)—the moving‑average stack is Loonie bullish, and rallies into prior support should be treated as fading opportunities rather than trend breaks. The immediate objective sits at the 1.3700 psychological level; failure to attract buyers there would keep pressure on the downside trajectory. Conversely, only a daily close back above the 1.3812–1.3836 zone (the 20‑/200‑day cluster and the underside of the Cloud) would neutralize the current impulse. Looking ahead, next week’s North American double‑header is the obvious catalyst risk: the Bank of Canada announces on Wednesday, Jan 28, and the FOMC later that day. Both central banks are widely expected to hold policy steady, which makes guidance and balance‑of‑risks language the swing factor for USD/CAD’s next leg. Expect positioning noise into the events, with 1.3812–1.3836 acting as the near‑term pivot on pops and 1.3700 the key downside magnet if the bullish trend resumes for the Loonie.

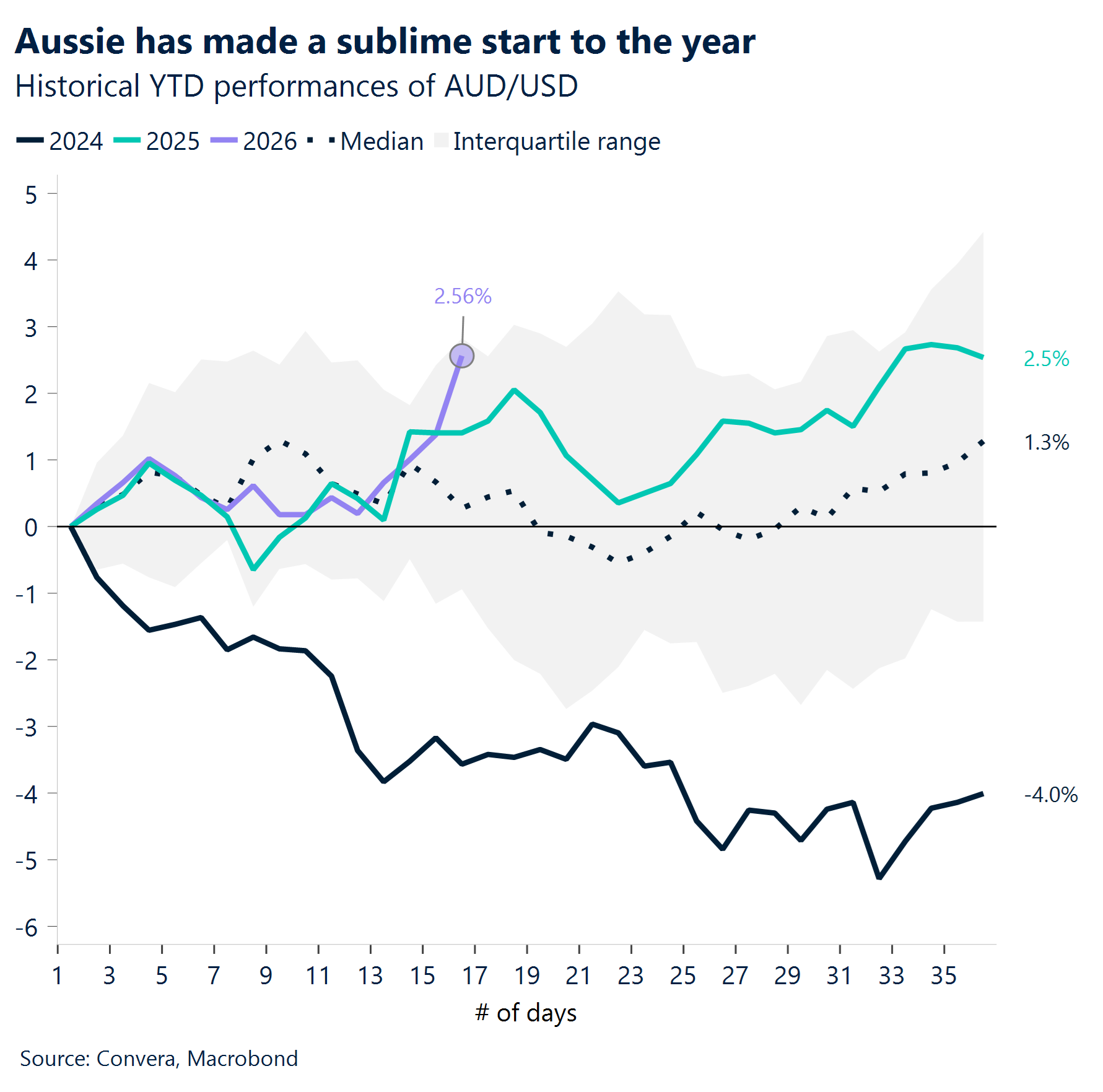

AUD Aussie hits 15-month high. The Reserve Bank’s February meeting is shaping up as a live event after strong December jobs data. A hot Q4 inflation print could put a rate hike back on the table. Employment surged by 65.2k, driven by a 54.8k jump in full‑time positions, far above the +27k forecast. The jobless rate dropped to 4.1%, beating expectations of 4.3% and the RBA’s December projection of 4.4%. Participation held steady at 66.7%, just shy of the 66.8% estimate. AUD/USD has pushed toward the top of its rising channel. Support sits at 0.6721 on the 21‑day average, with the 50‑day close behind at 0.6665. Market participants should keep an eye on upcoming CPIs, and PPIs data.

CNH China rolls out loan perks to fire up spending. China unveiled new incentives to spark investment and consumer demand, including a CNY 500bn loan guarantee facility aimed at helping private firms expand, the Ministry of Finance said in a statement. Small and medium-sized enterprises will also benefit from a two‑year annual interest subsidy of 1.5 percentage points on qualifying loans. In addition, the ministry extended consumer loan discounts through the end of this year. Vice Finance Minister Liao Min said at a press briefing that public spending will expand from 2025 as the government pursues a “more active” fiscal stance. He added that the budget deficit and bond issuance will stay at “necessary” levels, while more funds will be directed toward boosting consumption. USD/CNH sits at the bottom of its Bollinger Band, pointing to oversold conditions. The next resistance is at the 21‑day EMA of 6.9793, followed by the 50‑day EMA of 7.0174. Market participants should keep an eye on upcoming Chinese industrial profit.

JPY BoJ stays put as one member pushes for a hike. The Bank of Japan kept rates at 0.75%, as expected, while Takata broke ranks and voted for a move to 1%. The bank now expects growth in fiscal 2026 and 2027 to reach 1% and 0.8%, up from 0.7% and 1%. It struck a cautious tone, noting that the economic recovery has slowed. It also raised its core‑core inflation outlook above 2% through fiscal 2027 and highlighted the risks coming from currency moves and import costs. Support sits at the 21‑day EMA of 157.65, followed by the 50‑day EMA of 156.36. The pair remains at the lower end of its ascending channel — a setup that could signal continued strength. Market participants should keep an eye on upcoming Monetary Policy Meeting Minutes, Tokyo core CPI, and industrial production.

MXN Rally resumed. While developed markets grappled this week with a fresh wave of geopolitical “noise” and trade uncertainty, the Mexican Peso has emerged as a standout performer, defying the broader risk-off sentiment. The currency has rallied to its strongest level in over two years, trading near the 17.50 mark. This resilience is particularly striking given the turmoil in the U.S. and Europe, where new tariff threats, sparked a momentary “sell America” trade. For the Peso, the narrative has shifted from being a victim of trade wars to a beneficiary of high-interest-rate, bolstered by Banxico’s restrictive 7% policy rate.

The Mexican Peso sits at a volatile crossroads where fundamental strength meets technical exhaustion. While Latin American equities have surged around 6.4% year-to-date, significantly outperforming their developed-market peers, the “Super Peso” is now facing its toughest test of 2026, the cooling sentiment from institutional heavyweights such as JP Morgan, which recently called LatAm currencies run to be overbought. If global volatility continues to rise, the overcrowding of this popular trade could lead to a sudden liquidity squeeze. For investors, the challenge is now distinguishing between a structural shift toward emerging markets and a tactical bubble that is ripe for profit-taking.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.