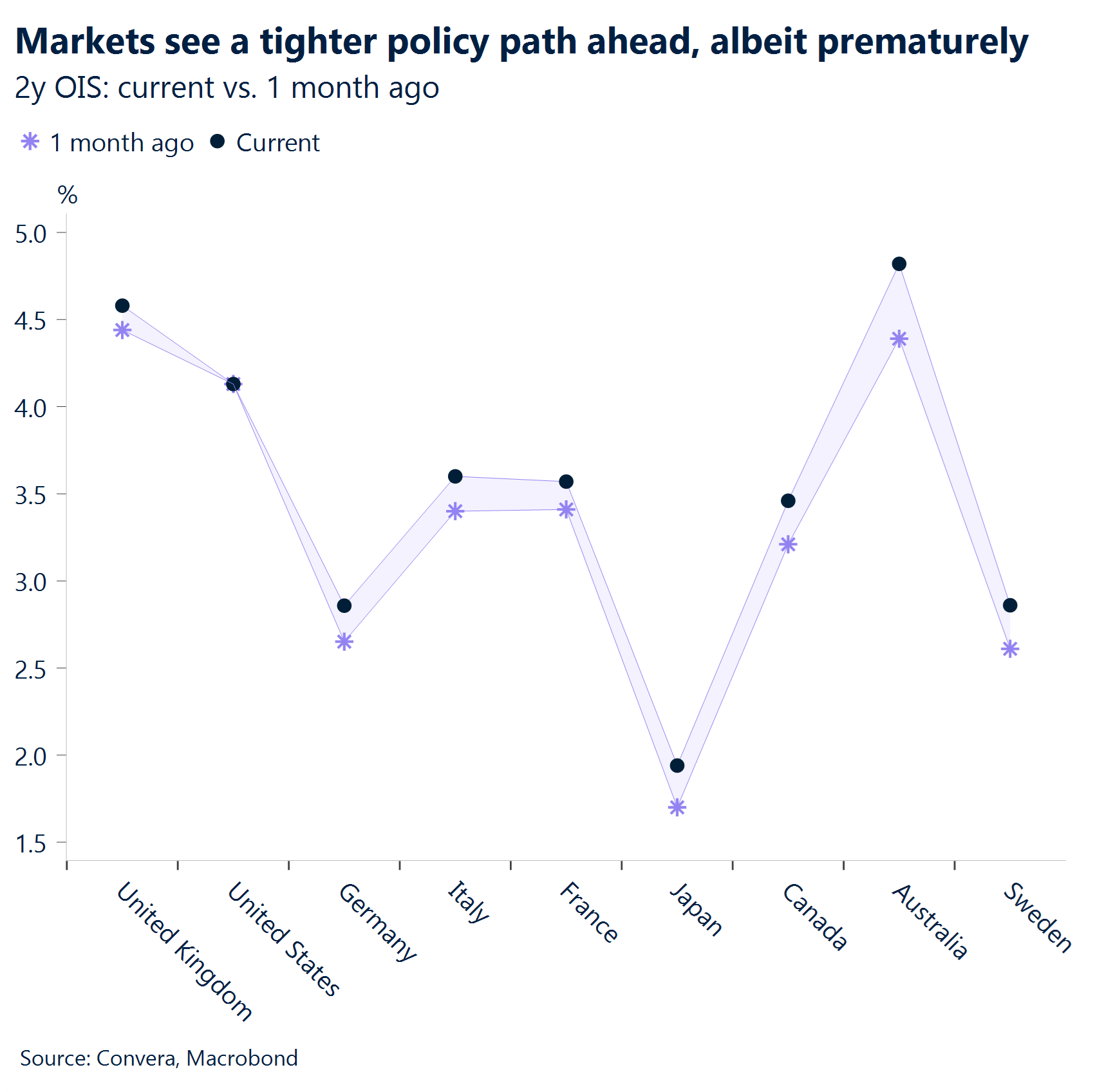

- Schnabel triggers yield recalibration ECB’s Schnabel noted early in the week that she would be comfortable with the next move being a hike, sparking a global recalibration toward tighter policy in 2026 and pushing yields higher worldwide.

- FX impact waits on 2026 outlook FX consequences remain muted until the 2026 economic outlook becomes clearer, allowing a reassessment – with data‑driven evidence – of which policy path is truly mispriced.

- Dollar pressured by job softness For now, the dollar looks more disadvantaged, with the US standing out as having the softest labour market among the majors: eurozone, Canada, and Australia.

- Central banks hold It was a heavy week on the central‑bank front, mostly tilting hawkish, with rates held in Canada, Switzerland, Australia, and the US.

- France survives, main vote ahead French Prime Minister Lecornu narrowly survived a crucial test as parliament backed the 2026 social security budget bill, sparing the government from immediate crisis. Risks linger with the main budget vote still due before year‑end, and deep divisions cast doubt on a repeat victory.

- Fed cut lifts, Oracle dampens Stocks enjoyed a brief rally as the Fed delivered a third consecutive cut with a less‑than‑hawkish tone. However, Oracle’s earnings release the same evening reignited concerns about vast AI‑related spending, after reporting a jump in data‑center and equipment costs.

Global Macro

Mounting dissent, fragile balance

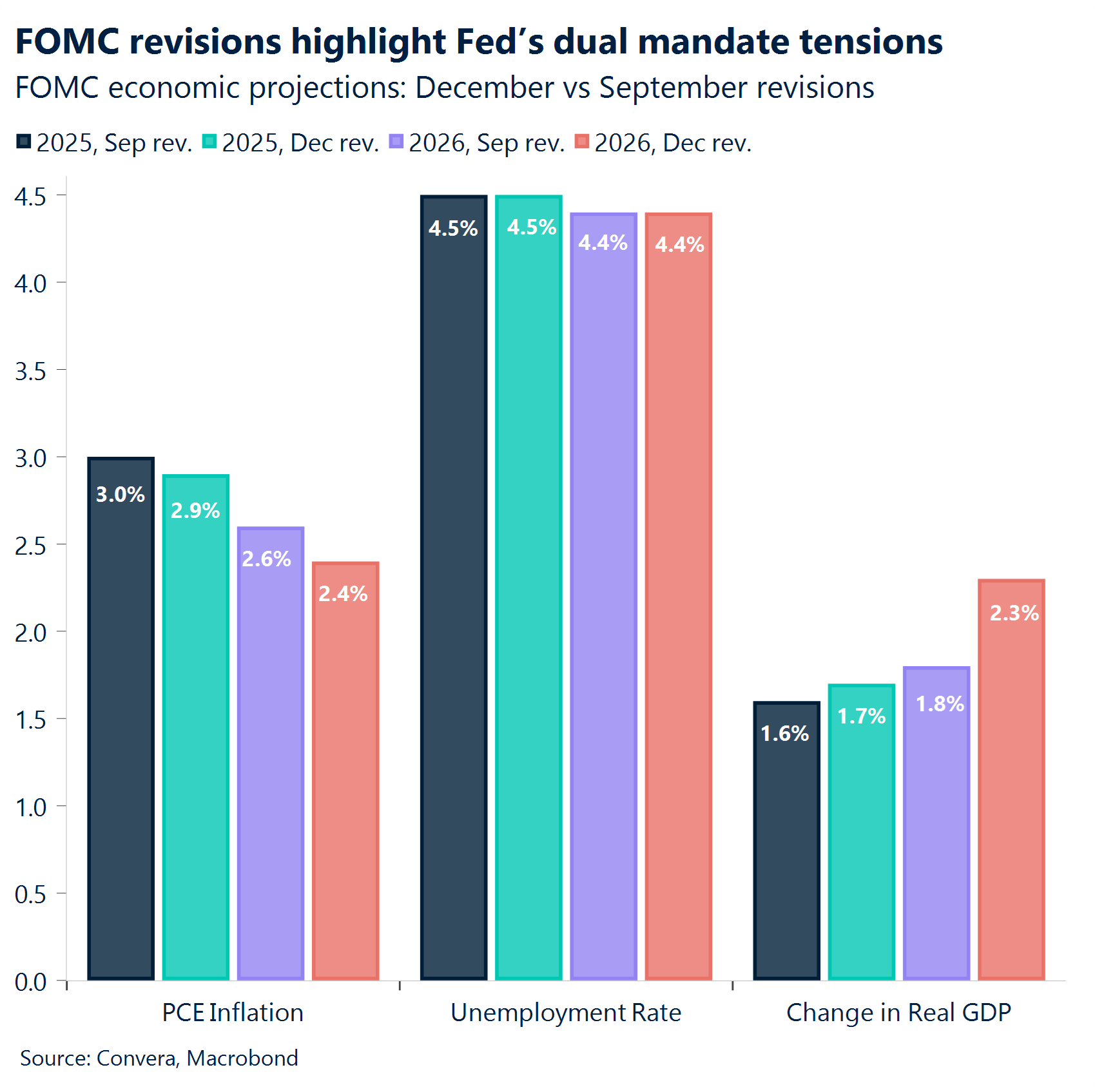

Fed cuts again, divisions deepen The Fed delivered a third consecutive rate cut, lowering the target range to 3.50–3.75 and signaling one more in 2026. The vote split was 9–3 in favour of a quarter‑point reduction. The dollar index slipped 0.4%, as markets – despite having priced in the cut – have also grown more familiar with Powell’s cautious, data‑dependent tone, which set the bar high for more hawkish surprises. Still, divisions within the FOMC were clear: two formal dissents and several “silent” ones from regional presidents who argued for higher rates into 2025. That backdrop suggests next year’s easing will be shallow unless the macro backdrop deteriorates materially.

Hawkish tilt, dovish doubts. From Australia to Europe, this week’s hawkish recalibration in policy paths into 2026 – sparked by ECB’s Schnabel – offers a preview of next year’s stance rather than a near‑term FX driver. While the global thrust remains dovish, its durability is increasingly in doubt. Caution and dissent dominate, shaped by stronger growth expectations, with key catalysts: Germany’s fiscal push, the US “Big Beautiful bill,” and still‑elevated inflation. The credibility of this hawkish tilt will only be clear once the 2026 macro backdrop takes shape.

Mixed JOLTS, scrutiny shifts to NFP. JOLTS data for October painted a mixed picture: job openings beat expectations at 7.67 million versus 7.12 million, while the quits rate fell and layoffs edged higher. This suggests workers are less confident about finding new jobs, even as employers show tentative signs of willingness to hire. Rising layoffs – partly tied to AI‑driven transformation – add further complexity, while shutdown‑related disruptions may also have skewed the data. Attention now turns to next week’s November NFP, also under greater scrutiny because of the shutdown.

Week ahead

ECB steady, but how dovish can BoE turn?

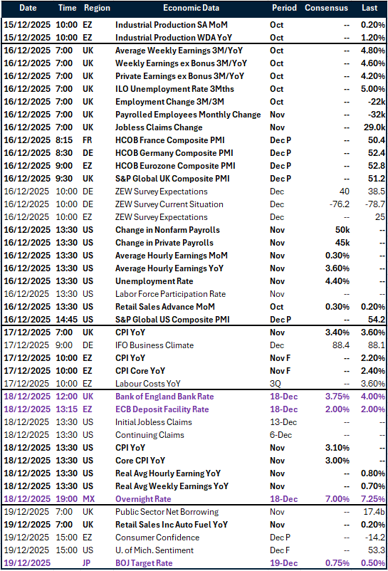

ECB steady, BoE set to cut. A series of central bank meetings are due next week, notably the ECB and the BoE. The latter is expected to cut, although we remain doubtful of how dovish the tone will sound given still‑elevated inflation levels. The ECB, meanwhile, is set to remain steady, with analysts eager to hear Lagarde’s potential response to Schnabel’s recent hawkish remarks.

UK labour & inflation in focus. Key UK data is also due: the labour market and October inflation reports will provide a vital feed to help the Bank gauge the degree of softness in employment and whether September’s cooler inflation print marked the start of a more prolonged easing pattern.

FOMC divisions, data will decide. A similar story is unfolding in the US. The November NFP report, coupled with CPI, will be key inputs in shaping the Fed’s policy path as we head into 2026, particularly after the growing dissents within the FOMC.

Unemployment and wage growth gain policy weight. On the US labour market, unemployment has gained greater importance, as Powell recently highlighted, alongside wage growth. At the December meeting, the Fed Chair stressed that cooling wage growth – driven by a softer labour market – is the main culprit behind lower services inflation.

FX Views

Fed puts pressure back on greenback

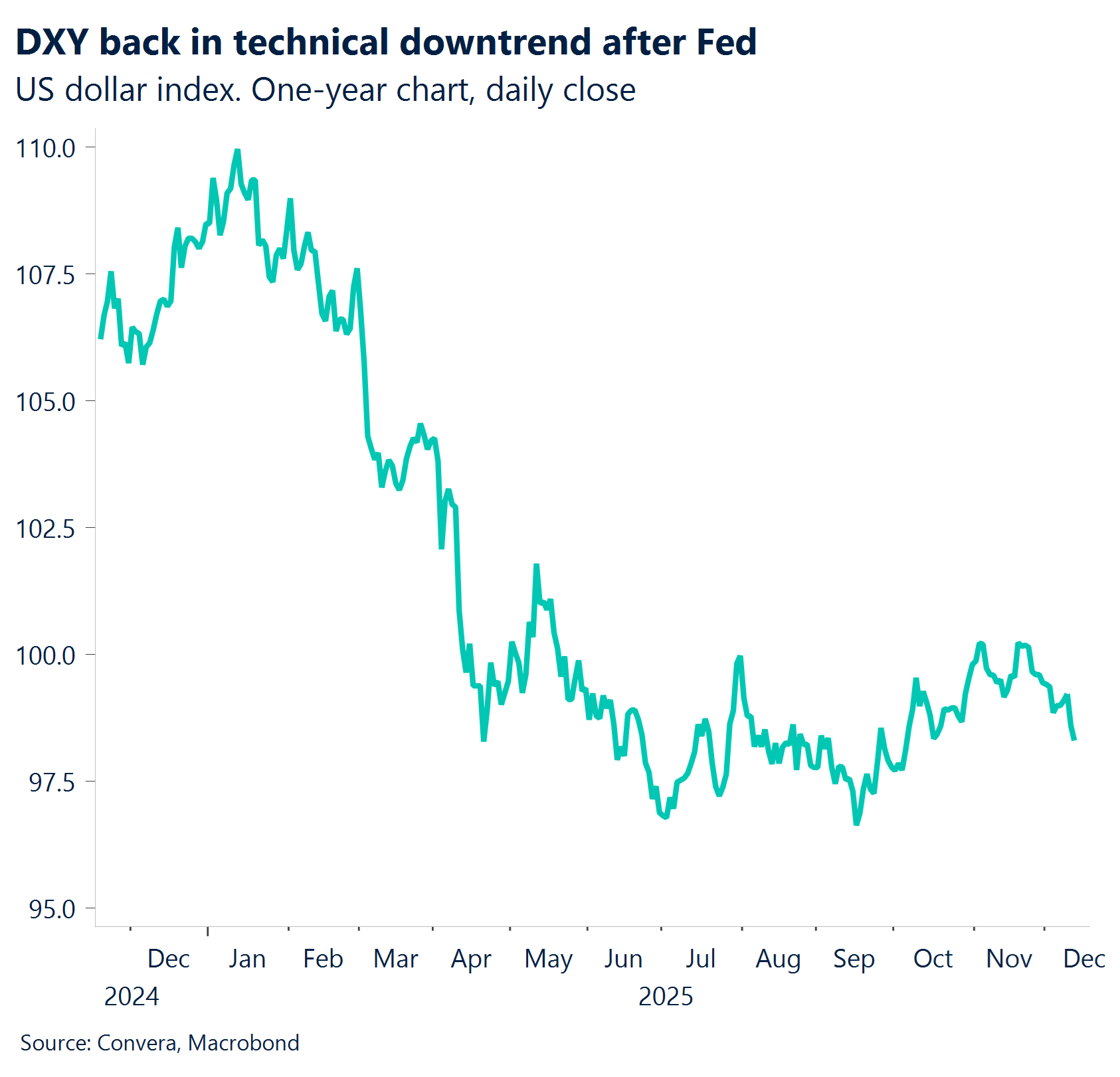

USD Fed hits greenback. The greenback extended its recent weakness with a third consecutive weekly decline. The Fed’s decision to cut interest rates was highly disputed, with a 9–3 split highlighting deep divisions within the Federal Open Market Committee (FOMC). The three dissents marked the highest number of objections in six years. The Fed board remains divided as a weakening jobs market coincides with rising inflation. Chair Powell said the labour market took precedence because the Fed believes the inflation uptick is largely tariff-driven, while non-tariff components are cooling. The US dollar weakened after the announcement, with the benchmark USD index falling to a two-month low, pushing the broader greenback index back into a short-term downtrend.

EUR Euro nearing highs. The euro strengthened over the past week, mainly supported by a weaker US dollar. Early-week remarks from ECB’s Schnabel, suggesting the next move could be a hike, also provided a boost. However, since the US government shutdown began in early October, EUR/USD has tracked rate differentials less closely, indicating that the USD leg—typically a proxy for Fed policy expectations—may have lost some FX-moving power. EUR/USD gained for a third consecutive week. The technical outlook remains positive, with key moving averages pointing higher, though major resistance is seen at 1.1840 and then 1.1920.

GBP Jobs, inflation key. GBP/USD climbed to two-month highs, supported by the Fed’s mid-week cut. A private survey by the Recruitment & Employment Confederation (REC), KPMG, and S&P Global showed wage growth picked up in November despite a weak labour market, briefly reducing expectations for a cut next week. Persistent wage pressures suggest inflation may prove stickier than anticipated, keeping the MPC divided and GBP under partial bearish pressure through rate differentials. Hard data will ultimately decide the outcome. Labour market and inflation reports are due next week, just days before the policy meeting. A softer November inflation print, following October’s below-expectation outcome, could push the board toward a more dovish stance, potentially allowing sterling to break below 1.33 with greater sustainability.

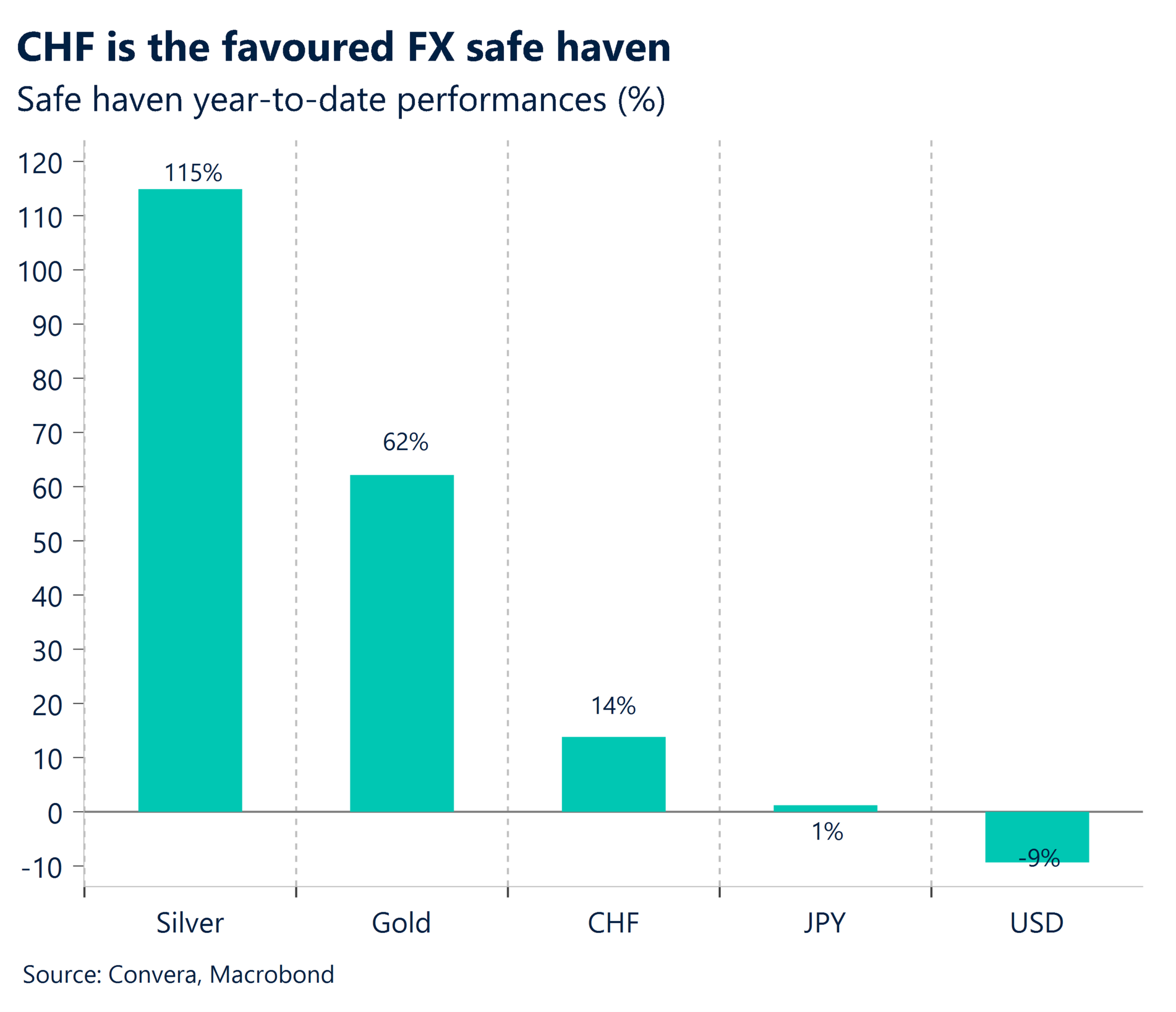

CHF SNB opens door to negative rates. USD/CHF fell to a one-month low after the SNB held rates at 0.00% but kept the door open for further cuts. This marked a shift from September, when SNB Chair Martin Schlegel suggested a high bar for lowering rates below zero. Despite rapid rate reductions over the past year, the Swiss franc has continued to gain as geopolitical tensions boost its safe-haven appeal. USD/CHF dropped to its lowest level since 14 November, while EUR/CHF hit two-week lows and GBP/CHF fell to one-week lows.

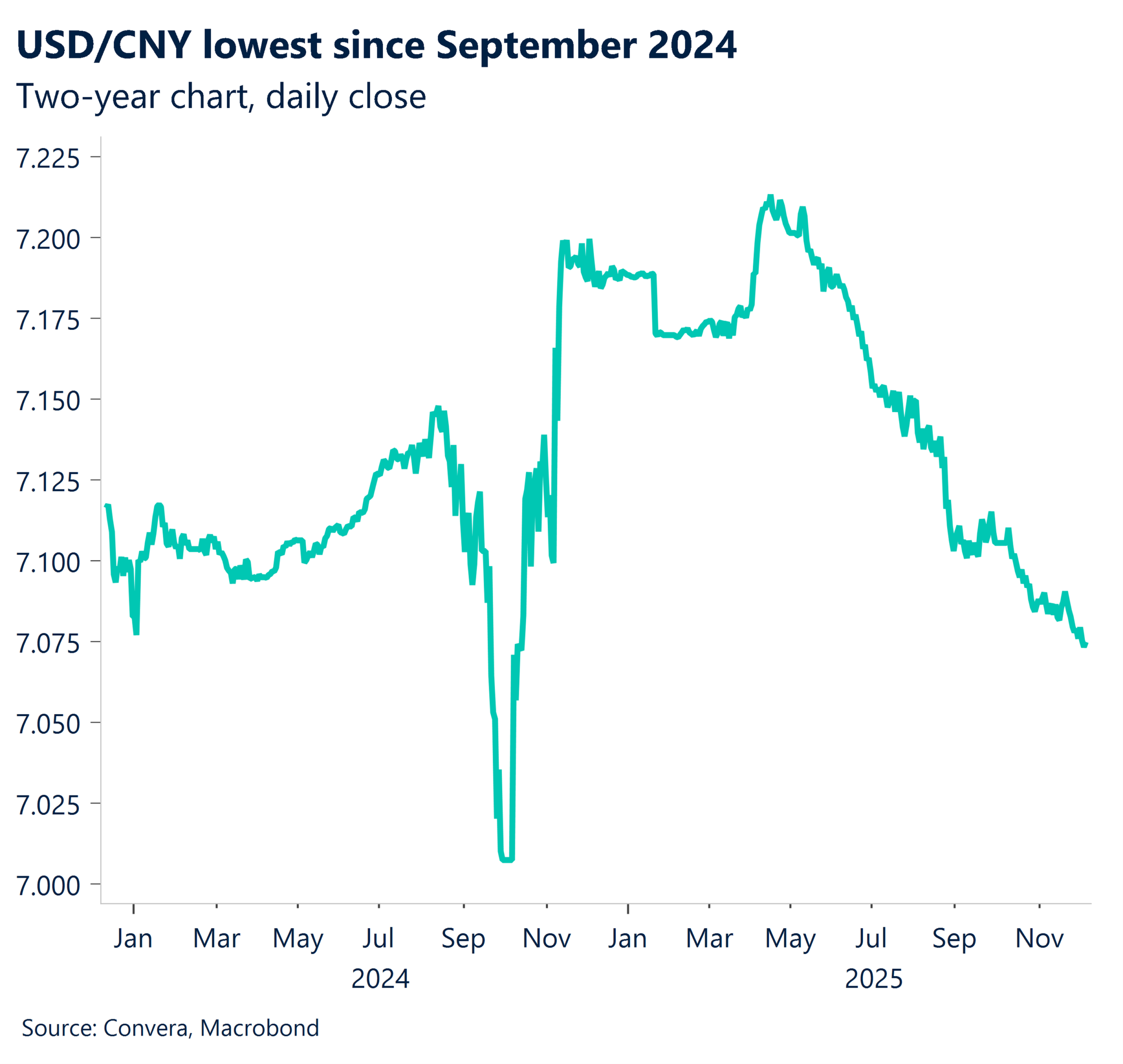

CNH New highs. The Chinese yuan strengthened to its highest level since September 2024. While most Asian currencies have weakened against the US dollar, the yuan has outperformed. This is notable because the move runs counter to regional trends—particularly the yen’s year-long decline—and appears supported by the People’s Bank of China. The yuan’s strength has impacted local companies, with The Securities Times reporting a surge in hedging activity. Onshore USD/CNY fell to its lowest level since September 2024, while offshore USD/CNH neared 18-month lows at key support around 7.0500.

JPY BoJ in focus. The yen sell-off continued despite expectations of a BoJ hike. The Japanese yen drifted lower even as officials signalled a likely rate increase next week. BoJ Governor Kazuo Ueda told the Financial Times on Tuesday that the bank is nearing its inflation target, saying: “We are closer to 2% inflation on a sustained basis…I can say that I think.” However, slowing data this week, including a drop in Economy Watchers Sentiment, weighed on JPY. USD/JPY was initially stronger but eased after the Fed’s mid-week cut. In Europe, yen losses were even more pronounced: GBP/JPY climbed to its highest level since 2008, while EUR/JPY reached an all-time high. Next Friday’s Bank of Japan decision will be key.

CAD Support breaks, but market oversold. USD/CAD fell to three-month lows, breaking key support at 1.3800 after the Bank of Canada held rates steady at 2.25%. Technically, a deeper move lower may be harder in the short term. The relative strength index, a key momentum gauge, recently turned from “overbought,” which can signal a reversal higher. Support is seen at 1.3725, while upside targets are 1.3900 and then 1.3920. CPI, due Tuesday, will be the upcoming week’s major event.

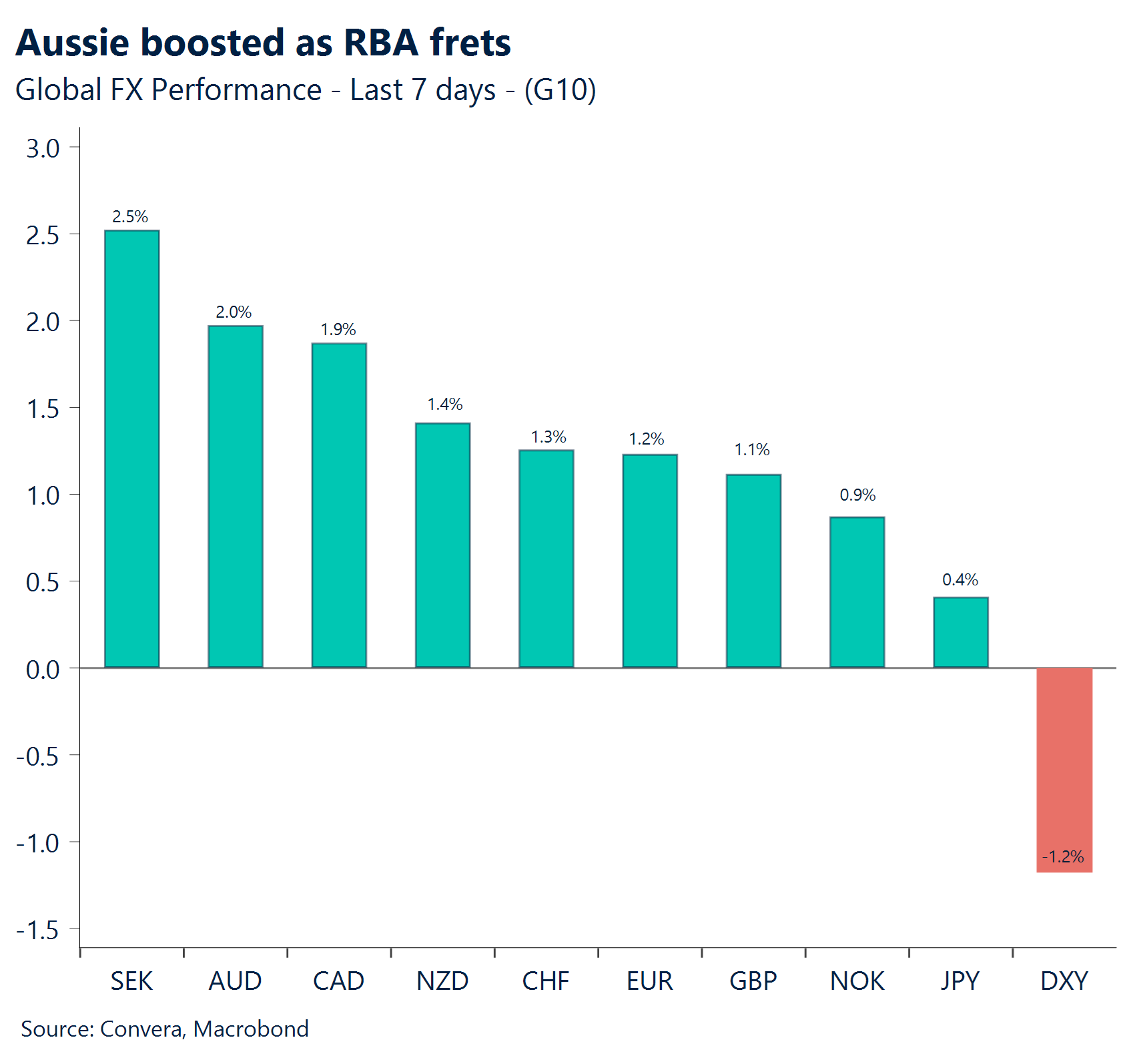

AUD RBA to consider hikes. The Australian dollar strengthened last week following the December RBA decision. Markets have abandoned expectations for further cuts as inflation heats up. Annual headline inflation rose from 3.6% in September to 3.8% in October – more than double the 1.8% seen in June. Traders now expect the next move to be a hike by August next year. AUD/USD moved toward the top of its recent range, with support at 0.6400 and resistance at 0.6700. A break above 0.6700 could set up a move toward 0.7000. Manufacturing and services PMI numbers along with the government’s mid-year economic and fiscal update will be the week’s key events.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.