- Gulf tensions. Oil surged over 6% this week as US-Iran conflict fears intensified, weighing on broader risk sentiment and prompting further de-risking.

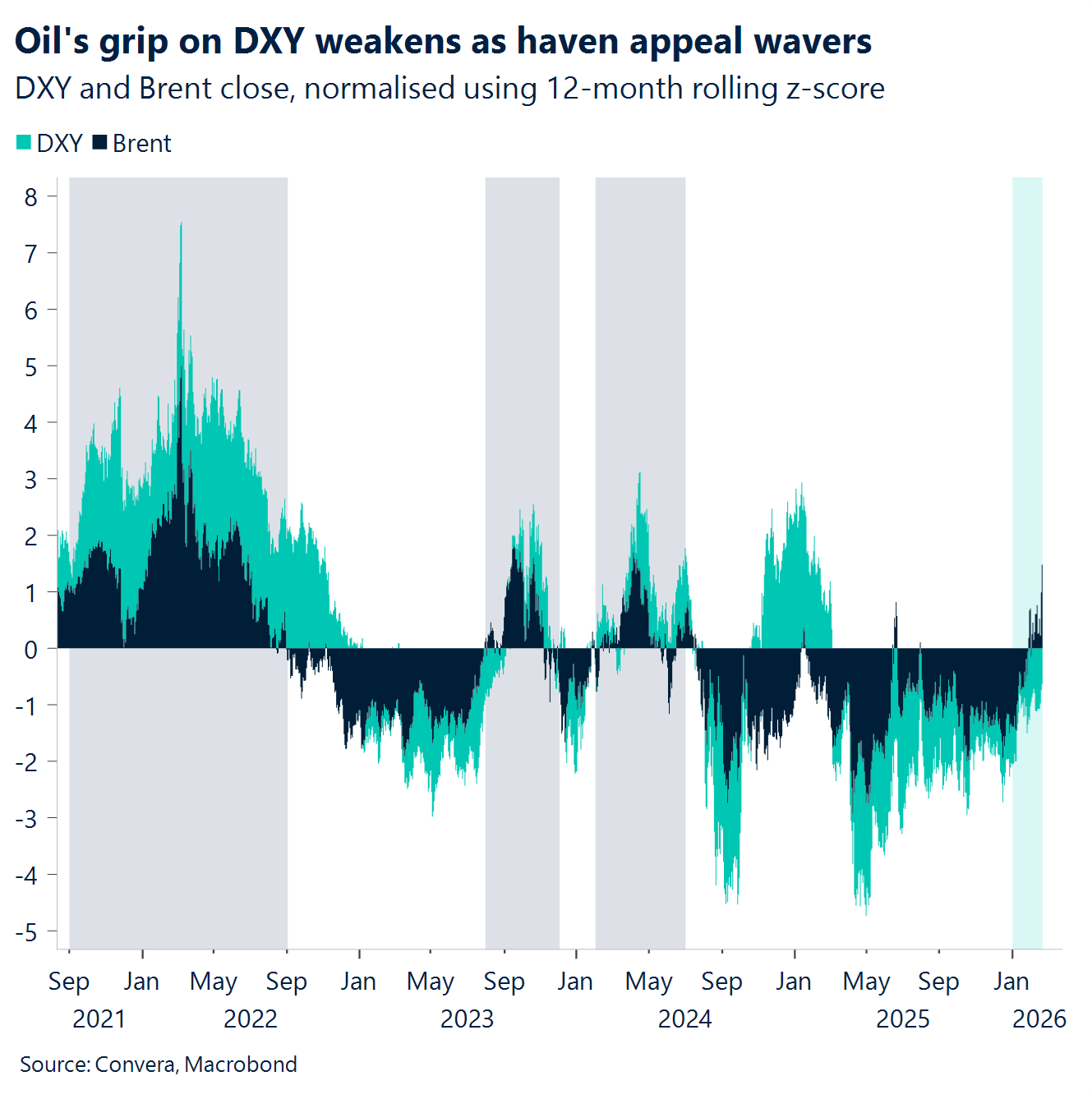

- Commodity kicker. Geopolitical tensions have supported the dollar via higher oil prices. Post-Liberation Day, the dollar’s safe-haven appeal re-emerges during oil shocks, helped by the US being a net energy exporter. AUD has also benefited.

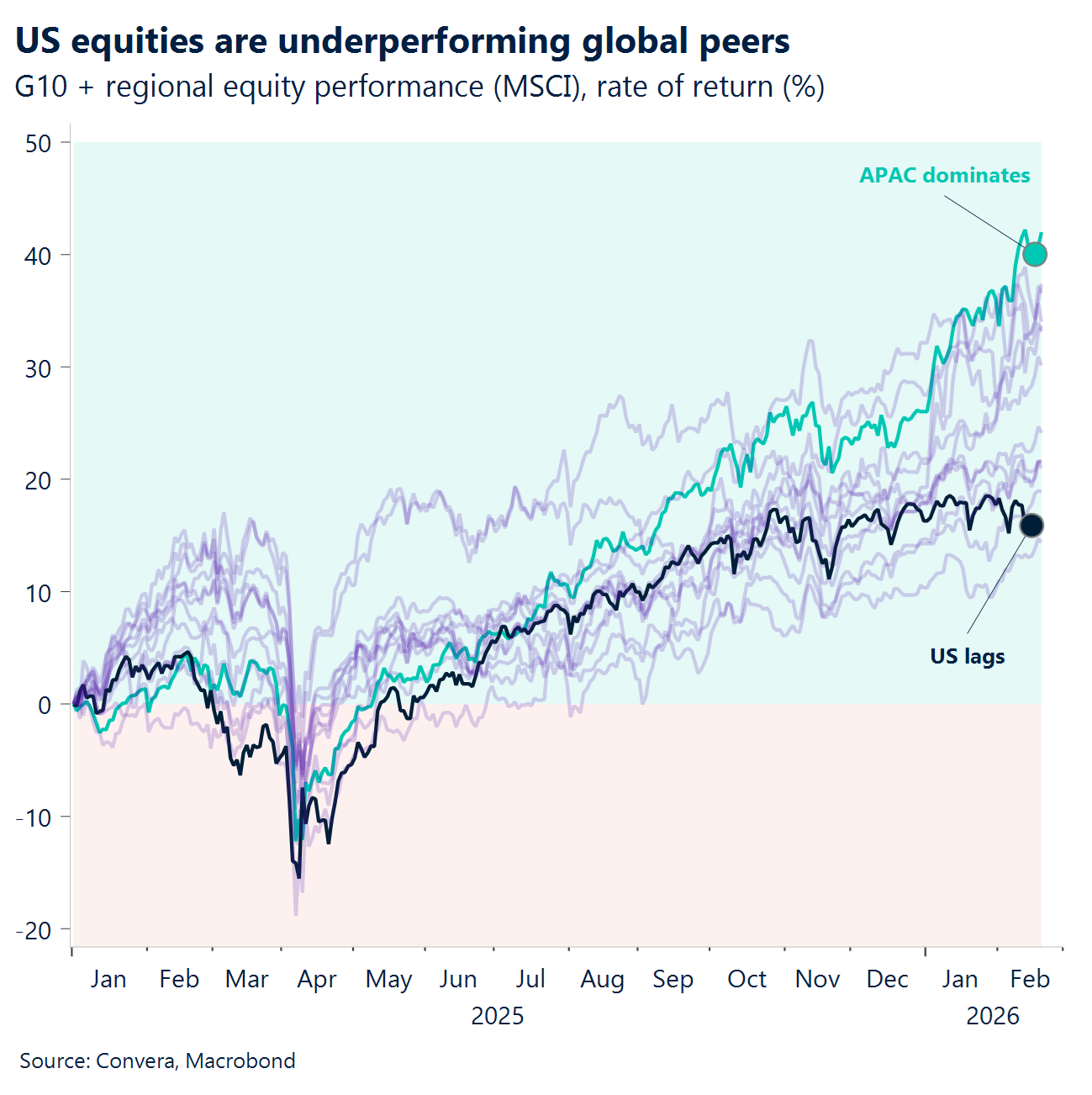

- America bought, not sold. Strong US growth keeps investors buying American assets, debunking the “sell America” myth, yet US equities still lag global peers, with APAC markets leading performance.

- Hawkish hints. Fed minutes showed renewed inflation worries and fading labour concerns. Some officials even signaled rates may need to rise again. This lifted short-term yields and added support to the dollar’s over 1% rise this week.

- Policy collision. A hawkish Fed risks clashing with President Trump’s push for lower rates, complicating the task of the president’s nominee for chair, Kevin Warsh and potentially lifting long-term yields and pressuring the dollar again.

- Kiwi cool-down. A dovish RBNZ pushed expected rate hikes out to 2027, knocking the kiwi and resetting policy expectations.

- Dovish UK pulse. Soft UK data — rising unemployment, cooling wages and falling inflation — reinforced expectations of earlier BoE cuts. Sterling is under pressure, ignoring upbeat retail sales/PMI data and eying political risk next week.

Global Macro

A ‘tariff-proof’ trade deficit

A meager decline. Despite the administration’s claims of victory, the 0.2% dip in the 2025 trade deficit (to $901.5 billion) was a statistical mirage driven by a spike in gold exports rather than a structural shift. Under the surface, the goods deficit actually hit a record $1.24 trillion. While tariffs slashed the deficit with China by nearly 32%, the gap simply migrated to other nations. Furthermore, the “softer” dollar has failed to close this divide; even with more competitive export pricing, the US remains tethered to high-tech imports that cannot yet be sourced domestically.

A hawkish surprise. The latest Fed minutes reveal a board that is fundamentally divided, and it appears Powell struggled to communicate these diverging views in his most recent press conference. While the prospect of a “hike if necessary” is back on the table, the defining challenge for the incoming Fed Chair, Kevin Warsh, will be selling the board on his thesis, that AI forces are structurally disinflationary. This friction is set to revive macro-borne volatility in Q2.

Cooling prompts cuts. A cooling UK economy has cleared the path for a potential Bank of England rate cut next month. January data shows headline inflation hitting a nearly one-year low of 3.0%, supported by broad declines in both goods and services. This disinflationary trend is reinforced by a softening labor market, where unemployment climbed to 5.2%, including a sharp 14% for youth, and private-sector wage growth slowed to 3.4%. Together, these figures provide the “green light” for a pivot toward monetary easing.

Week ahead

A week ruled by sentiment

UK politics back in the spotlight. UK by-elections are held next week. With Starmer’s leadership facing significant challenges as key Labour figures urge the Prime Minister to step down, political uncertainty has re-emerged, reminiscent of the pre-Autumn Budget period, leaving sterling vulnerable to further weakness.

The business-side sentiment check. Germany’s IFO business-climate indicators are due Monday. After last week’s soft ZEW print, the IFO will help show how business sentiment is evolving. ZEW reflects financial-market views, while the IFO captures business leaders’ assessments, giving a more rounded sentiment snapshot as 2026 begins. After a rapid rise in early 2025 on the back of government spending plans, the index has since stalled as enthusiasm faded on still-unrealised gains.

Consumer sentiment still bruised. Across the Atlantic, the Conference Board consumer-confidence release will be in focus. The headline index sits at its lowest level since the pandemic, reflecting discomfort with Trump’s policy direction, a softer labour market, and still-elevated living costs. Both the current and expectations components dropped sharply in January after the Greenland attacks and renewed tariff tensions. With some of that pressure now easing, a modest rebound is expected.

The key driver of eurozone disinflation. Germany’s preliminary February CPI release is due. The headline figure dipped below the 2% target in January 2026, reaching 1.10%. With Germany being the largest contributor to the eurozone HICP aggregate, monitoring its disinflationary trend is crucial at a time when risks of eurozone inflation undershooting are mounting.

FX views

Oil and Fed minutes lift the bruised buck

USD Dollar’s lift, not a launch. The dollar index heads into the end of the week roughly 1% higher. A still soft sentiment toward the greenback has been overshadowed by upbeat US macro data, alongside a geopolitical layer involving military pressure on Iran to secure a nuclear deal. While the dollar’s safe haven appeal has diluted more broadly, it still dominates JPY and EUR in oil-linked episodes given its central role in oil invoicing and its status as a major exporter of the black gold. That said, only further escalation would justify additional dollar upside. On the macro side, strong weekly jobless claims and firm industrial production figures continue to point to a more stable labour market and solid economic activity, messages reinforced by the Fed minutes from the January meeting. Still, with sentiment soft and a rates path that whispers hawkishness but is ultimately set on an easing course, the dollar’s medium-term orbit looks anchored around the 98 handle, which is where we expect the index to settle by the end of Q1.

EUR Euro momentum fades. EUR/USD spent the week grinding lower, slipping back below 1.18 after an extended rally to its strongest levels since 2021. Part of the pullback reflects a technical cleanout, but the heavier drivers were widening rate differentials and a spike in oil prices tied to Iran–US tensions, which the euro does not welcome as a net oil importer. The euro also faced its own curveball as Lagarde announced she would step down earlier than expected, a move read as politically strategic and one that reintroduces a degree of risk premium at a time when the “central bank independence” theme is back in focus. Meanwhile, hints of dovishness re-emerged as euro strength draws ECB attention and inflation sits below target. Still, the widening in rate differentials in favour of the dollar looks difficult to sustain unless upcoming data validates the emerging dovish versus hawkish contrast between the ECB and the Fed. It is too early to make that call, which is why we stop short of declaring a firm re-establishment of 1.18 as well-known resistance.

GBP Dovish drift. Sterling is heading for its biggest weekly decline against the dollar in more than a year, down around 1.4% as GBP/USD breaks key support and flirts with its 200-day moving average near $1.3445. The move reflects a clear dovish turn in UK data: unemployment has ticked higher, wage growth has cooled and headline inflation has fallen sharply. Markets now assign an 80% probability of a March BoE cut, and that shift in rate expectations has dragged on GBP across the board. With markets pricing a more dovish BoE and a more hawkish Fed, 12-month GBPUSD forward points have turned positive for the first time since August as the rate differential swings in favour of the dollar. While fragile global risk sentiment and geopolitical uncertainty add marginal pressure, the dominant drivers remain domestic. The UK’s softening data pulse, combined with a more dovish BoE outlook, leaves sterling vulnerable. Political risk is the other key headwind: next week’s by-election could add further strain on PM Starmer’s leadership team and reinforce the sense of policy uncertainty.

CHF Structural strength. The Swiss franc remains exceptionally strong, with inflows driven by a mix of dollar-debasement concerns and geopolitical hedging, including recent fears of a potential US strike on Iran. EUR/CHF is holding near the 0.91 handle, its lowest level on record outside the brief 2015 dislocation, and the pair is likely to stay under pressure until geopolitical tensions ease and the US naval build-up in the Middle East recedes. Speculation around SNB intervention is building, but the bar remains high. Inflation is still comfortably within the SNB’s target range, and the bank is reluctant to provoke the US administration by leaning too visibly against franc appreciation. Officials have repeatedly stressed they do not want to take policy rates negative again, yet persistent downward pressure on EUR/CHF means markets may start to price in a full 25bp SNB rate cut over the coming year. For now, the franc’s safe-haven appeal and the lack of credible policy pushback leave CHF strength firmly in place.

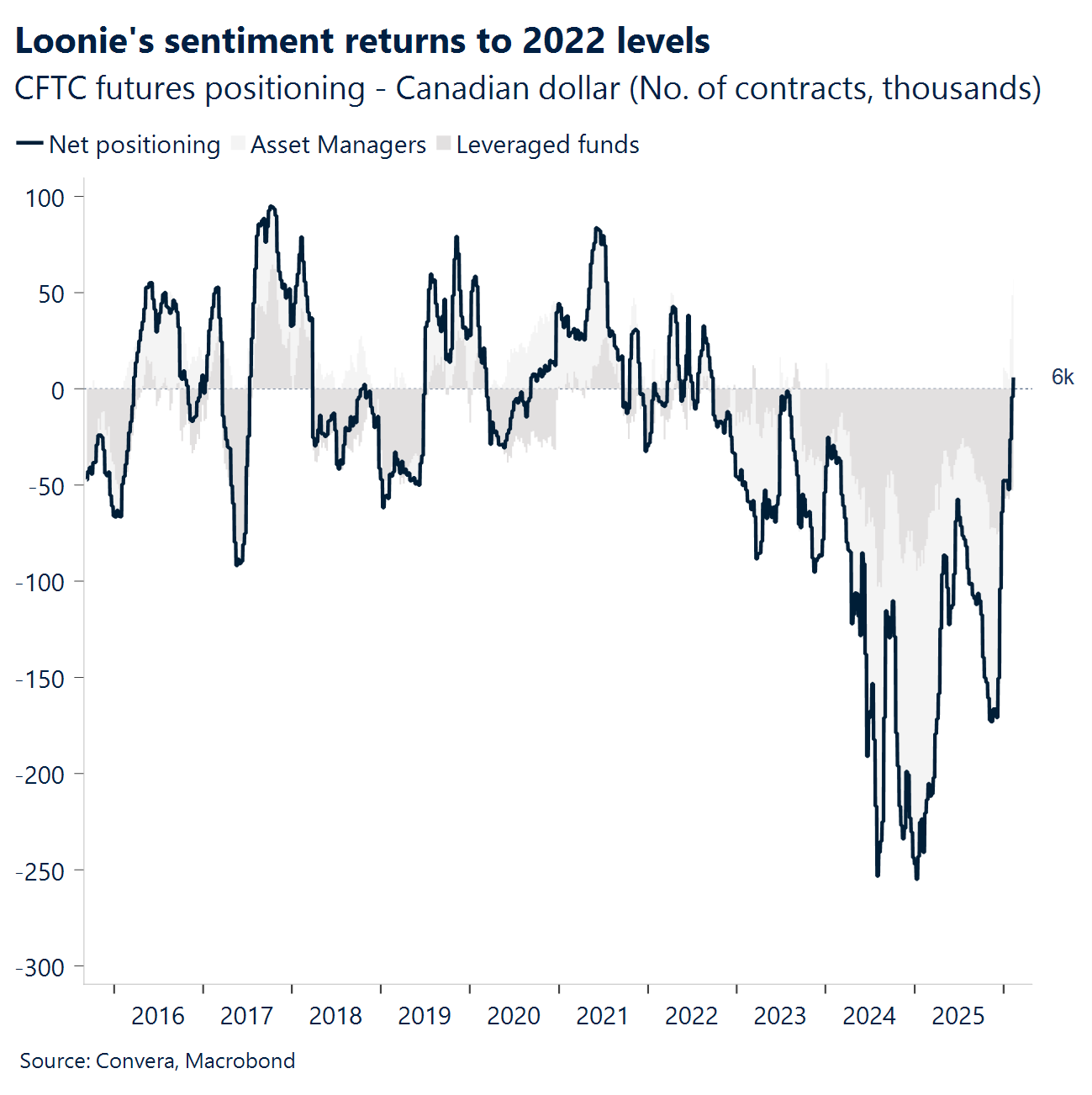

CAD Still lagging the majors. Heading into 2026, the extreme pessimism surrounding the Canadian Dollar has officially flipped, as speculative positioning recovered from record lows of 250,000 net short contracts to a modest 6,000 net long. While this shift removes a two-year structural headwind, the Loonie’s 0.4% year-to-date gain significantly trails its G10 peers, such as the Norwegian Krone (+6.1%) and Australian Dollar (+5.9%). Despite a softer Greenback, the CAD is struggling to attract the aggressive capital flows seen in other commodity-linked currencies, hampered by persistent tariff risk premiums and a stagnant domestic economic outlook. This week the Loonie traded between 1.36 and 1.371, just right above its 200-weekly average at 1.357. Next Friday will be on focus as Q4 2025 will be released.

AUD March RBA risk wakes up. The latest jobs report surprised with a lower unemployment rate of 4.075%, a result that will make the RBA uneasy about waiting until May to act. If another hike already feels inevitable, the small pricing for March looks out of line with the much larger move expected by May. This week’s monthly inflation reading, followed by early-March GDP, will decide whether March becomes a live option. AUDUSD now trades about 1.7% below its recent high of 0.7147 on February 12. Key support sits near the 21-day EMA at 0.6998, with the 50-day EMA lower at 0.6871. Market participants will keep an eye on upcoming CPI and private new capital expenditure.

CNH China’s housing drag. China’s property market is now in its sixth year of decline. Despite government efforts—loosening home purchase rules, cutting mortgage rates, and buying back excess housing—the slump continues. Oversupply keeps prices edging down, encouraging buyers to wait, which in turn dampens construction further. In January, authorities again pledged to stabilize and revive the market, reaffirming their stance in the Qiushi Journal, the Communist Party’s official publication. Meanwhile, USDCNH has bounced off a 33-month low. It now sits 0.3% above the February 16 trough of 6.8810. Resistance lies at the 21-day EMA of 6.9205, followed by the 50-day EMA of 6.9616. Investors will be watching upcoming foreign direct investment flows for the next catalyst.

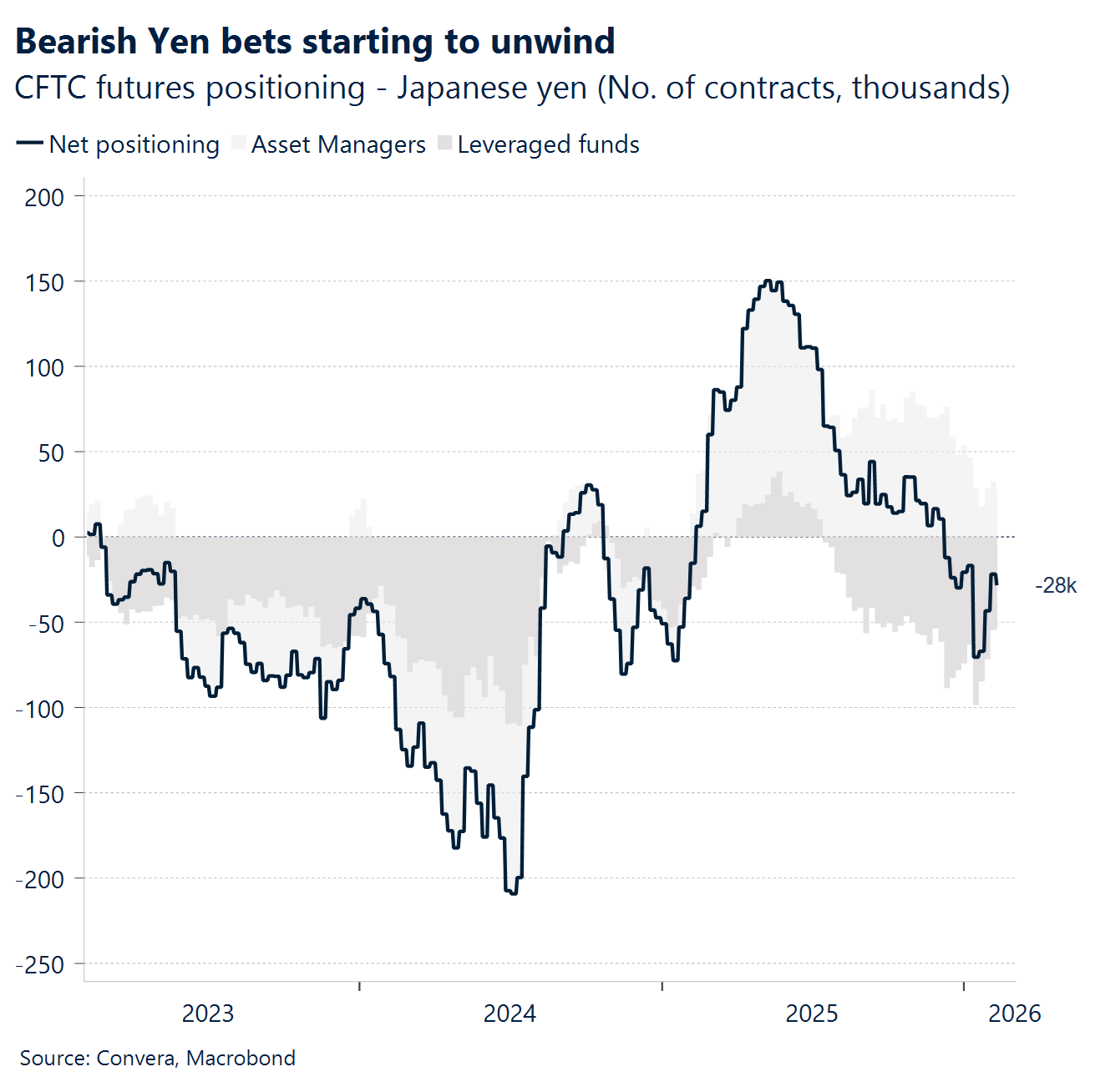

JPY USDJPY climbs to more than a week’s high. Japan’s core machinery orders surged 19.1% in December after an 11% drop the month before, far above expectations for a modest rise. Manufacturing orders jumped 25.1% and non-manufacturing climbed 8.2%, pointing to a clear pickup in investment and a stronger outlook for capital spending. USDJPY has pushed to more than one-week high and is trading above 155.00. The next resistance sits near 156.00, while key support is around the 100-day EMA at 154.34, where USD buyers may look to take advantage. Market participants will keep an eye on upcoming Tokyo core CPI and industrial production.

MXN Consolidation continues. The Mexican Peso highlights LatAm’s broader resilience as it continues to navigate a complex environment of domestic stability and international trade uncertainty. Even with reports suggesting potential changes to regional trade pacts, the currency has maintained its position as a top performer thanks to a decisive monetary policy stance from the central bank. By holding interest rates at 7% to counter core inflation pressures, the local board has ensured that the currency offers a 325 basis point advantage over the Federal Reserve. This robust yield differential has solidified the status of the peso as a preferred choice for global asset managers looking to diversify into local assets while seeking protection against broader market swings. This week, the Peso continued consolidating, trading between 17.08 and 17.30, as low volatility over the last couple of weeks hasn’t translated into further market moves downside. 4Q 2025 GDP (Mon), bi-weekly CPI (Tue) and unemployment rate (Thu) will be on focus.

BRL Hits resistance. The Brazilian real remains tightly tethered to global sentiment, with the 5.17 per dollar level serving as a persistent resistance ceiling that has capped recent gains. Despite hitting a 20-month high of 5.16 earlier in the month, the currency has struggled to sustain a break beyond this barrier due to a mix of external uncertainty and domestic hurdles. Local attention is currently split between upbeat activity data, with December GDP proxies expected to show a 2.3% year-over-year pickup, and the ongoing political fallout from the Banco Master fraud investigation. While strong growth figures typically support the real, they currently threaten to complicate the Bank of Brazil’s easing narrative, as policymakers weigh resilient economic demand against headline inflation that remains near the upper bound of the target at 4.44%.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.