Global investors are gearing up for the final weeks of an eventful year. Central bank meetings across the world and crucial inflation and macro data will shape financial markets going into year-end. Against this backdrop, we take a look at the expected outcome of rate decisions in the US, UK and Eurozone, with investors pricing in between 75 and 150 basis points of rate cuts from these central banks for 2024 alone.

Hopes for rate cuts. The first week of the last month of the year is shaping up to confirm the macro and market trends seen in November. Investors have continued pricing in more monetary policy easing for 2024 as disappointing macro data has dampened the global economic outlook. This has pushed global bond yields across the curve lower.

Weaker data. Signs of a cooling US labor market in the form of falling job openings and weaker private hiring have underpinned the sharp fall in government bond yields across both sides of the Atlantic. However, the weakness in Europe, with German industrial data disappointing, has helped the Greenback establish a short-term bottom against the euro.

Yields fall. The 10-year Bund yield fell from 2.64% to 2.24% in a matter of just two weeks in what has become the strongest rally in German bonds since March 2023. In the United States, yields on the 10-year Treasury have fallen by 80 basis points since the end of October but have steadied this week. This explains the outperformance of European equities (0.99%) versus their US peers (-0.2%), given that the dovish repricing had been stronger for the ECB versus the Fed.

Goldilocks holds. As we mentioned in our previous weekly publication, markets are both positioned for a soft landing and for the Fed to cut rates. Normally, these two conditions would not be compatible with each other. Since US data has weakened enough for investors to price in cuts, but not enough to cause panic, this “Goldilocks” environment has remained in place.

Higher volatility ahead. Investors have therefore cheered the peak in interest rates and the prospects of significant policy easing in 2024. However, while equities tend to outperform in the twelve months following the end of the Fed’s tightening cycle versus historical averages, this only holds true in cases where the US avoids a hard landing. Looking at the performance of the S&P500 around the start of the Fed cutting cycle in periods where the US falls into a recession gives us a median drawdown of 15% in the following 12 months. Meaning that the Fed easing policy is not a sufficient condition for risk assets to continue rallying – the US economy needs to avoid a hard landing too.

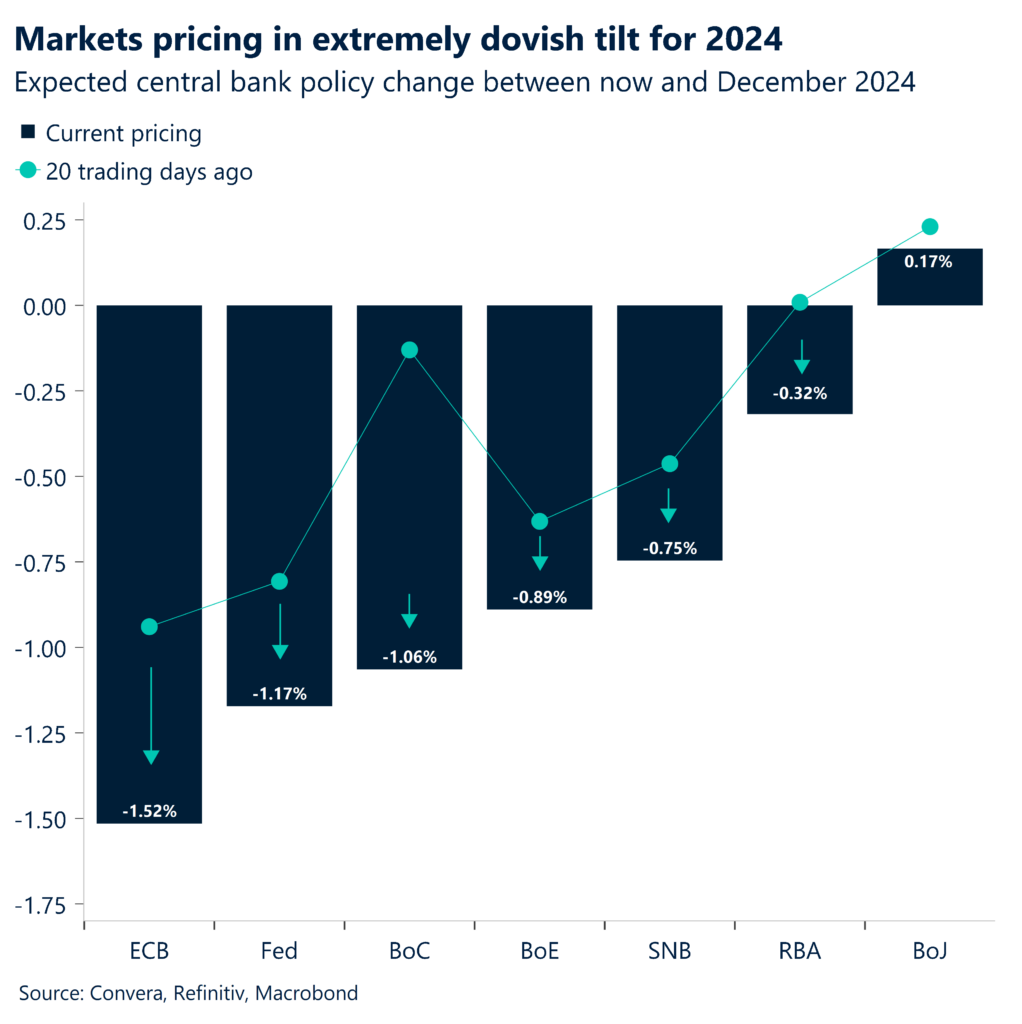

Inflation continues to slow globally. The slowdown of inflation across the globe and central banks ending their aggressive tightening cycle in November has shifted focus to 2024, with investors having started pricing in significant rate cuts from the Federal Reserve, European Central Bank and Bank of England. Last week saw US and Eurozone inflation fall to 3% and 2.4% respectively. The disinflationary trend has taken hold in other countries as well. Newly released consumer price data increased less than expected in November in South Korea (3.3%), Switzerland (1.4%) and Tokyo (2.3%) with inflation getting ever closer to target (2%).

Regional nuances matter. The magnitude of this disinflationary trend has however varied across regions with inflation in the UK and in Australia still elevated at 4.6% and 5.4%, which is why the pound and the Aussie dollar have outperformed the broader FX space in November. This has reversed a bit in December as weaker Australian data pushed up bets on RBA easing in 2024.

Global Macro

Last week’s major events

This week saw some negative equity price action in what looked like buyers’ fatigue and overly stretched cross-asset positioning. The US dollar is gaining its footing, after having fallen for three consecutive weeks with US Treasury yields trading higher by around 10 basis points across the curve versus the Friday close. The main question going into December continues to be how likely the 125 basis points of rate cuts by the Fed for 2024 priced in by markets are to materialize.

European bottoming from low levels. The Sentix Investor Confidence Index revealed that Eurozone investors’ morale improved for the third straight month in December. The headline index climbed to a 7-month high at -16.8 in December from -18.6 in November, a slight miss against market consensus. This was in line with the rise in the ZEW index reported last month and an overall rebound in risk assets. While a recent turn in a number of leading indicators gives something to cheer about going into 2024, the current situation remains dire, and momentum is weak. The headline Sentix index has remained in a negative territory for 22 consecutive months, the length only comparable to the GFC.

German factory orders crumble. German factory orders released this week did not provide much to cheer about. The index fell by 3.7% m/m, in a sign the industrial sector remains fragile. This has been confirmed by industrial production failing to grow for six consecutive months ending October. At the same time, Germany’s Dax index closed at all-time high as prospects of lower interest rates boosted demand for the country’s biggest stocks amidst falling government bond yields.

So, while the European business cycle is bottoming based on the improvement of leading indicators, the lagging data continues to point to a negative Q4 GDP print.

Job openings disappoint. US job openings started this labor market-dominated week off with a big downside surprise. The number of open positions decreased by more than 600 thousand to 8.783 million in October, falling to its lowest level since March 2021. Job openings have now decreased in eight of the ten months this year in a sign that the tightness of the labor market is easing.

ADP saw weaker hiring in November. This weakening labor market narrative got reinforced by Wednesday’s ADP release showing private employment (103k vs. 130k expected) rising less than expected in November. Companies scaled back hiring with the manufacturing sector reducing headcount to the lowest level since early 2022 and leisure and hospitality shedding jobs for the first time since 2021.

ISM PMI offers support. These two data points had reinforced the already priced-in Fed rate cuts for 2024 worth 125 basis points with investors continuing to rotate capital into government bonds as protection against a potential recession. However, while the job openings number did surprise to the downside, the ISM Services PMI increased from 51.8 to 52.7 in November. The employment index improved by 0.5 points and came in at 50.7, remaining in expansionary territory.

Softer labor market. Nonetheless, the labor market data has disappointed expectations this week. Besides job openings and the ADP’s private employment report, initial jobless claims have slightly picked up as well. The number of Americans filling for unemployment benefits remains low at 220 thousand. However, the number is still the second highest since September, showing that claims have started picking up again.

Global Macro

The view ahead

All eyes on policy makers. The next week will be all about the upcoming policy meetings in the US, UK and Eurozone with all three central banks expected to leave interest rates unchanged. However, the updated projections will be a key data point to watch in the face of markets pricing in significant policy easing for 2024.

The 14-day look ahead. A detailed analysis can be found in our weekly risk calendar.

Monday (11.12) –

Tuesday (12.12) – UK labor report, ZEW sentiment, US inflation,

Wednesday (13.12) – UK GDP, US PPI, Fed interest rate decision

Thursday (14.12) – SNB, BoE and ECB rate decisions

Friday (15.12) – Flash PMIs for Eurozone, UK, US, ECB staff projections

Monday (18.12) – Ifo business climate

Tuesday (19.12) – Canadian inflation,

Wednesday (20.12) – German consumer confidence, US consumer confidence

Thursday (21.12) – US GDP, US initial jobless claims, US Leading Index

Friday (22.12) – Japanese inflation

All dates GMT

Fed’s hiking cycle ended in July. The Federal Reserve paused its tightening cycle in July, after having raised interest rates eleven times to a 22-year high at 5.25% – 5.50%. Since then, policy makers have been on halt as inflation and economic momentum continued to cool. The next FOMC meeting on Wednesday will most likely end with policy makers officially concluding their almost two-year long tightening cycle without giving in to market expectations of policy easing coming in 2024.

Market pricing vs. the FOMC. Investors have priced in around five rate cuts from the US central bank for next year. We do think that the Federal Reserve will need to ease monetary policy to support the economy during the expected cyclical downtrend. Still, with core inflation seen above 2% throughout 2024, the labor market will be key in determining how much easing the Fed will deliver. Historically, easing cycles have been more aggressive in an environment of soft labor markets compared to tight ones, as the Fed’s intolerance for an increase in the unemployment rate has been a constraint for policy setting.

Goldilocks holds. So far, the soft-landing narrative has held up against the incoming data. Both inflation and economic momentum are continuing to soften. However, while the pace of the weakening has been enough for markets to feel comfortable pricing in rate cuts from the Fed, it was not sufficient to throw the soft-landing narrative over board. The US economic surprise index has fallen to its lowest level since June and the Atlanta Fed now sees US growth coming in at 1.2% for Q4. Both indicators are therefore well below their Q3 averages but clearly still positive. The same progress has been made on the labor market front with the closely watched V/U ratio (vacancies vs. unemployed) falling from its peak at 2.0 to 1.3.

Remaining cautious. We continue to expect the US labor market to weaken and for the US to fall into a recession based on the deterioration of leading indicators. This could give the Fed the justification to star the cutting cycle in Q2 and to deliver a cumulative easing of around 75-100 basis points next year, less than what is priced in.

ECB peaking at all-time highs. The European Central Bank has been the last of the G3 central banks to raise interest rates in response to rising inflation. Still, the cumulative tightening worth 450 basis points, going from a negative- to a high rates regime in just a matter of 15 months has raised the deposit rate at a record level. However, as Germany is likely to enter its second recession since 2022 and with inflation falling to 2.4% in November, the ECB will most likely hold rates unchanged for a third consecutive time.

Dovish comments move markets. Markets have continuing upping their bets on aggressive policy easing from the ECB and are now pricing in 5-6 rates cuts for 2024. The weakening of economic data has been the initial driver of these expectations, which had been followed by dovish ECB speak. German ECB member Isabel Schnabel’s comments about the remarkable fall in inflation making mor rate hikes unlikely moved yields and the euro lower.

Last shoe to drop. The ECB will release its new economic projections following the policy meeting on Thursday. We are expending the institutions economists to revise down their forecasts on both growth and inflation. Firstly, inflation for Q4 will most likely average less than what the ECB had expected (2.9%). Secondly, the ECB had not expected inflation to fall below 2% in 2025 back in September. Given the current path, the new projections could put inflation for 2025 below the inflation target, paving the way for a first rate cut in Q1 next year.

Bottoming from low levels. Leading indicators for the German and Eurozone economy continue to improve from low levels, suggesting a bottoming of the business cycle. However, prospects for 2024 remain subdued given high interest rates and the fiscal issued in Germany. German industrial production failed to grow for six consecutive months, while factory orders fell by 3.7% in October alone. We continue to expect inflation in the Eurozone to fall below 2% in the middle of next year, supporting the calls for policy easing from the ECB.

BoE to remain on hold. The Bank of England remained on hold for a second consecutive time at the November meeting, after having raised its policy rate to a 15-year high of 5.25% in July. Against the backdrop of inflation falling to the lowest level since October 2021, the manufacturing sector remaining in recession for 16 consecutive months and quarterly GDP growth averaging just 0.13% since Q2 of last year, we remain convinced that the BoE is done with its tightening cycle. The market currently prices in rate cuts worth 90 basis points for the BoE for 2024.

Hawkish pause. Recent comments from British policy makers suggest that the 6:3 (six members voting for a hold and three for a hike) will be replicated on Thursday. This could, at least for now, solidify the BoE as the most hawkish central bank within the G3 space and limit the markets resolve to price in more rate cuts for 2024. Both Governor Andrew Bailey and Deputy Dave Ramsden have recently said that (1) market pricing on cuts remains too optimistic and that (2) services inflation remains too high to consider policy easing. While we do see these stances easing early next year, this hawkish rhetoric could be enough to fend off investors for now.

Inflation falls from high levels. One reason for pausing its tightening cycle will be the slowdown of headline inflation from 6.7% to 4.6% and core inflation from 6.1% to 5.7% in November. The overall trend in the survey data looks promising, but not enough to fully convince the BoE of leaning into rate cutting speculations.

Survey data ambiguous. The British Retail Consortiums retail survey showed shop prices continue falling on a year-on-year basis, coming down from 15% in April to 7.7% in November. The same holds true for price pressures in the services sector, according to the survey from the Confederation of British Industry. However, the prices charged component of the UK services PMI survey jumped up to the highest level in four months, dampening the near-term optimism. National wide pay negotiations will be completed in Q1 next year with the approved 10% rise in the national living wage (nlw) getting implemented.

FX Views

Dovish Europe vs. hawkish Japan

USD Helped by external factors. The US dollar has found its footing against the euro and pound but is only slightly up on the week on a trade weighted basis due to the strength of the Japanese yen. Weakness in Europe has helped the Greenback establish a short-term bottom against the euro, as the fall in EUR/USD and global oil prices rippled through to other majors like the CAD, AUD, NOK, and GBP. The US Dollar Index (DXY) is on track to rise for the first week in a month as EUR/USD fell from $1.10 to now $1.0770. GBP/USD has held up a bit better on expectations that the Bank of England would not be as aggressive in its policy easing cycle next year and has fallen from $1.2710 to now $1.2570.

EUR Dovish ECB prompts euro selloff. An unexpected ECB tilt to the dovish camp ignited a euro selloff on the back of an already weak price momentum. Isabel Schnabel admitted that further rate increases are “rather unlikely” given recent inflation developments. Fellow policymakers Kazāks and Villeroy followed suit and opened a window for policy easing discussions in H2 2024. Markets are still betting on earlier rate cuts and attach a 70% probability for such an outcome in March. On the data front, Eurozone GDP contraction was confirmed in Q3, but coincident and leading indicators point to a gloomy outlook for Q4 providing little support for the common currency. EUR/USD fell by 1% to a 3-week low at $1.0754 – the fourth largest weekly depreciation of the year. Meanwhile, EUR/JPY depreciated by close to 3% w/w in what was the largest decline since end of September 2022, driven by BoJ policy adjustment speculation. With five central banks decisions due next week, volatility will come from their respective forward guidance comments and subsequent differentials in policy rate expectations will dictate market dynamics.

GBP Eyeing $1.25 level. Continued selling momentum saw cable lose 1% of its value this week as sterling retreated from overbought territory and the ongoing price dynamics continue to be largely driven by US developments. On the data front, UK private sector output expanded for the first time since July, but the property sector continues to struggle as construction output remained in a deep contractionary territory. Amid investors’ weaker economic growth and falling inflation expectations, yields on the mid and long end of the bond yield curve have fallen to their lowest level since May. Markets see the Bank of England (BoE) cutting interest rates less aggressively than its G3 peers next year as core inflation remains more than double its 2% target. The favourable expected interest rate differential and a recent dovish ECB tilt had sterling testing fresh four-month high against the euro around the $1.6900 level, while GBP/CAD surrendered some ground on the back off a hawkish BoC hold.

CHF Franc’s strength to cause SNB headache? The Swiss franc was on track for its first weekly loss versus the US dollar in four weeks as the USD/CHF rebounded following a 6.3% fall since early October. That said, the Swiss franc remains medium-term bullish, with the USD/CHF below both the 100- and 200-day moving averages. The CHF was stronger in most other markets. The Swiss franc climbed to five-week highs versus the British pound. The EUR/CHF fell to major multi-year support at 0.9400 – the pair has only ever traded below this level briefly during its January 2015 “flash crash” after the Swiss National Bank suddenly removed its euro peg. The Swiss National Bank meets on Thursday in its final monetary policy decision of the year. Most forecasters expect the SNB will keep rates at 1.75% but the ongoing CHF strength – particularly versus the euro – is also likely to be on the central bank’s agenda.

CAD Hawkish BoC hold provides temporary support. Bank of Canada (BoC) held its overnight rate at a 22-year high of 5%, coupled with a hawkish stance . Despite acknowledging a slowdown in the economy and a general softening of prices, the central bank hinted at a possibility of another hike amid concerns over sticky inflation rate. Investors didn’t buy that and now speculating about a potential rate cut trajectory. The market implied probability of a rate cut in March currently stands around 40% and over 110bps of cumulative rate cuts have been priced in for 2024. While the rate decision was generally good news for the Canadian dollar, external factors took precedence and Loonie depreciated towards the $1.36 level against the US Dollar. So far in Q4, CAD is down against most G10 peers, with most notable depreciations against SEK and CHF in the range of -5% and -4% respectively. More recently, CAD/EUR is trading close to its 1-month high of 0.6830 amid broad euro weakness on the back of a dovish ECB tilt. In the short term, the Canadian dollar could find support near the 50-day SMA $1.3510 and halt its fifth consecutive daily decline.

AUD RBA turns dovish. AUDUSD is trading around 0.66, holding above the psychological 0.65 level as commodity prices found support over the past week. From a positioning perspective, the pair remains in the middle of its 6-month range after recovering from oversold conditions last month when it hit a 2-year low below 0.63 handle. Following Tuesday’s RBA meeting where there was no hint of the hawkishness that market was expecting, AUD was the biggest underperformer in G10 FX, particularly against NZD which was supported by a more hawkish-than-expected RBNZ in the previous week. In the near term we remain neutral to mildly bearish on AUDUSD with risks skewed to the downside. The pair needs to break below the recent swing lows around 0.6450 to open the door for a retest of 2022 lows into year-end. On the upside, a move above 0.6850 is needed to signal upside momentum is returning. All eyes on Westpac Consumer Confidence, PMI, and November employment next week.

CNY China credit outlook downgrade. USDCNY has fallen from nearly 7.30 to around 7.15 in recent weeks. The CNY’s rally came despite further disappointing economic data out of China and persistent property market weakness, adding to medium-term downtrend pressures. From a positioning lens, short-term momentum indicators are oversold. The USDCNY fix continues to be below market forecasts in a sign the People’s Bank of China is attempting to maintain the RMB following Moody’s outlook downgrade on growing debt but at a slower pace than in recent months. Currently holding the key 7.15 level, risks seem balanced for USDCNY heading into year-end. But further evidence of economic slowing could easily pressure the yuan and boost USD/CNY. FX reserve data will also be critical to gauge PBoC resolve. Next week, key data PBoC MLF announcement, house price index and retail sales will be out.

JPY Speculation rife around BoJ policy shift. The Japanese yen saw its biggest one-day gain in a year as Governor of the Bank of Japan Kazuo Ueda appeared open to questions about rate hikes during a key speech to the legislature. Rather than brushing the idea off out of hand, Ueda pointed out the several methods the BoJ may use to tighten. He spoke about altering both the overnight rate and the tiering structure. In the near term we’re neutral on USDJPY given mixed signals from fundamentals. But we maintain a core medium-term bearish view that a cyclical top is likely falling into place below the 150 level as markets bring forward expectations for Japan’s policy normalization. A break below the 142 swing lows would confirm upside exhaustion and open the door for a move toward 135. Looking forward, all eyes are on Tankan Big Manufacturing Index, Machinery Orders and Industrial Production next week.