The latest inflation data continues to point in the wrong direction from the Fed’s perspective, as the fifth relevant inflation print came in hotter than expected.

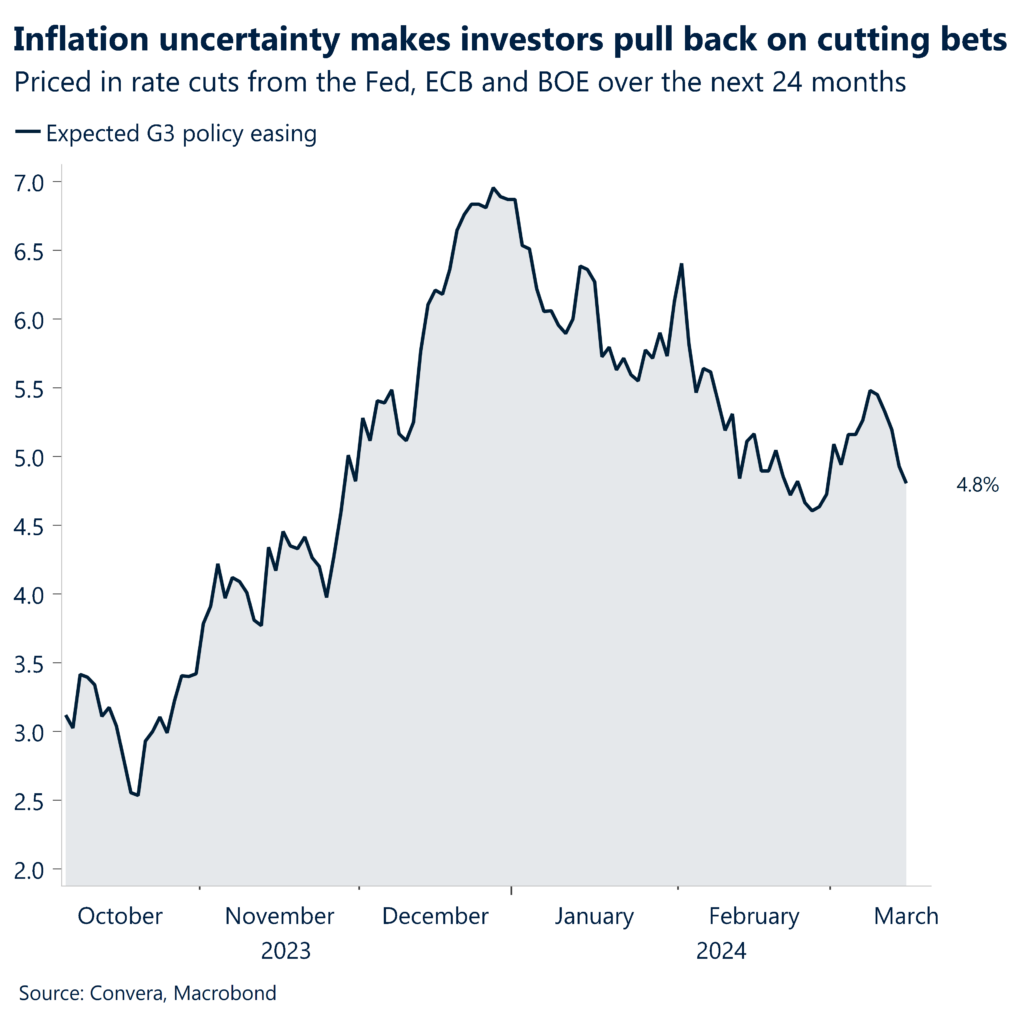

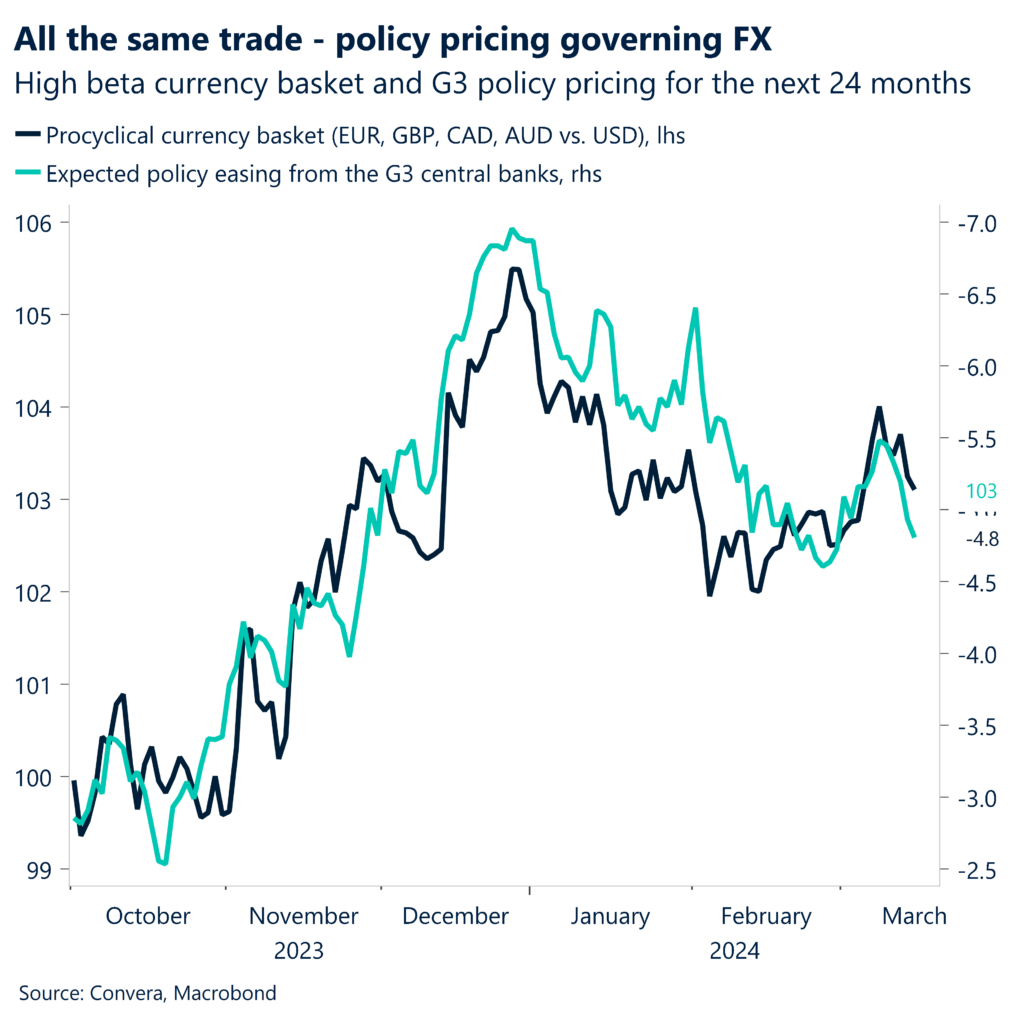

Market pricing is now back in line with the FOMC’s own rates projections, showing three rate cuts for 2024, down from seven at the beginning of the year.

The orderly pullback in easing expectations has so far defined the first quarter of 2024 and has seen the G3 10-year government bond yield rise from 3.10% to 3.60%.

The US dollar has risen against over 60% of its global peers this week. EUR/USD retreated from 7-week highs and GBP/USD from 7-month highs.

Global equity markets extended their March gains and closed out their 10th consecutive week in positive territory, having risen by 23% since November

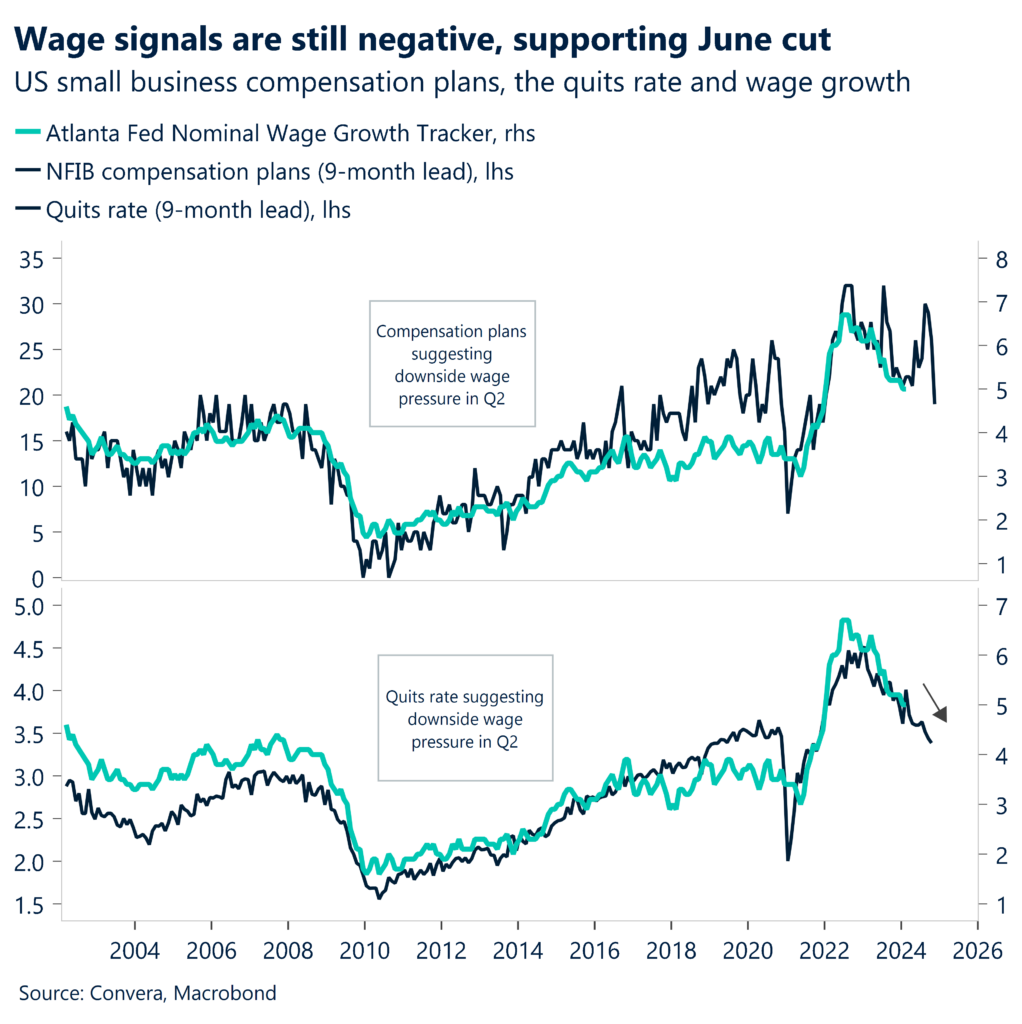

The recent data flow confirms the Fed’s cautiousness to cut before June. However, retail sales and the NFIB print show that the US economy is losing momentum.

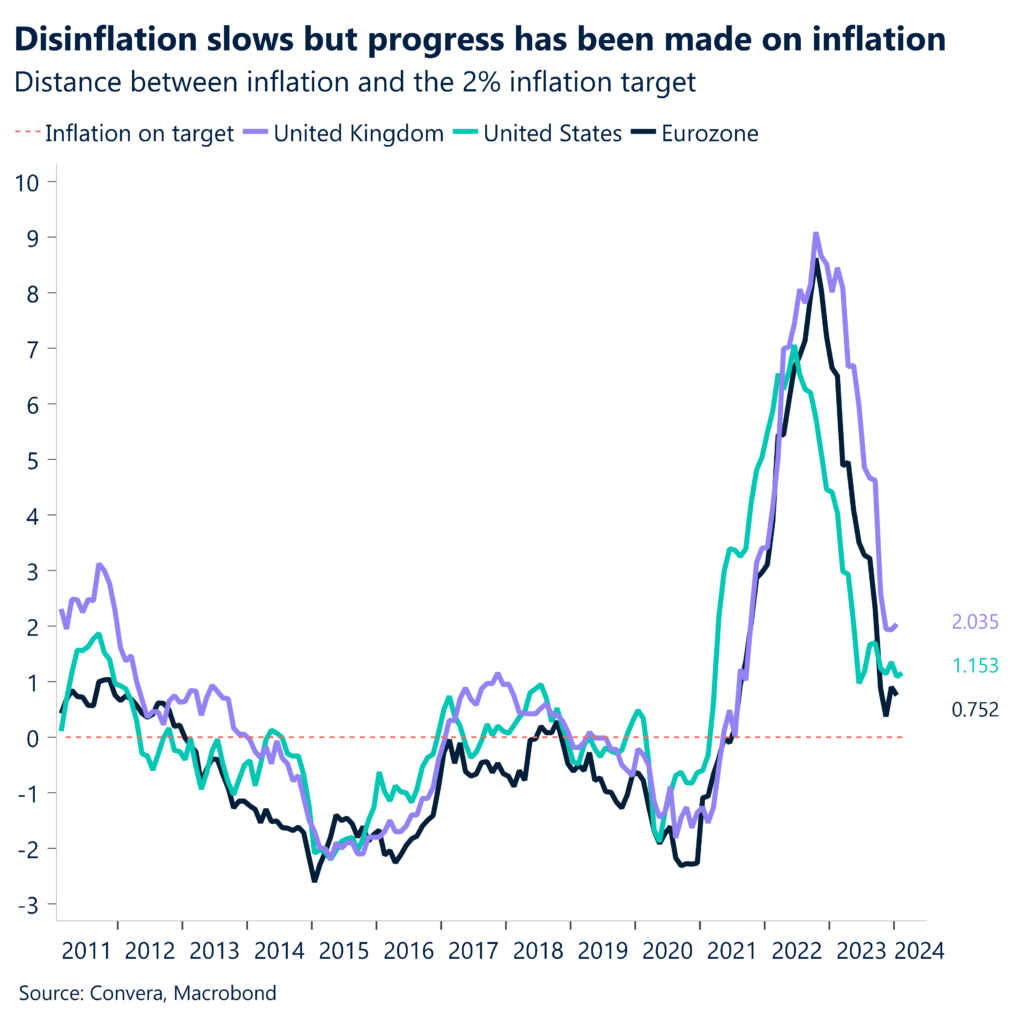

Our constructive view sees inflation convergence to 2% in both the Eurozone and UK in some months. Expect the Fed, ECB and BoE to cut interest rates in June.

Britain’s economy resumed growth in January after experiencing a shallow recession in the second half of 2023. Wage growth has slowed further.

Global Macro

More confidence on inflation needed

Less easing. Market pricing is now finally back in line with the FOMC’s own rates projections, published via the dot plot back in December, showing three rate cuts for 2024. With government bond yields rising for the fourth day in a row against the backdrop of the inflation surprises, discussions have emerged about the upcoming dot plot next week showing only two rate cuts for this year. This remains a threat for investors holding risk sensitive assets hoping for a quick pivot from the Fed. As pricing between the central banks has converges, so too have the easing expectations for the ECB and BoE fallen last week.

Inflation still an issue. We think not for long. The main culprit of falling easing bets has been the slowdown of the disinflation process in the developed world. Core inflation rates continue to fall in the US, UK and Eurozone, albeit at a slower pace. While the consensus and central bank forecasts see the disinflation trend to continue throughout the year, more confidence is needed amid the ambiguous data to start the monetary easing cycle. This uncertainty has helped the dollar sustain its positive year-to-date performance. We have a constructive view on inflation and see annual CPI rates convergence to 2% in both the Eurozone and UK around the middle of the year. Expect the Fed, ECB and BoE to cut interest rates in June.

Orderly markets. This so far orderly pullback in easing expectations has so far defined the first quarter of 2024 and has seen the G3 10-year government bond yield rise from 3.10% to 3.60% year-to-date. These higher yields have limited the Greenback’s depreciation but have failed to meaningfully impact equity markets in a negative way. We continue to note that volatility and risk indices remain depressed. The euro risk premium – difference between Italian and German yields – has fallen to its lowest level in 27 months, the ECB’s systemic risk index remains near record lowest and multiple regional equity benchmarks sit comfortably at all-time highs.

Regional outlook (US)

Fed in no rush to cut with inflation on the rise

Inflation beats estimates. US inflation came in hotter than expected once again in February, confirming the increase in consumer prices from the month prior. The main surprise came from core inflation posting a second consecutive monthly print of +0.4%, putting the annual growth rate at 3.8%. February is shaping up to repeat the hot numbers from the prior month with consumer- and producer prices once again coming in above consensus this week. The latter rose by 0.6% on the month, raising the annualized growth rate from 1.0% to 1.6%.

Low jobless claims. A separate report showed initial jobless claims remaining at historically low levels (209k), supporting the thesis that the easing of the labour markets tightness seen via other indicators is happening at a moderate pace.

Weaker sales. Retail sales did rise less than expected in February (0.6% vs. 0.8% expected), with the January print being revised down from -0.8% to -1.1%. Consumer spending is expected to slow down going into Q2 as savings rates are depleted and higher borrowing costs start working their way into household finances.

Wages to continue descent. Flying under the radar, but arguably more important, was the NFIB survey of small businesses, which offered investors some relief as the compensation plans of companies – a leading indicator for wage growth and therefore inflation – ticked down to its lowest since the beginning of 2022 in February. While the Q1 reflation has dampened hopes of a March or May rate cut, June is still seen as the beginning of the easing cycle.

The macro data confirms the Fed’s cautiousness to cut before June. However, retail sales and the NFIB print show that the US economy is losing momentum.

Regional outlook (UK)

Out of recession, but watch the labour market

Positive January. After falling into a technical recession in the second half of last year, the UK economy rebounded in January, registering modest GDP growth of 0.2%, whilst the rolling 3-month GDP only shows a very small contraction. Momentum is likely to remain weak in the near-term, but the economy seems to be showing enough signs of improvement, which is persuading investors that the Bank of England may have to keep interest rates higher for longer than its peers.

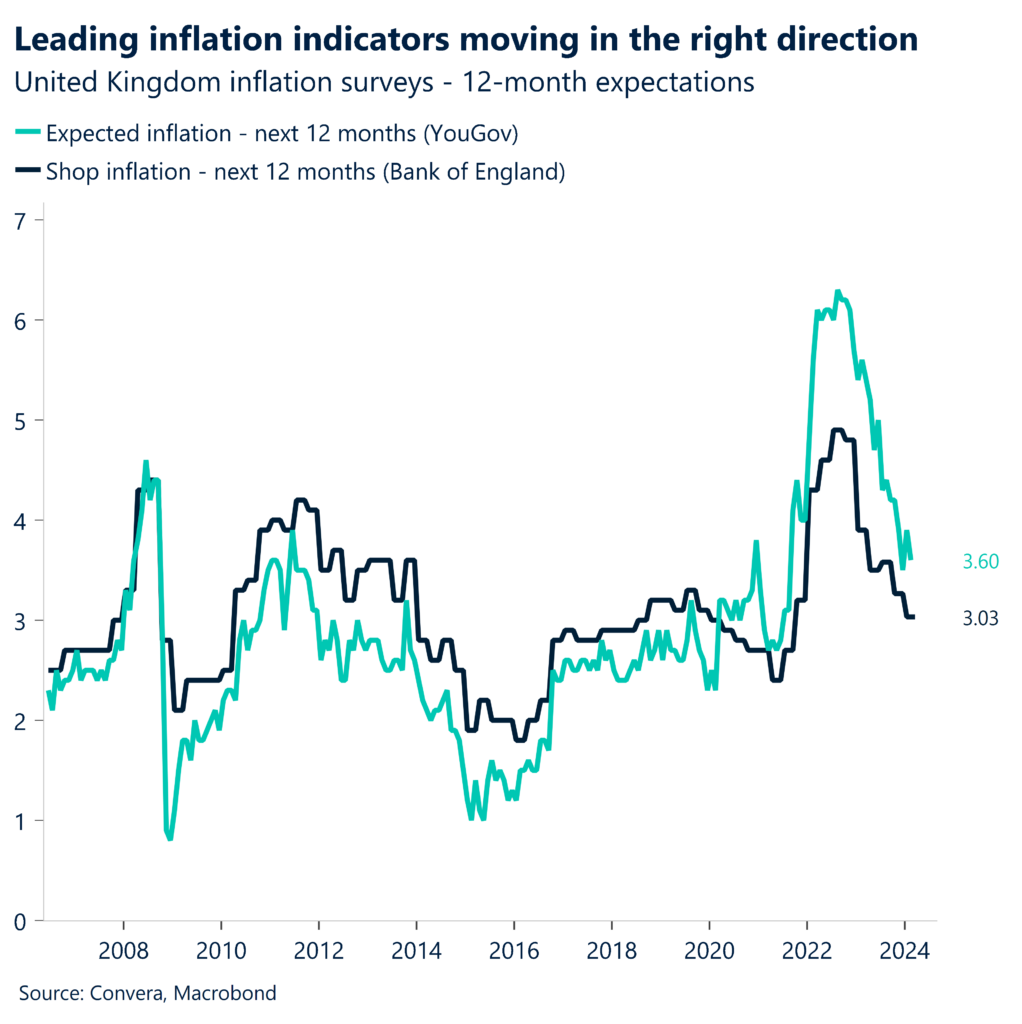

Wage growth slows. British wages excluding bonuses grew at their slowest pace since October 2022, while the unemployment rate edged up unexpectedly, easing inflation worries. Survey data from the Bank of England and YouGov showed both supermarket prices and inflation expectations for the next 12 months fall as well in February. Nevertheless, wage growth remains well above the rates consistent with 2% inflation, whilst survey data has hinted at a recovery in the economy, with private-sector growth at a nine-month high in February.

Rising jobless rate. The unemployment rate unexpectedly ticked up from 3.8% to 3.9% in January and the number of payrolled employees in February rose 20k, below the forecast of 25k. The pace of average weekly earnings (5.6%) came in lower than expected (5.7%) as well, which is good news for the Bank of England, but more progress needs to be made before rate cuts are delivered.

The pace of the disinflation remains too slow for the BoE to consider a cut before the June meeting against the backdrop of the uptick in economic momentum seen in January and February.

Regional outlook (Eurozone)

Weak data but push against cuts before June

Consensus about June. A consensus appears to be forming among Governing Council members on the timing of the ECB rate cuts with June emerging as the most likely contender to kickstart policy easing cycle. In an interview, Council Member Robert Holzman – among the most hawkish rate setters – confirmed that a rate cut is more likely in June, than April, but does not remain a done deal. While the ECB remains optimistic about the inflation progress thus far, “there are some residual doubt” about the convergence to 2% in 2025 as per latest ECB staff projections.

Still some room for repricing. The Governor of Bank of Greece argued that the ECB must lower borrowing costs twice before its August summer break and another two times before the end of the year, signalling a cumulative of 100bps rate cuts are on the cards by year-end. The policymaker highlighted that keeping rates at historic highs could foster a monetary policy environment that is too restrictive, hindering an already difficult economic recovery across the bloc. Consequentially, market participants moved to price in additional monetary easing, expecting over 90bps of rate cuts by end of 2024.

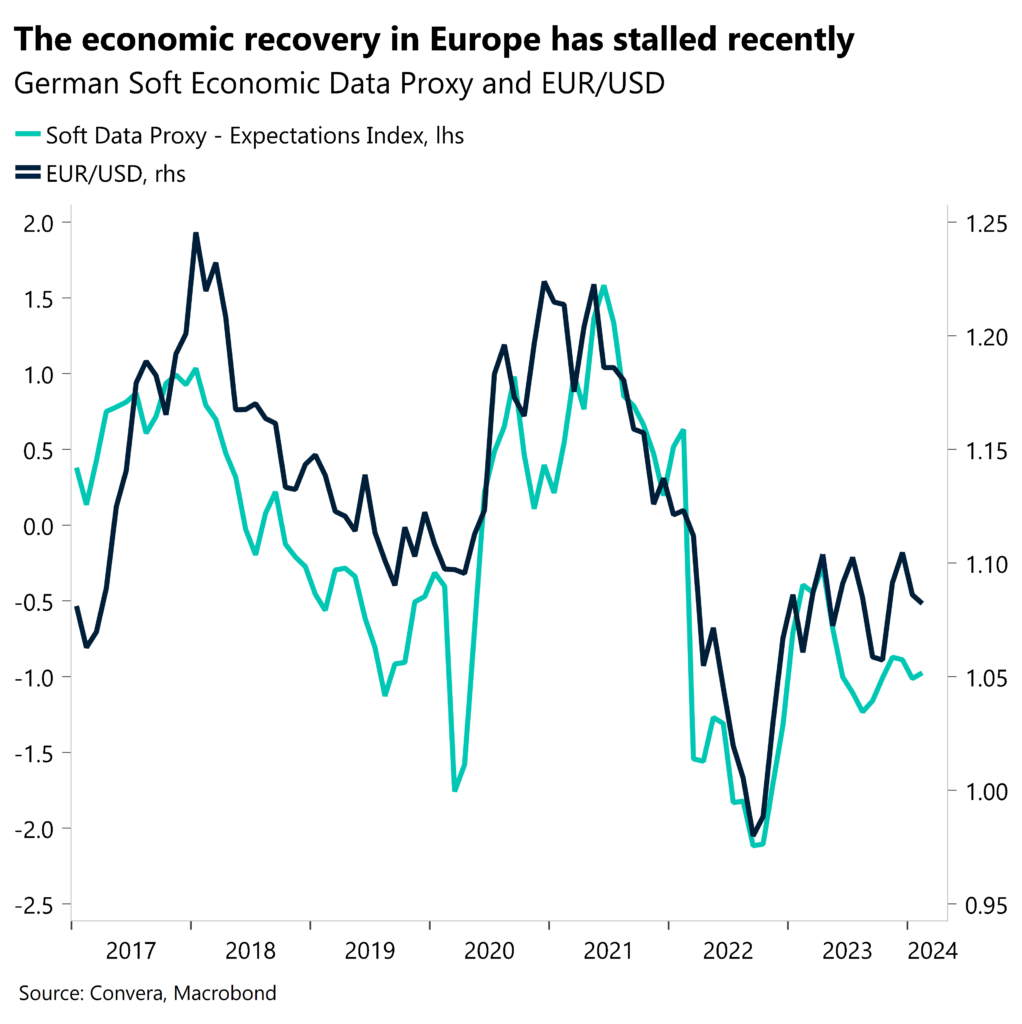

Industrial weakness. Although largely ignored by the markets, the latest Eurozone industrial production print plunged by 6.7% y/y in January – the sharpest contraction in activity in 10 months, and the second largest decline since the aftermath of the COVID-19 outbreak, primarily driven by a 14.5% drop in the production of capital goods. This means that Q1 GDP is under pressure again as the Eurozone economy continues to broadly stagnate.

The ECB is set on delaying the start of its easing cycle to June and has been aided in its cause by Fed cuts being postponed and rebound inflation at the beginning of 2024.

Global Macro

Looking for subtle shifts from policy makers

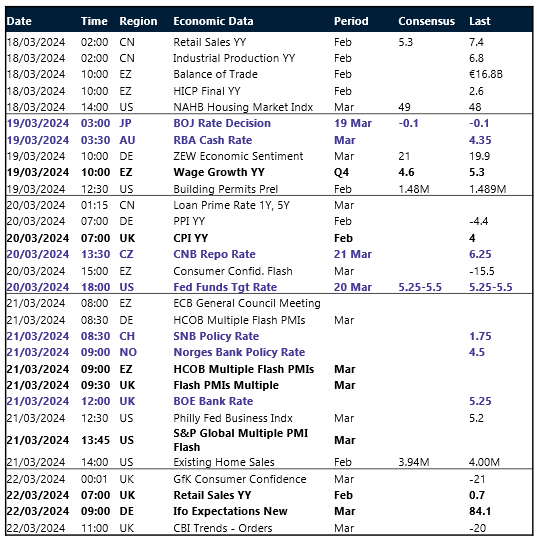

Watching the dots. The Federal Reserve is expected to hold policy rates unchanged next week. The attention will fall on the summary of economic projections (SEP) and the dot plot, which could show the Fed’s preference of only cutting interest rates two times this year. While not our base case, this would significantly impact market pricing. In Europe, we expect a majority of the Monetary Policy Committee to vote to keep Bank Rate at 5.25% next Thursday. But sticky pay growth in the private sector, and recent comments by MPC members point to another three-way split in the vote.

Setting the scene. The less market moving decision in Norway should see no change to policy rates as well. However, the decision in Switzerland could be a close call between leaving policy unchanged and cutting rates. In Asia, the Japanese and Australian central banks will be closely watched. The year started out with investors expecting the Federal Reserve to cut interest rates in March. However, the recent macro and inflation data has postponed these expectations to June. Next week will therefore be about setting the scene for a potential cut from the G3 central banks in Q2.

First March data. The purchasing manager indices for various countries will give us a first insight into the economic momentum in March. The leading indicators for the US, UK, and Eurozone have been market moving in the past and will most likely continue to be so. Apart from the PMI’s, wage data in the Eurozone and consumer prices in the UK might give the Bank of England the last data point to consider before its decision.

FX Views

Dollar back on top as data fuels rates worries

USD Strong rebound after hot inflation. The US dollar has risen against over 60% of its global peers this week, a huge contrast to the mere 2% it rose against last week. The dollar index snapped a 3-week losing streak after hotter-than-expected US producer and consumer price data led to markets pricing three cuts as opposed to four (last week) by the Fed in 2024. After falling to a 1-month low recently, US yields have marched higher with the 10-year yield on track for its biggest weekly rise since October last year with the dollar index accordingly rising in line, scoring its best daily performance in a month on Thursday and on track for its biggest weekly rise since mid-January. The hard US data of late is not consistent with a substantially weaker dollar any time soon and we could see this rebound of the dollar index stretch towards 104 in the near-term given the ongoing uncertainty around the timing and scale of policy easing as a result. Traders are also considering the risk of a potentially more hawkish Fed dot plot next Wednesday, signalling two cuts for this year, which would likely hurt risk assets and support further USD strength. However, with our constructive view on inflation and expected rate cuts from the summer, we remain lean bearish on the dollar over the medium term.

EUR ECB signals readiness to cut rates in June. EUR/USD retreated from its 7-week high as the US dollar firmed after the release of US inflation showed inflationary pressures were higher than expected in February. Several ECB policymakers expressed readiness to cut policy rates before the summer break, with ECB’s Stournaras signalling a cumulative of 100bps rate cuts are on the cards by year-end. Until then “there are some residual doubt” about the inflation convergence to 2% in 2025, namely stubborn wage growth pressures, which will be either confirmed or negated with a wage growth report due on Tuesday. In the meantime, the bloc continues to struggle under restrictive monetary conditions with the latest EZ industrial production recording the sharpest contraction in activity in 10 months and hindering Q1 GDP recovery. For now, EUR/USD is currently licking wounds at a support level near $1.0880 (14-day SMA), and is looking to enter the FOMC week with softer momentum.

GBP Overall G3 easing bets steering sterling. After its biggest weekly advance of 2024 last week, the British pound has fallen around 1.3% from its 7-month high of $1.2893 versus the US dollar. GBP/USD failed to hold above its 200-week moving average but remains in positive territory year-to-date. US data was the main driver of this week’s trends, whilst domestically we saw UK wage growth pressures continue to ease, though policymakers will be looking for more progress before cutting interest rates. UK GDP rebounding in January supports the BoE’s stance for rates to stay restrictive for longer too. Given the expected path of monetary policy isn’t too dissimilar amongst the G3 central banks, we think the overall extent of monetary easing is more important now. The more rate cuts are being priced in, the better the growth prospects for high beta currencies, like the British pound, versus the US dollar. Thus, despite a hawkish repricing of UK rates seen this week, the overall hawkish repricing of G3 policy has hurt the pound. Next week, UK inflation and the BoE’s policy decision are key events for GBP traders, though no change to rates or forward guidance is anticipated.

CHF Weakness continues as SNB eyed. The Swiss franc erased its prior week’s gains against the US dollar, meaning it has now fallen over 4.5% this year, the second-worst performance among G10 currencies. Meanwhile, the franc is on course for six weekly drops in a row versus the euro as the common currency eyes a bullish close above its 50-week moving average. The franc’s 3.6% decline year-to-date marks its worst start to a year on record versus the euro. The positive-risk backdrop of late has not helped the safe-haven franc, but its weakness is mostly because the SNB is no longer pursuing CHF-strengthening policies, such as selling FX reserves, now that inflation is under control. This week, we saw Switzerland’s producer and import prices fell 2% y/y in February, easing from a 2.3% decrease in January, but marking the tenth consecutive period of decline. Markets are betting the SNB could be the first out of the G10 central banks to cut interest rates, though the probability of a cut at its policy meeting next Thursday has fallen from 66% at the start of the month, to 33% today. Overall, the Swiss franc has only appreciated against 20% of the world’s currencies so far this month, after appreciating against just 14% in February and we believe it will continue to underperform through 2024.

CNY China’s property sector reforms face headwinds. China has reiterated its long-standing stance on curbing speculative activity in the housing market, dampening hopes for further easing of purchase restrictions in major cities. Authorities acknowledged capital constraints and insolvency issues plaguing some property developers, suggesting a need for restructuring or bankruptcy proceedings. USD/CNH is nearing initial upside targets (re Weekly Jan 19th publication: targeting 7.239-7.2665 resistance) after consolidating between November-January. Looking ahead, investors will closely monitor key economic indicators such as fixed asset investment, industrial production, retail sales, and the 5Y Loan Prime Rate for insights into the health of the Chinese economy.

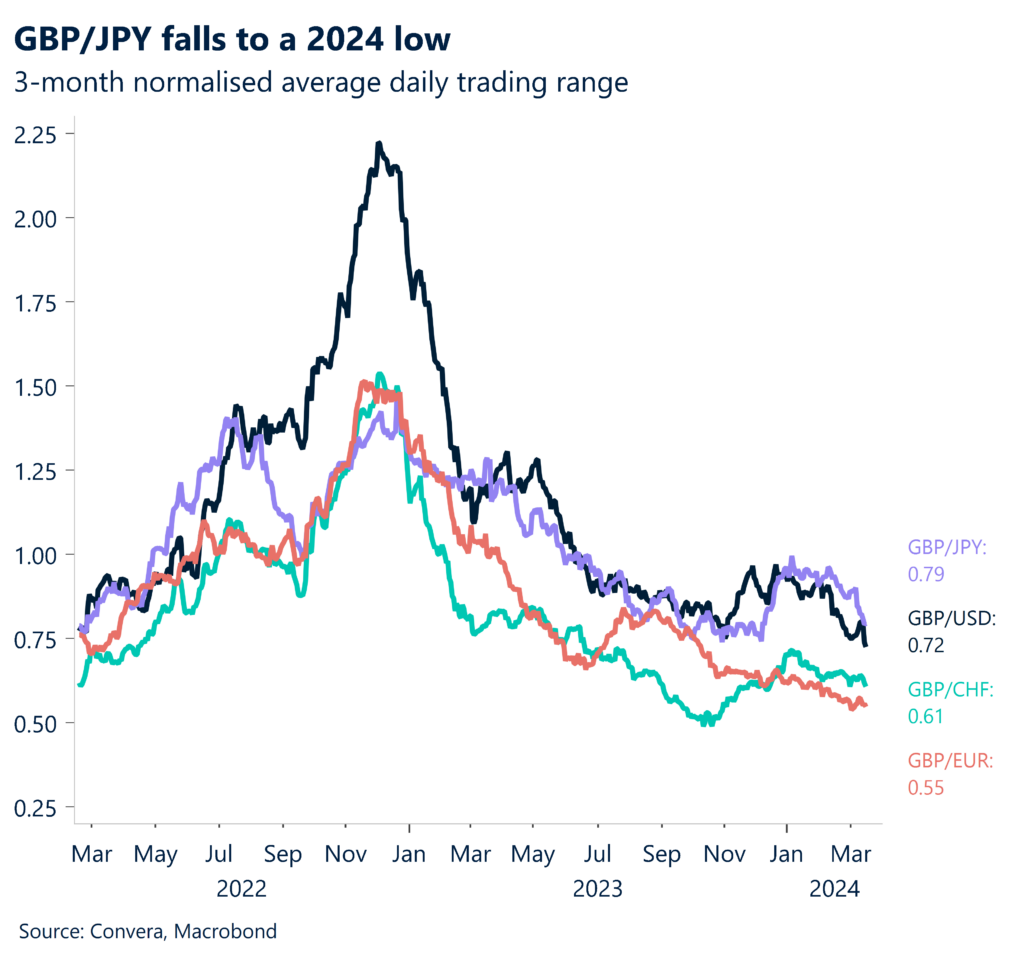

JPY BoJ navigates yield curve challenge amid policy shift. While markets speculate on the timing of the Bank of Japan’s potential rate hike, the central bank’s primary focus remains on its yield curve control (YCC) policy. Managing short-term rates is relatively straightforward, but exiting the YCC framework poses a significant challenge, as it could leave long-term bond yields unanchored. The BoJ is expected to provide guidance on bond purchases and YCC next week, potentially shifting away from YCC as a formal policy while implementing measures to maintain curve and yield stability. Looking at GBP crosses’ volatility, in particular GBP/JPY (RHS chart), the volatility has been on the low end, as have other crosses for GBP. On the technical front, the USD/JPY pair’s rally has lost momentum near the 151.945 resistance level, with a break below 148.815 potentially derailing the uptrend. Key economic data to watch includes the BoJ rate decision, industrial production, trade balance, and inflation figures.

CAD Back on the bearish trend. USD/CAD made a strong comeback breaching the C$1.3500 level after encountering fresh buying on the back of hot US inflation reports and lower than expected initial jobless claims. A recent spike in WTI crude oil futures, underpinned by signs of robust US demand and a bullish outlook on global consumption for this year, provided limited support for the Canadian dollar and USD/CAD is looking to post the largest weekly gain (+0.4% w/w) since beginning of January. Going to next week, markets are positioned for less aggressive rate cuts by the BoC than the Fed, but a downside surprise in next week’s Canadian inflation reports could bring the pricing in line with its US counterpart and further weaken the Loonie. USD/CAD could experience more positive trading sessions in the near term, particularly if the bulls break through the resistance of C$1.3535.

AUD Aussie under pressure amid household strain. The Reserve Bank of Australia’s assistant governor highlighted the significant burden that persistently high inflation levels are placing on Australian households. With some families also grappling with the impact of interest rate hikes, the central bank is expected to maintain its policy rate at 4.35% in the upcoming meeting despite recent inflation data aligning with projections. While the AUD/USD attempted a rebound after buy signals in February, the momentum fizzled around resistance near 0.6611-0.6640. Further upside appears limited, with the potential for a deeper pullback towards the Q4 2023 low of 0.6269 in the coming months. Key data to watch next week includes the RBA rate decision, employment figures, and the unemployment rate.