Something for everyone. Investors are convinced that monetary policy easing is coming this year, just not as early as the consensus had been expecting going into 2024. The first quarter is therefore shaping up to be characterized by two distinct developments. (1) The pickup in government bond yields on the short end of the curve due to the paring of interest rate cuts and (2) the continued rise of equity markets off the back of the global tightening cycle having peaked.

Uncertainties loom large. While cross-asset volatility remains depressed compared to historic averages, investors continue to be troubled by a lot of uncertainties. Geopolitical tensions and their implications on the inflation outlook remain within the top three risks in most investor surveys. And the probability of inflation settling above the Fed’s 2% target this year has clearly risen over the past few weeks. Adding to that the uncertainty on the Chinese growth outlook and the European and US elections coming up and we can say that markets are currently underpricing the underlying risks to the consensus.

No rate cuts in March. The last two weeks gave us the first lagging and leading data points for the months of January and February. In conclusion, base effects continued to drag down annual inflation in most developed countries. And while the monthly growth rates did surprise expectations in the United States, investors seemed to look through the January data, which is plagued by revisions and multiple one-off effects. Still, the upside surprises were enough to reduce the probability of a March cut by the Fed, BoE or ECB to practically zero.

Global Macro

Looking at two sides of one coin

Paring back easing bets. The big macro theme in early 2024 has been the paring of G3 policy easing bets against the backdrop of somewhat rebounding inflation rates and growth 1) remaining resilient in the US and 2) bottoming out in China and Europe. Investors have reduced their overall rate cutting expectations by a third so far this year and are pricing in policy easing worth 460 basis points from the Fed, ECB and BoE over the next 24 months. This development has pushed bond yields across the developed world higher and has supported the Greenback, while not denting the appeal of equities.

Bond vs. equity markets. One reason for this divergence between equities and bond yields can be explained by those two asset classes focusing in on different aspects of the monetary policy cycle. Bond markets have priced in the fact that rate cuts have been postponed, while equity markets are benefiting from the continued pricing in of rate cuts worth 460 basis points over the next two years.

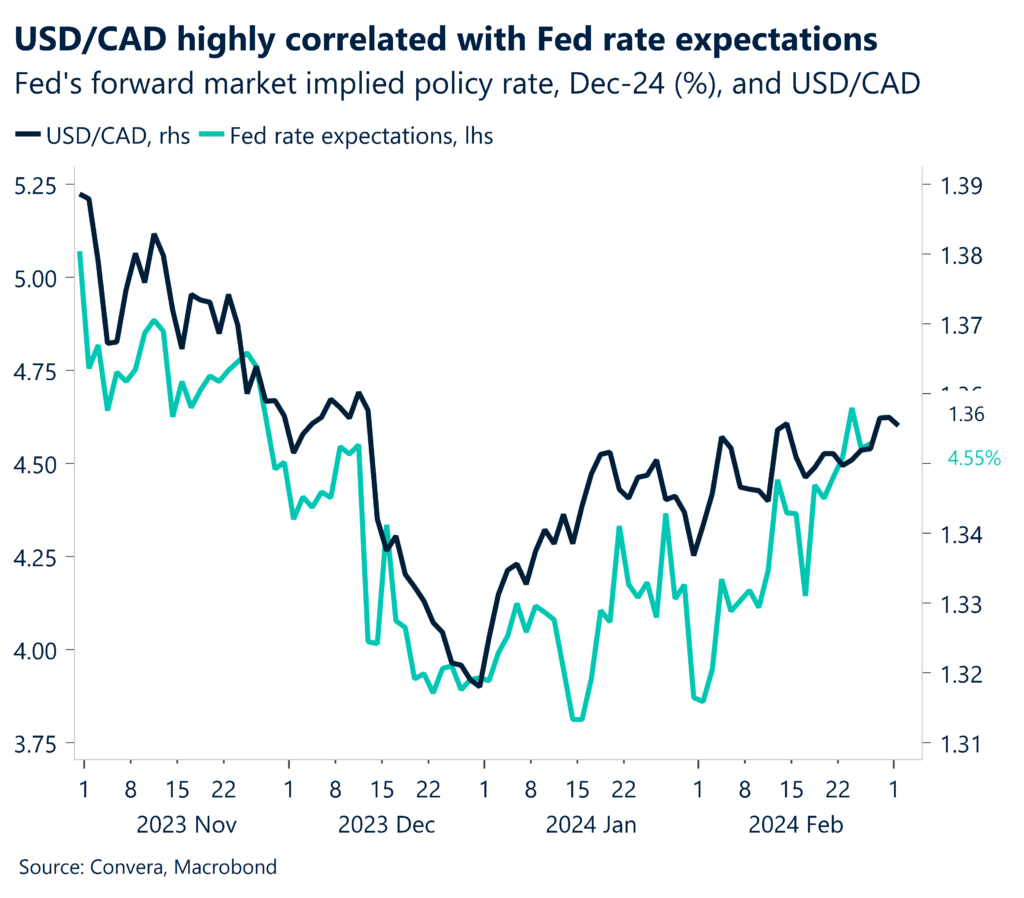

FX stuck in the middle. The currency market has been somewhat stuck in the middle between bonds and equities. The rise in bond yields since the beginning of the year has been risk-negative and supportive of the Greenback. However, rising stock prices and the synchronization of yields between countries have kept a lid on the strength of the US dollar. While EUR/USD has turned negative year-to-date following the reduced probability of a Fed March cut, the repricing lower has been limited so far.

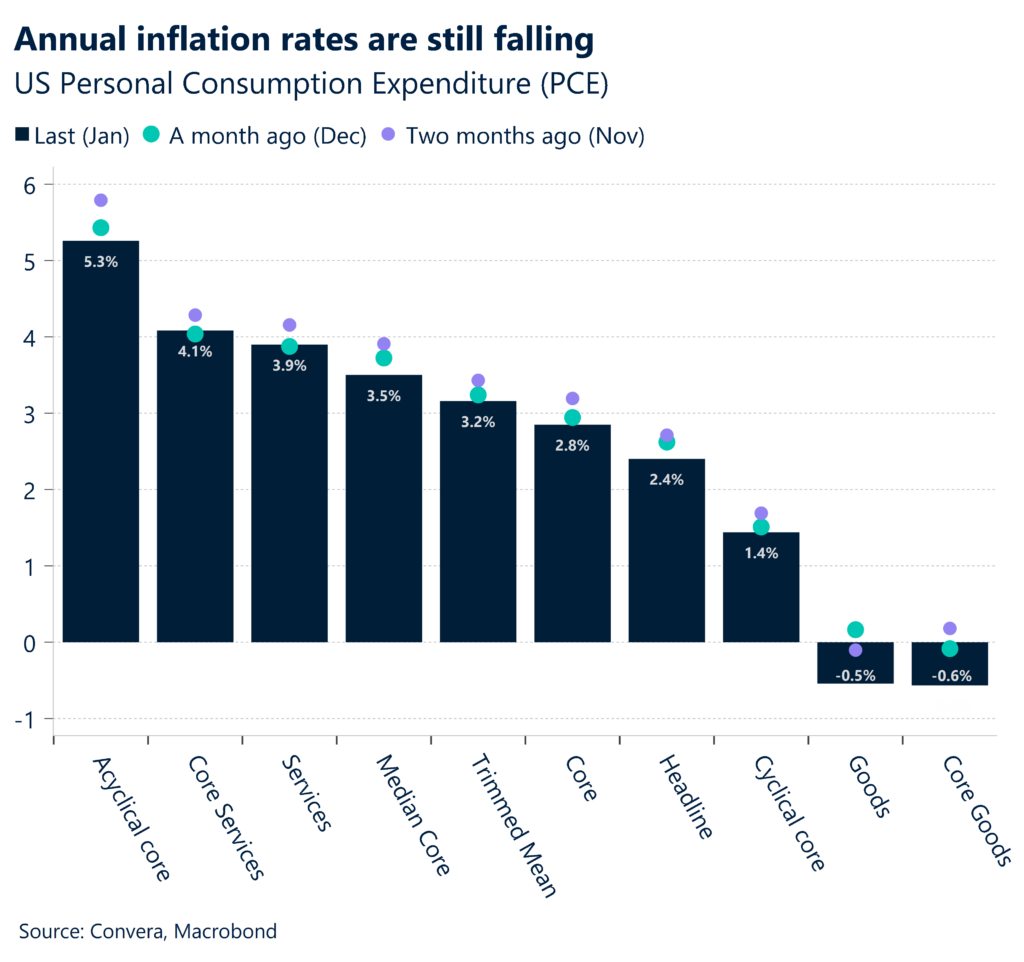

Inflation not screaming rate cuts. The Fed’s preferred inflation gauge (core PCE) started the year on stronger footing, rising by 0.4% in January. The largest monthly rise in more than a year had overshadowed the base-effects driven fall of the annual core inflation rate from 2.9% to 2.8%. One metric of particular interest to Fed chair Jerome Powell, the services inflation excluding housing and energy, even rose by 0.6% from a month ago, the most in 22-months. However, the highly anticipated report has not been able to move the needle much when it comes to market’s pricing of future Fed policy.

Looking beyond January. While the trifecta of rebounding inflation prints in the form of the CPI, PPI and PCE reports has now been completed for January, it seems that investors took comfort in the fact that inflation did not exceed economists’ expectations. January is also seen as being plagued by multiple one-off factors as companies adjust prices at the beginning of the year, which means that investors continue to patiently await new data to strengthen their conviction trades.

Rate cuts penciled in for June. The broad consensus still sees inflation rates falling and paving the way for the ECB and Fed to cut rates in June. With most Fed officials uniting around a cautious and slow approach to cutting interest rates, and data coming in mostly more robust than expected, markets have largely priced out a rate cut at both the Fed’s March and May meeting and the chance of a cut in June sits around 50%.

Not all that rosy. Investors largely brushed off weaker than expected data from the US. Durable goods fell 6.1% last month, missing expectations and marking the most substantial monthly decline since April 2020. US new home sales rose less than expected despite a batch of downward revisions in earlier months and the Conference Board’s consumer confidence index fell from 110.9 in January to 106.7 in February.

Sentiment remains weak. In the Eurozone, the latest economic sentiment indicator declined to 95.4 in February 2024, down from January’s revised figure of 96.1 and falling short of market expectations. Sentiment remained subdued as businesses grappled with inflation, rising borrowing costs, and weak external demand. Confidence deteriorated among manufacturers, service providers, retailers and constructors, but improved slightly among consumers. Across regional breakdown, the index deteriorated the most in Italy and Germany.

Consumer confidence bottoming. German consumer morale improved slightly heading into March from February’s 11-month low. However, the headline index has remained below its long-term average for a record of 28 consecutive prints – the longest pessimistic streak. Income expectations hit their highest since February 2022.

Lending growth slows further. This trend extends to the wider bloc, as data indicated that Eurozone bank lending growth slowed to a near 9-year low, further underscoring the significant deceleration in the bloc’s economy due to the European Central Bank’s unprecedented tightening measures implemented over the past months. The overall private sector credit growth, encompassing both households and non-financial corporations, stood at only 0.4%.

Cautiousness from Lagarde. This week, ECB President Christine Lagarde cautioned the markets yet again against early rate cut expectations. The consensus within the Governing Council appears directed at waiting for early-2024 wage data for further confirmation before taking steps to ease policy. Having said that, investors have upwardly revised their ECB rate cut expectations, increasing the probability of a June cut to 79%, up from 73% beginning of the week. Overall, money markets expect 91bps cumulative rate cuts by year-end.

German inflation slows further. Preliminary CPI reports from Europe’s largest economies indicated Germany’s inflation rate declined to 2.5% in February, more than market expectations of 2.6% and reaching the lowest level since mid-2021. Similarly, the French inflation rate also eased to 2.9% in February, marking the lowest level since January 2022, and Spain’s rate dropped to a six-month low of 2.8%, with both readings slightly above market expectations of 2.7%. Despite some recent positive inflation surprises recently, the ECB remains vigilant urging markets not to get ahead of themselves by prematurely declaring victory against inflation.

Eurozone inflation beats estimate. As with the growth story, so too is inflation diverging between Germany and the larger Eurozone. While consumer prices rose less than expected in Europe’s largest economy, the broader bloc saw its inflation moderate only slightly from 2.8% to 2.6%. It was the lowest rate in three months but came in above the expected 2.5% print.

Zooming in on China once again. The Chinese equity benchmark CSI 300 has turned positive on the year, after having fallen by 10% in the first 30 trading days of 2024. The likely bottoming of sentiment comes against the backdrop of the Chinese central bank having cut its 5-year loan prime rate (LPR) and the reserve rate requirement (RRR) in an attempt to dampen selling pressures. The People’s Bank of China has induced the most liquidity on record into its financial markets over the last six months and focus is not shifting to the fiscal authorities.

Policy announcements expected. The upcoming National People’s Congress of the ruling Communist Party on Tuesday will be watched for any news on economic policy announcements. The last three annual gatherings had not delivered on promises for stimulus and had been followed by falling equity prices. This could change this time around.

Global Macro

ECB, BoC meet but don’t macro to move markets

March to close out solid Q1? The first two months of the year have generated strong returns on equity markets across the globe with the US and European benchmarks at all-time highs and the Japanese Nikkei at its highest level since the 1990s. The continuation of this trend will depend on falling inflation rates and moderate growth prospects for the world economy and the US consumer.

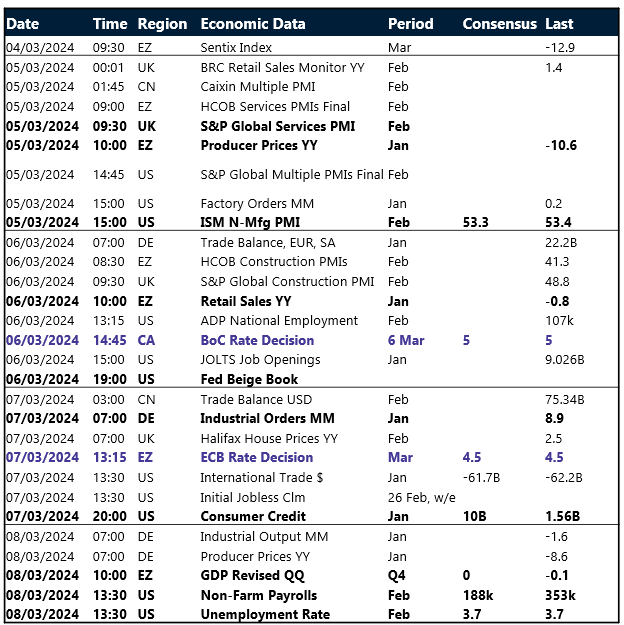

US data in focus. Against this backdrop, we will be watching out for three key data points on the macro side next week. The ISM non-manufacturing PMI on Tuesday, US job openings on Wednesday and the non-farm payrolls report on Friday. Next week will be US centric as Fed pricing has dominated regional stories and expectations for other central banks like the BoE, ECB and BoE.

No change expected. The policy meetings in the Eurozone and Canada will conclude without any change to interest rates. However, the rhetoric about future policy will be closely watched as both banks are expected to ease policy significantly starting in the second quarter of this year. We are expected the ECB to pave the way for rate cuts via lowering its inflation projections for this and next year and see a continued divergence of opinions within the Governing Council. Markets are betting on 3-4 rate cuts this year with the first one commencing in June.

FX Views

Dollar strength moderates

USD Resilient despite falling US yields. After suffering its worst weekly fall since late December last week, the US dollar index rebounded off its 200-day moving average and back above the 104 mark this week despite US yields falling across the curve. US data has been mixed this week, but all eyes were on the PCE inflation report, which came in-line with expectations and keeping hopes alive that the Fed will start cutting interest rates in June and deliver three cuts in total by year-end. There remains a sense of stability across markets at present though, particularly now that market expectations are more closely aligned with the Fed’s latest projections and comments. Given the wide divergence in economic performance between a still-booming US and recessionary Europe and Japan, it’s hard to bet on the dollar weakening substantially in the short-term, and upside economic data surprises could keep dollar selling at bay. But the dollar is historically overvalued, and we may have already seen its 2024 peak. The dollar index is more than one standard deviation above its 20-year average and so over the medium-term, we think the dollar should weaken against its major peers, especially once the Fed starts cutting rates.

EUR Holds Above $1.08 as inflation remains sticky. February’s inflation data in Eurozone sent markets a wake-up call that inflation pressures persist, with the small decline in the headline rate from 2.8% to 2.6% mainly due to base effect. The ECB is expected to hold its policy rates unchanged during the rate decision next week (Mar 7) as it needs more evidence of cooling wage growth pressures and sustainable converge of inflation towards its 2% target. Traders are presently anticipating around 90bps of rate cuts from the ECB this year, down from approximately 150bps at the beginning of the year. EUR/USD could face another month of struggle as US developments continue to overshadow domestic events. On weekly basis, the pair remains largely unchanged, but has entered a bearish trend since mid-week. If EUR/USD manages to stabilize above $1.0820 and starts using that level as support, $1.0870 (50-day SMA) could be seen as next resistance before the psychological level of $1.0900. On the downside, a breach below $1.0800 could attract euro sellers and open the door for an extended slide towards $1.0790 (21-day SMA) and $1.0760.

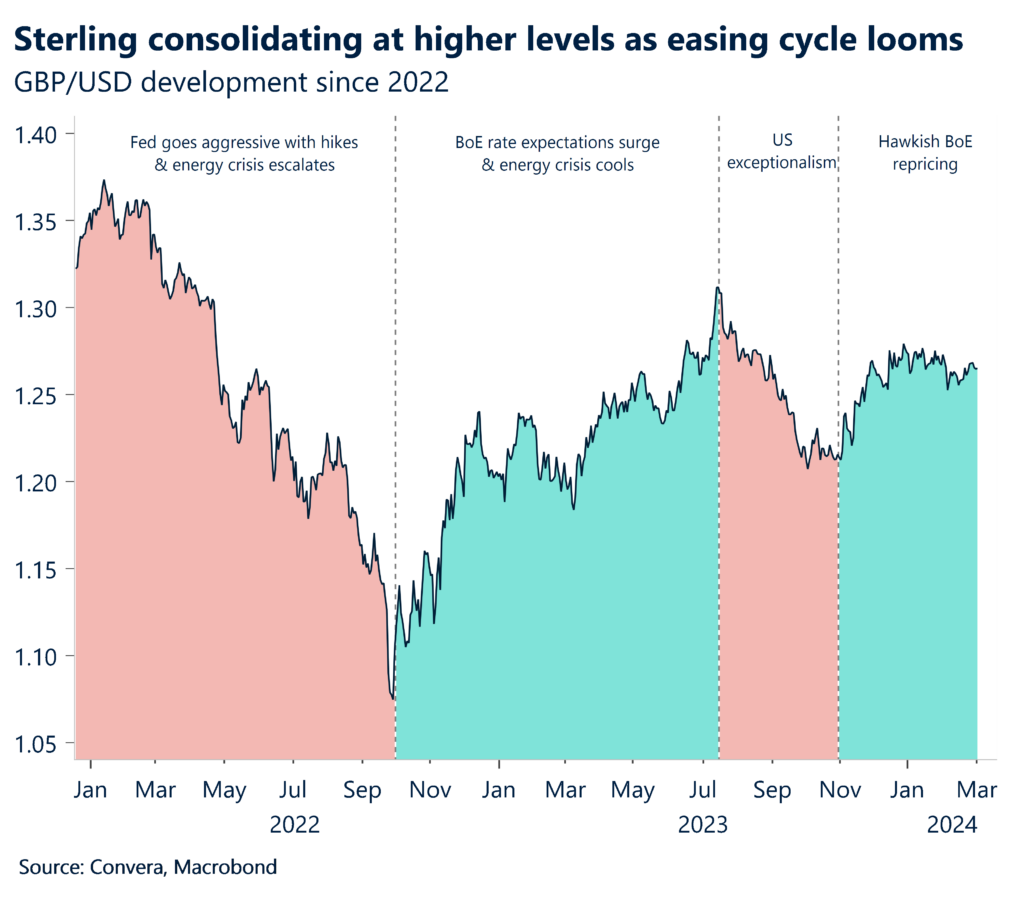

GBP Consolidating phase in motion. The British pound ended its longest daily winning streak against the US dollar since October last year as investors trimmed their bullish bets on the pound for the first time in eight weeks. GBP/USD struggled once again to hold above the $1.27 threshold and remains caught in an unusually tight 2% trading range between its 200- and 50-day moving averages. The 3-month implied volatility of GBP/USD also hit a 4-year low, reflecting the degree of investor complacency and the currency’s steady performance. These quieter conditions across the FX space make so-called carry trades more popular, which has supported the high-yielding pound this year, helped by the hawkish repricing of UK interest rate expectations under the assumption that the BoE will ease policy less than the Fed and ECB. Money markets are pricing less than three rates cuts by the BoE before the end of this year, half the amount expected at the start of the year. However, because of this, there is arguably little room for further hawkish repricing, and with bullish GBP bets well above their long-term median, sterling’s momentum has stalled. Indeed, February saw the pound appreciate against just 20% of its global peers compared to the 70% in January. Next week brings the UK budget, and the pound could strengthen on growth initiatives and tax cuts but remains vulnerable to fears of government over-spending.

CHF Swissy throws hissy at Jordan’s departure. The Swiss franc fell to 13-week low against the euro after a surprise announcement that the Swiss National Bank (SNB) Chairman, Thomas Jordan, will step down in September after more than 12 years at the helm. During his tenure, Jordan steered Switzerland through Europe’s debt crisis, removed the cap on the franc in January 2015, and drove the response to the Credit Suisse crisis last year. The SNB also raised rates before the ECB did in 2022 and sold FX reserves to help fight inflation, which saw the franc rise to 2015 highs against the euro. The franc gained nearly 10% against the US dollar last year, the biggest advance among the G10, but the tide has turned, and the franc has shed over 4% year-to-date. The SNB is expected to cut interest rates before its G10 peers, which is weighing heavily on the franc. On Monday Swiss inflation data for February will be crucial as markets are currently pricing a 70% probability of a rate cut at the end of this month.

CNY China policy tailwind ahead of NPC. Policy tailwind should continue supporting markets in the lead up to the National People’s Congress starting March 5. The economic focus is expected to be on expanding domestic demand, as indicated by top leadership. President Xi Jinping called for large-scale renewal of equipment, consumer goods and lower logistics costs. Premier Li Qiang emphasized stabilizing foreign investment this year. CNY faces downward pressure from the PBoC’s incremental dovish policy turn. Yield differentials have already widened in favor of the US dollar versus the yuan over the past month and could extend further as PBoC policy grows more dovish. Core economic data to watch next week includes the Caixin Services PMI, trade balance and FX reserves, which will give clues about China’s economic trajectory.

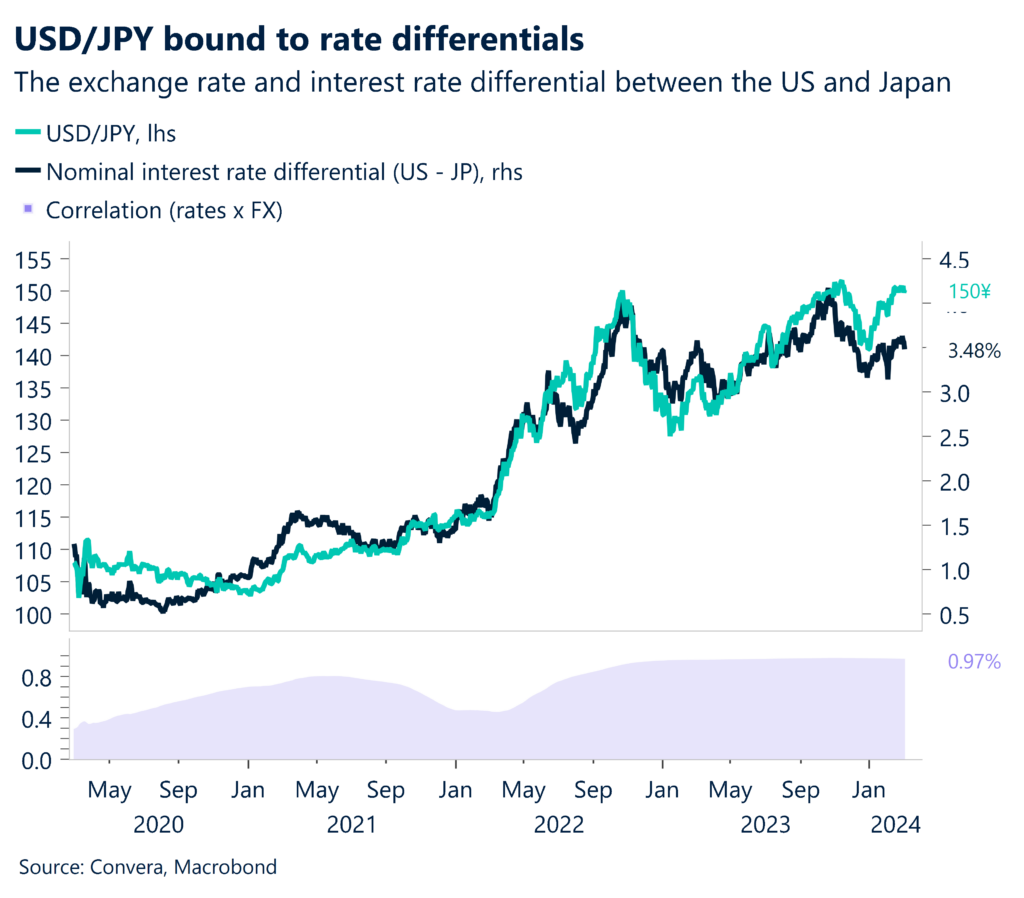

JPY Kanda warns against excessive yen moves. The Japanese yen fell to its lowest level since 2015 against the pound and came close to its weakest since 2008 versus the euro this week before an upside surprise in Japanese inflation cooled the yen’s depreciation. Moreover, Japan’s top finance ministry official Masato Kanda said excessive exchange rate moves are undesirable and action could be taken to respond, which further boosted the yen and USD/JPY dipped to 149.19 – a fresh 2-week low, before rebounding back above 150 by the end of the week. The yen remains 2024’s worst G10 performer so far (YTD performance of USD/JPY +6.91%), near post-1990 lows. Key Japan economic data to watch next week includes CPIs, services PMI and the adjusted current account balance. These will give further indications about the health of the economy and potential for additional BoJ policy action.

CAD Slides to 11-week low. The recent stream of better-than-expected Canadian economic data was not enough to pull the Canadian dollar back from an almost 3-month low as the outlook for US rates continues to dictate USD/CAD direction. Canada’s GDP returned to growth in Q4 2023, expanding by 0.2% q/q helped by higher exports, and preliminary estimates indicate a 0.4% expansion in January. In addition, manufacturing sales rebounded in January and small business confidence further improved in February. The data underscored some resilience in the Canadian economy, giving the Bank of Canada more time to weigh on the appropriate timing and extent of rate cuts in the year. Despite that, USD/CAD closed the month of February 1.0% higher and is poised to rise for the third consecutive week. The Canadian dollar did not get any help from rising oil prices either. A retest of February’s peaks was driven by rumours that OPEC may extend production cuts into Q2. However, prices are unlikely to rally given that crude supply is expected to exceed demand for 2024. The key event next week is the BoC rate decision and there is a risk it turns a touch more dovish given the lower-than-expected inflation figures. This would have a negative effect on the Canadian dollar, and we could see USD/CAD breach past $1.3600 mark (Dec high).

AUD Steady Aussie inflation backs case for RBA cuts. AUD is currently trading near to YTD lows of 0.6442, with YTD performance of AUD/USD -4.7%. Australian inflation held steady at 3.4% y/y in January, the lowest since November 2021 and below forecasts of 3.6%, supporting the case for RBA interest rate cuts. Large increases in insurance and tobacco were partially offset by falls in recreation, ABS data showed. Monthly CPI can be more volatile than quarterly data. The RBA wants inflation returning to its 2-3% target range by 2025. While goods inflation has declined, services remain high and are expected to fall only gradually, the RBA said. Wednesday’s CPI data is more geared toward goods inflation. AUD/USD whipsawed around 0.6489-0.6567 this week, trading in its multi-quarter range. Building approvals, current account and GDP data are due next week, which will provide further clues on the economic outlook and RBA policy path.