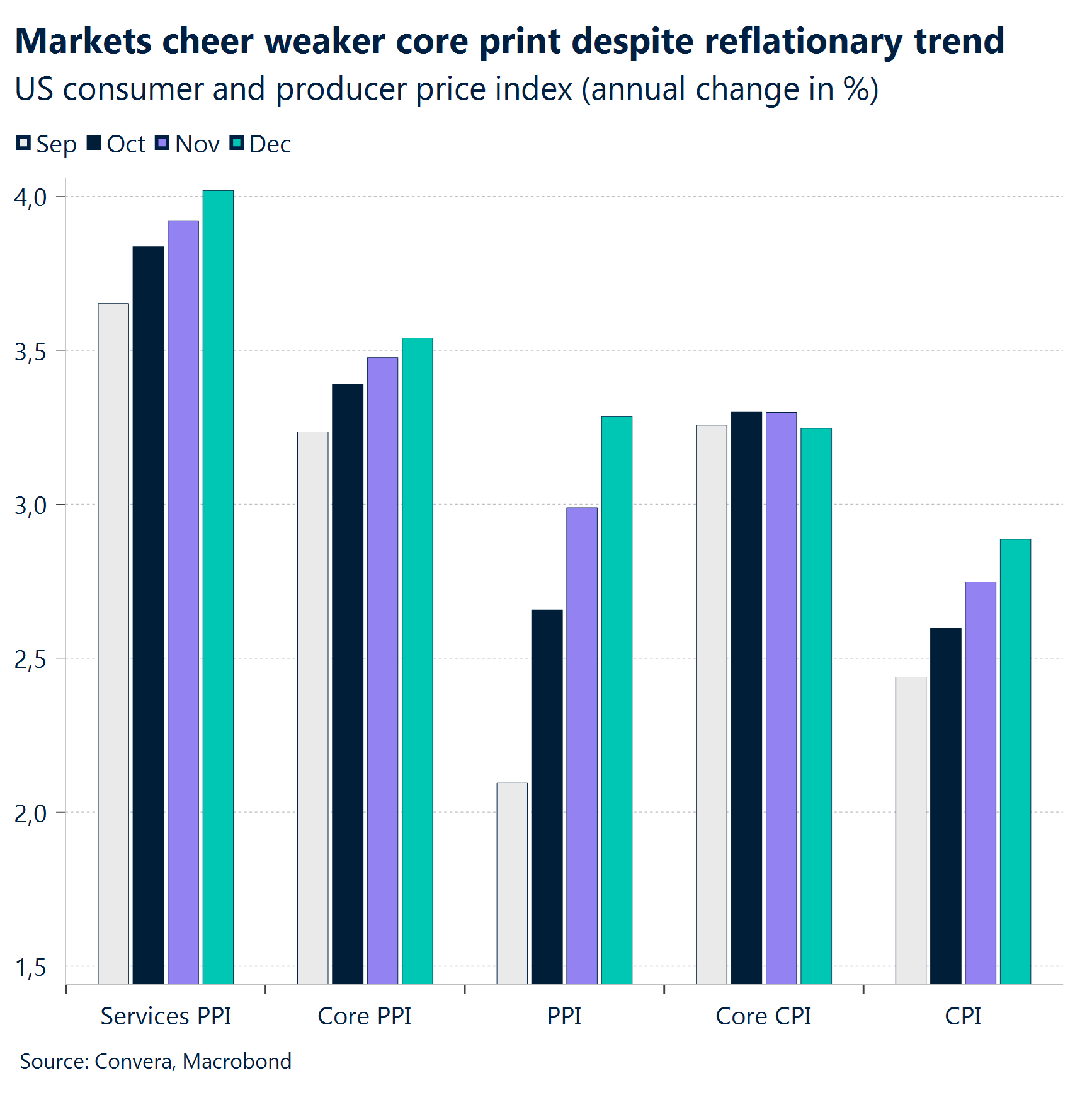

- Markets were choppy due to mixed macro data and dovish Fed comments. Weaker-than-expected US inflation data (core PPI and CPI) eased reflation concerns. Now the focus shifts quickly to the PCE report coming out next week.

- Retail sales grew strong but missed forecasts. The control group that is used to calculate GDP beat estimates, though. The Philly Fed Index hit its highest since April 2021, while jobless claims rose. An ambiguous macro week.

- Fed Governor Waller’s dovish comments decided the week for the dollar and yields and pushed them both lower, as the policy maker made the push for a potential rate cut in the first half of 2025 due to falling PCE inflation.

- ECB minutes showed unanimous support for a 25-bps cut in December. A cautious approach is expected, with rates stabilizing around 2% as inflation cools. Eurozone industrial production grew 0.2% in November, but growth remains weak.

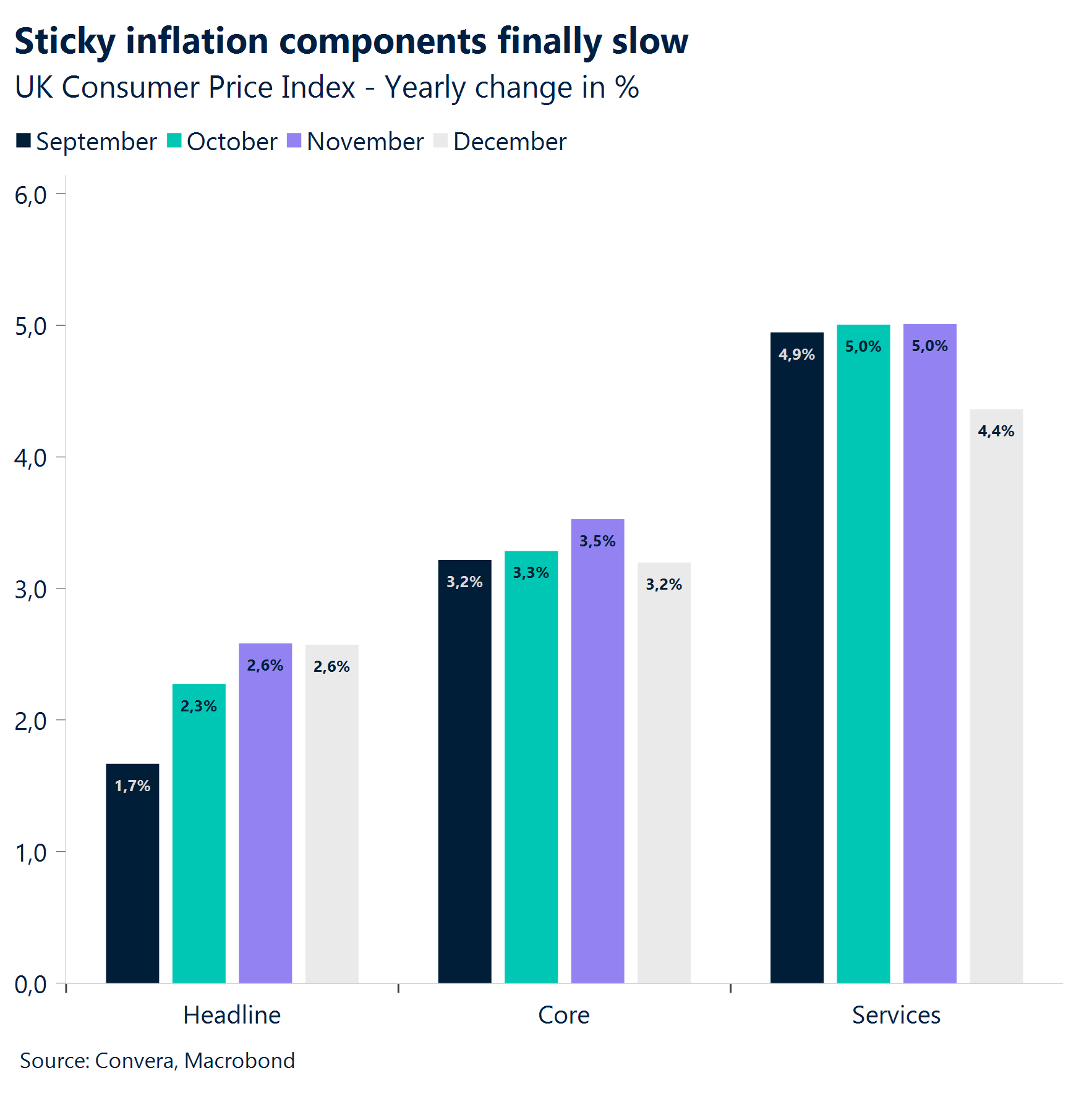

- UK inflation slowed to 2.5%, with core (3.2%) and services (4.4%) also cooling, increasing BoE easing expectations.

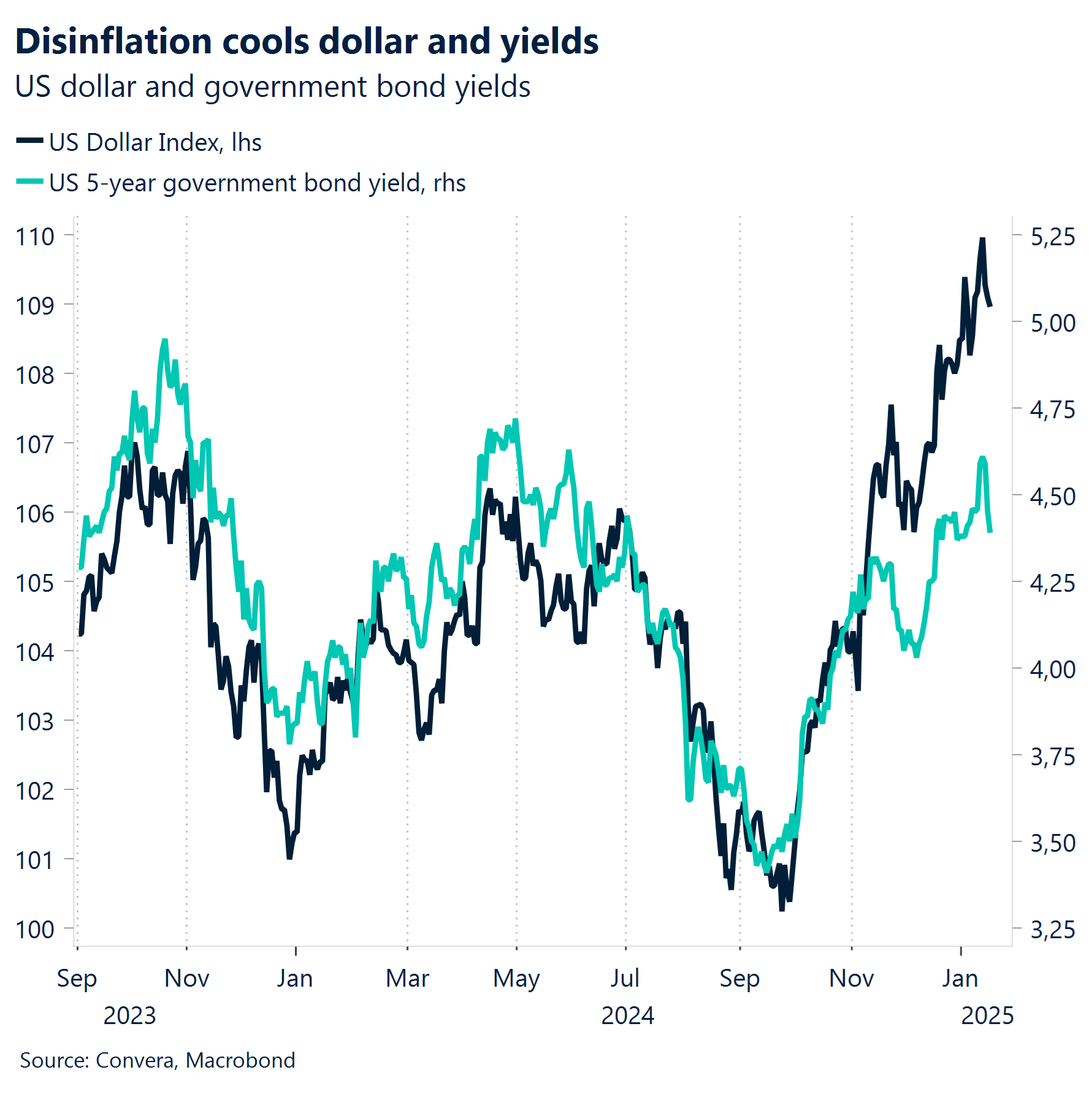

- The US dollar index (DXY) ended a 6-week winning streak after hitting resistance at 110.0, weighed down by softer inflation data.

- Since October 2024, GBP/USD has fallen nearly 10%, hitting a 25-month low near $1.21, with $1.20 seen as a key downside target.

Global Macro

Strong US economy, dovish Fed speak

A volatile week. Markets had some volatile sessions this week as investors weighed mixed macro data and dovish Fed commentary. While better-than-expected US inflation (core PPI and CPI) prints earlier in the week had eased concerns, fresh economic data and Fed speak brought uncertainty back to the forefront. Retail sales grew but missed expectations (-), while the control group beat estimates (+). Philly Fed Index surged to its highest since April 2021 (+). Jobless claims rose to 217K, reflecting holiday layoffs (-).

Dovish Waller. Despite the mixed signals, a stabilizing labor market and a revitalized manufacturing sector suggest resilience. Fed Governor Waller’s dovish remarks turned market sentiment around, pushing the dollar and yields lower again. His support for potential rate cuts in early 2025 was driven by declining PCE inflation, but we remain skeptical that inflation will fall to 2% this year. Instead, reflationary pressures appear to be resurfacing.

ECB to ease in January. The ECB minutes confirmed unanimous support for a 25-basis-point rate cut in December, the third in a row. Policymakers stressed a cautious, flexible approach to avoid economic stagnation or runaway inflation. Chief Economist Philip Lane warned against premature easing, while Mario Centeno suggested rates could stabilize around 2% as inflation cools.

Growth not improving. The macro outlook remains bleak. Eurozone industrial production rose 0.2% in November but is too weak to signal a recovery. Germany remains a key drag, posting its second consecutive annual contraction in 2024—the first since 2003—with a similarly grim outlook for 2025.

Global Macro

UK inflation eases, GILTs gain

UK inflation slows. Headline consumer prices in the UK rose 2.5% in December from a year earlier, missing the consensus forecast and previous print of 2.6%. Moreover, both core (3.2%) and services inflation (4.4%) slowed more than anticipated, which will be welcomed by Bank of England policymakers and market participants hoping for some respite from the turmoil in the UK gilts market that pushed benchmark government bond yields to a 17-year high.

NFIB optimism. Investors shrugged off the strong NFIB report, which showed small business optimism at its highest since 2018. Pro-growth policies like deregulation and tax reforms could boost smaller firms, with half of business owners expecting better economic conditions—the most since 1983. However, this optimism may be politically driven, as small business owners tend to favor Trump, a trend seen after both his elections. The second half of the year will be key in determining whether these expectations materialize.

Why are yields rising? There is a lively debate going on about the drivers of the recent increase in longer-dated US Treasury yields. Stronger-than-expected economic data and a stalling disinflationary trend have undoubtedly led investors to curtail expectations of Fed interest rate cuts, pushing yields higher across the curve. However, mounting fiscal pressures are also contributing to this trend. Investors are now demanding a higher premium for holding longer-dated bonds compared to shorter-term tenors, reflecting concerns about increased debt issuance and the precarious budgetary situation in the United States. The term premium for the 10-year Treasury bond has surged to 60 basis points, its highest level since 2015, signifying a growing preference for shorter-dated securities.

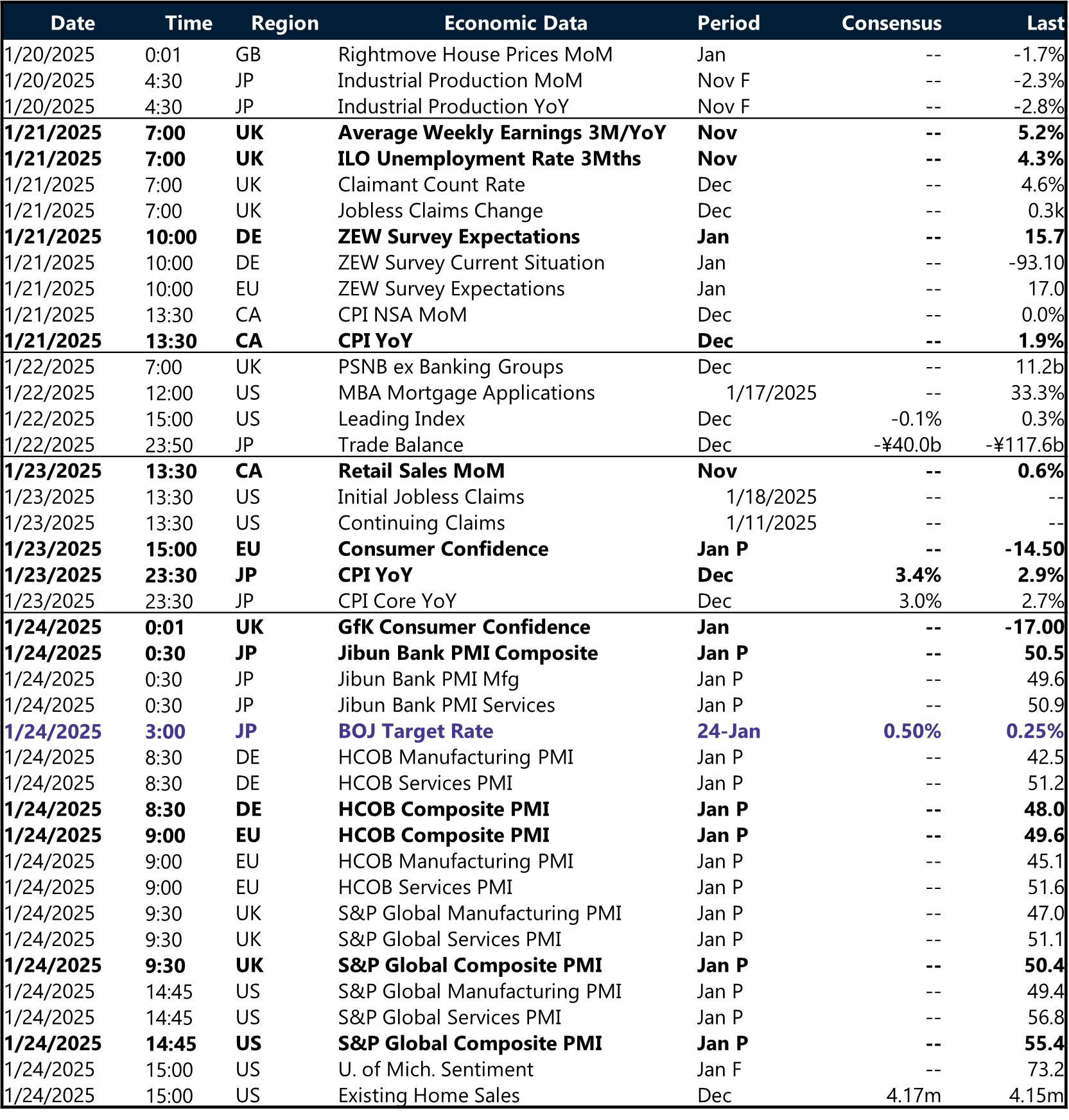

Week ahead

Crucial week as investors eye PCE data

The global economy faces another crucial week, with key data releases and central bank signals shaping market sentiment across the US, Eurozone, UK, and China.

In the US, all eyes will be on fourth-quarter GDP growth and PCE inflation, the Fed’s preferred gauge. With markets pricing in one to two rate cuts later in 2025, any upside surprise in inflation or consumer spending could challenge this outlook. Jobless claims will provide further insight into labor market resilience, while corporate earnings from major firms may drive risk sentiment. A stronger-than-expected inflation print could delay Fed easing expectations, pushing Treasury yields higher and supporting the dollar, while a softer report would fuel further equity gains.

The Eurozone continues to struggle with stagnation concerns. Weak industrial production and sluggish demand remain key headwinds, with PMI data next week week set to reveal whether manufacturing and services activity can rebound. The German ZEW investor survey will be closely watched to assess whether the region’s largest economy is stabilizing or heading for another contraction.

The Bank of England will try to get some hints on the trajectory of the economy after the softer CPI print this week. The labor report, and PMI data will test whether consumer spending is holding up despite high borrowing costs. If growth disappoints, expectations for earlier rate cuts could build, weakening the pound further.

Next week’s data will be pivotal in shaping expectations for global central bank policy, with markets reacting strongly to any surprises. Inflation prints, growth figures, and sentiment indicators will determine whether the recent narrative of rate cuts and economic soft landings holds or faces renewed challenges.

FX Views

Bracing for more intense swings

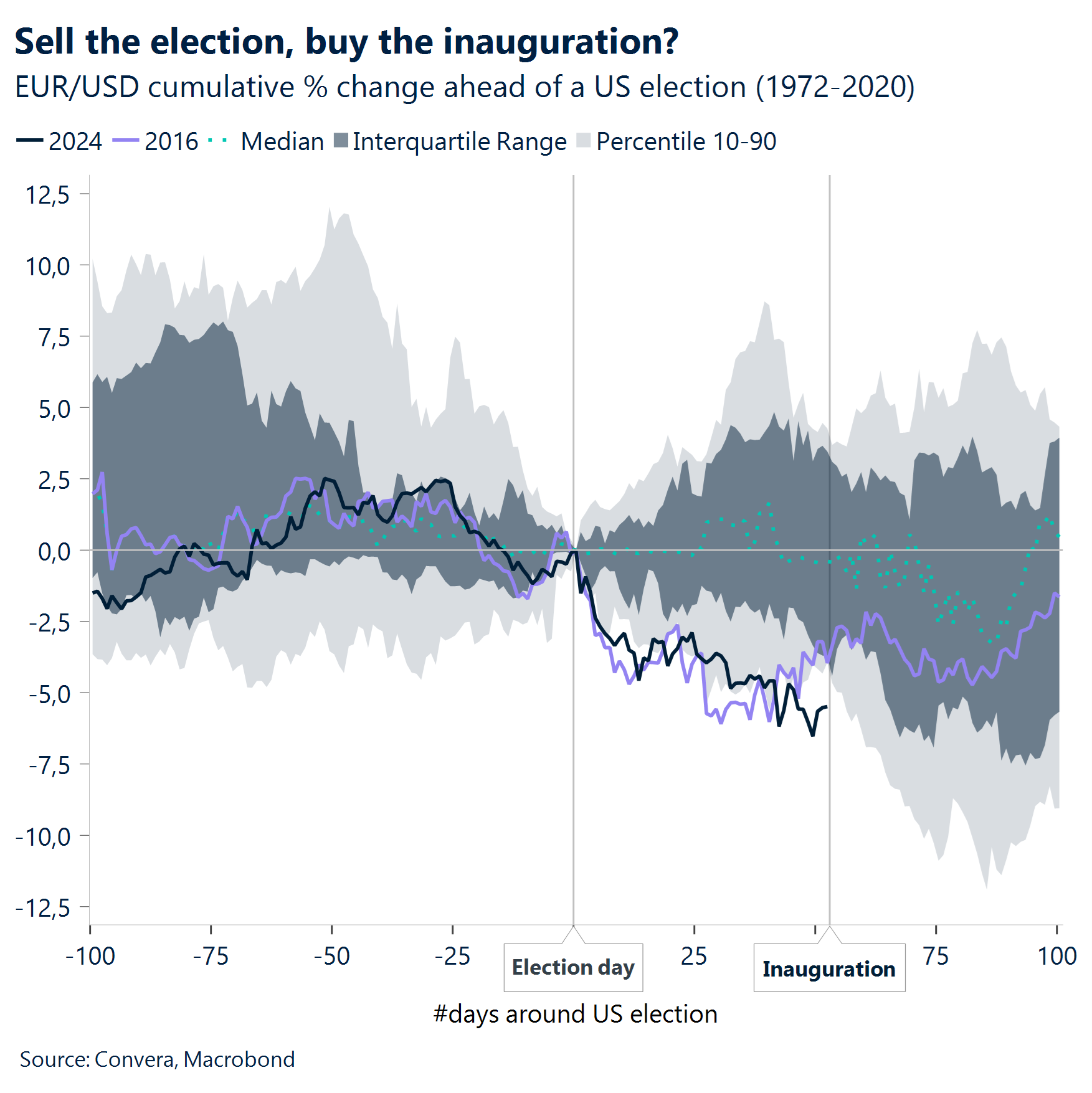

USD Bumping into resistance. The US dollar index (DXY) has snapped a 6-week winning streak, bumping into resistance at the 110.0 mark – near its highest since November 2022. Recent headlines suggest that the Trump administration may adopt a more measured and gradual approach to implementing tariffs, which has weighed on the buck. Moreover, despite the bulk of macro data coming in stronger-than-expected, the softer core inflation prints have weighed on yields across the curve and thus the dollar – highlighting their asymmetric reaction functions. The upward trend that started in October of last year remains intact though, as long as DXY remains above 108.60. US data misses and a dovish repricing of Fed rate expectations are necessary to prompt a sharper unwind of bullish dollar positions. But all eyes are on President-elect Donald Trump’s inauguration (Jan 20) to see whether executive orders on trade are implemented early on and trigger a fresh wave of dollar strength. Indeed, one-week implied volatility for the dollar spiked to the highest since the November election as traders position for more intense currency swings to come.

EUR Hesitant to recover. Despite hitting fresh 2-year lows against the dollar, the euro is on track to score its firstly weekly rise in three, supported by a broadly weaker USD on tariff news and mixed US data. That said, it’s only EUR/USD’s third weekly rise since late September, down over 9% over this period with the common currency still influenced (negatively) by external developments and Europe’s weak economic growth outlook. EUR/USD has recently been undershooting levels normally suggested by short-term rate differentials though, which suggests the pair should be trading closer to $1.05. However, bearish EUR positions continue to swell with calls of parity still hanging over the pair and there lacks compelling evidence at this stage that we have hit the bottom of this downtrend given the weak economic and political backdrop weighing on the euro. Improved cyclical headlines from China would support European exports and the euro, but we think a convincing reversal is dependent on the bullish-USD narrative shifting on the back of softer US data and softer tariff headlines.

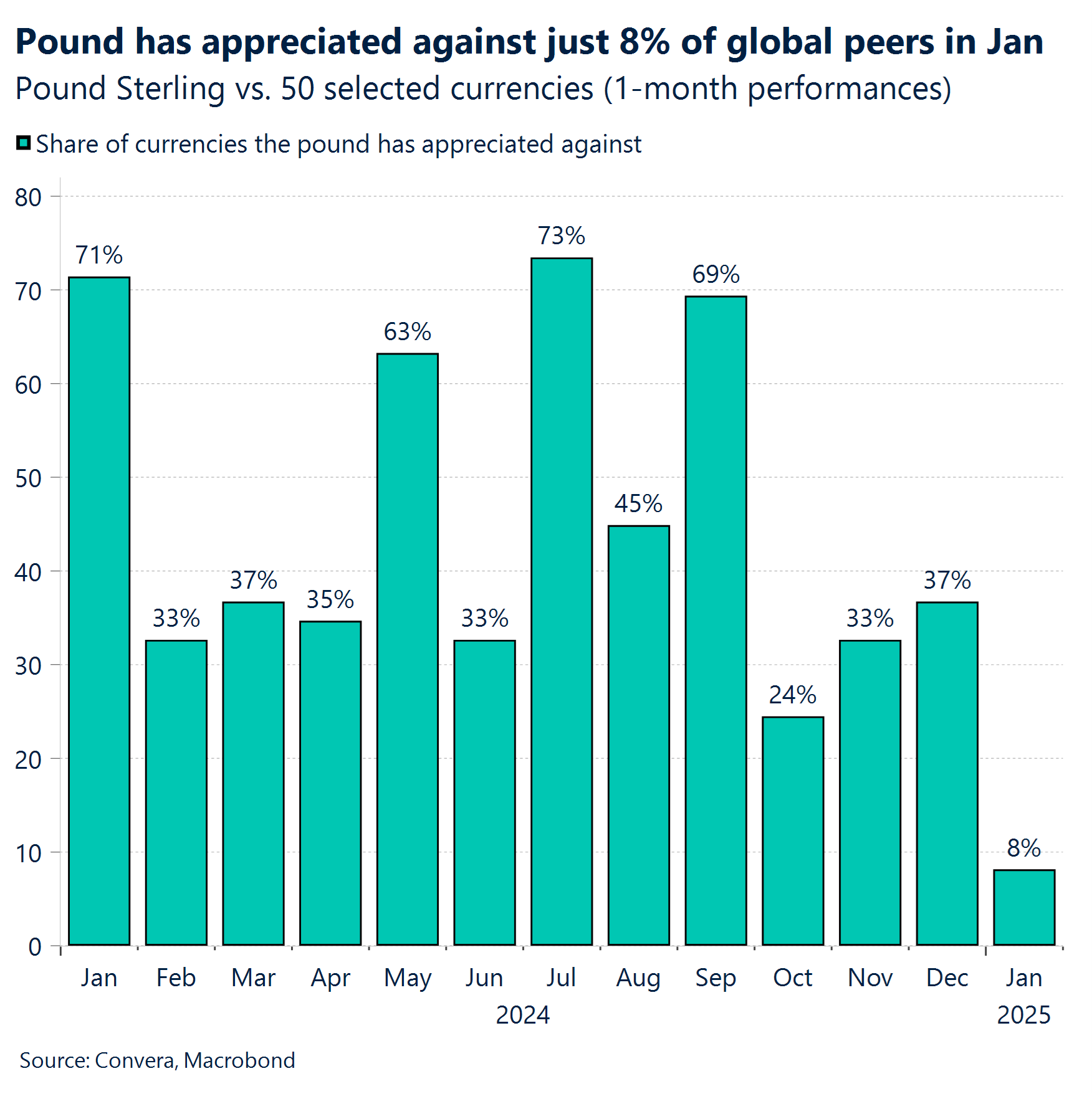

GBP Risks skewed unevenly lower. Since the start of October 2024, GBP/USD has only clocked 30 positive days and shed almost 10% in value. The pair fell to a fresh 25-month low this week, just shy of $1.21 and the situation could get worse before it gets better for sterling, with traders eying the psychological $1.20 handle as a key downside target. Although the daily and weekly relative strength indices are flashing oversold conditions, which could prompt a short-term rebound, a more meaningful recovery largely depends on a U-turn in the positive US dollar narrative and improved UK domestic data. Neither have materialised this week. Sterling continues to exhibit and an inverse correlation with rates, highlighted by the diverging paths of both GBP/USD and GBP/EUR relative to yield spreads, which reveals the negative structural challenges facing the UK economy. Options sentiment remains bearish GBP and volatility expectations elevated, though pricing has eased up this week from the multi-year extremes witnessed the week prior in the wake of the gilt market meltdown. Looking forward, positive GBP positioning adds to sterling’s headwinds, as speculators are still net long GBP. Moreover, the trade-weighted GBP index has weakened from recent highs but remains above the average level since the mid-2016 Brexit vote – and well above the Truss-era record lows back in 2022.

CHF Rangebound and expensive. The Swiss franc snapped a 5-week losing streak versus the USD this week as the USD/CHF exchange rate topped out at the 0.92 mark. A broadly weaker US dollar was the catalyst given the lack of top-tier data from Switzerland apart from consumer confidence beating expectations. EUR/CHF also slipped slightly lower, but remains trapped in a tight 1% range since the start of the year, unable to hold above 0.94 or hold below 0.935. Despite the franc’s weaker start to 2025, it remains one of the most expensive currencies in the G10 across valuation metrics. The SNB is expected to cut interest rates at least once more this year according to market pricing, but given the softer inflation outlook, a dovish recalibration could see the franc weaken further, especially if the SNB’s tolerance for a strong franc fades.

CNY Policy stability shapes near-term technical landscape. Recent policy communications from monetary authorities demonstrate a steadfast commitment to yuan stability, building on the balanced approach established throughout 2024. The strategic framework emphasizes readiness to implement counter-cyclical measures, including targeted adjustments to both RRR and interest rates, ensuring optimal liquidity conditions in the financial system. From a technical perspective, USDCNH presents an intriguing setup with immediate focus on the 7.3682 resistance level. This threshold serves as a critical pivot point for near-term directional bias. A convincing breach above this level could catalyze momentum toward 7.4616, potentially establishing a new bullish phase. Conversely, rejection at this resistance might trigger a corrective move toward 7.2242, particularly if the intermediate support at 7.3077 fails to hold. The upcoming LPR announcement will be crucial in determining near-term market dynamics, potentially influencing both technical and fundamental trajectories.

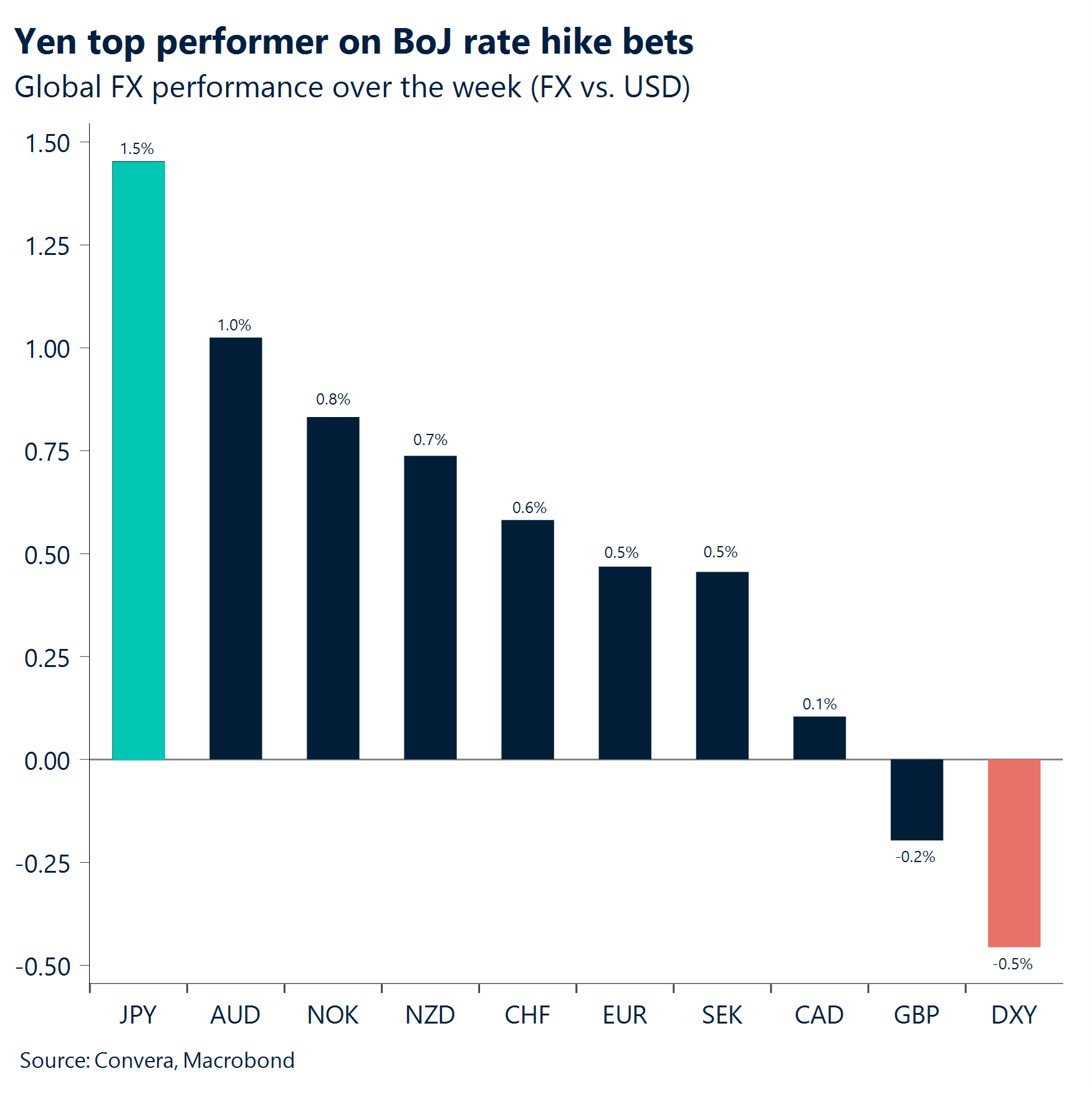

JPY Top of G10 pack. The monetary policy stance has taken a notably hawkish turn, with policymakers such as BoJ Ueda and Deputy Governor Himino signaling potential adjustments as economic indicators align with forecasts. January policy changes appear increasingly likely, though the approach remains characteristically measured. Currently the market has priced in ~21bps hike as of this writing. USD/JPY fell to 1 month low, at 155.7 level driven by hawkish comments. Intervention risks may rise if USD/JPY strengthens to 160 handle. The technical outlook has deteriorated significantly following the rejection at the rising wedge’s resistance trendline. The accelerating downward momentum post-January 13th, coupled with the failure to maintain upward trajectory, strongly suggests further weakness ahead. The bearish technical structure is particularly compelling given the steepening decline in momentum indicators. Key event risks include the BoJ meeting, trade data, and national inflation figures.

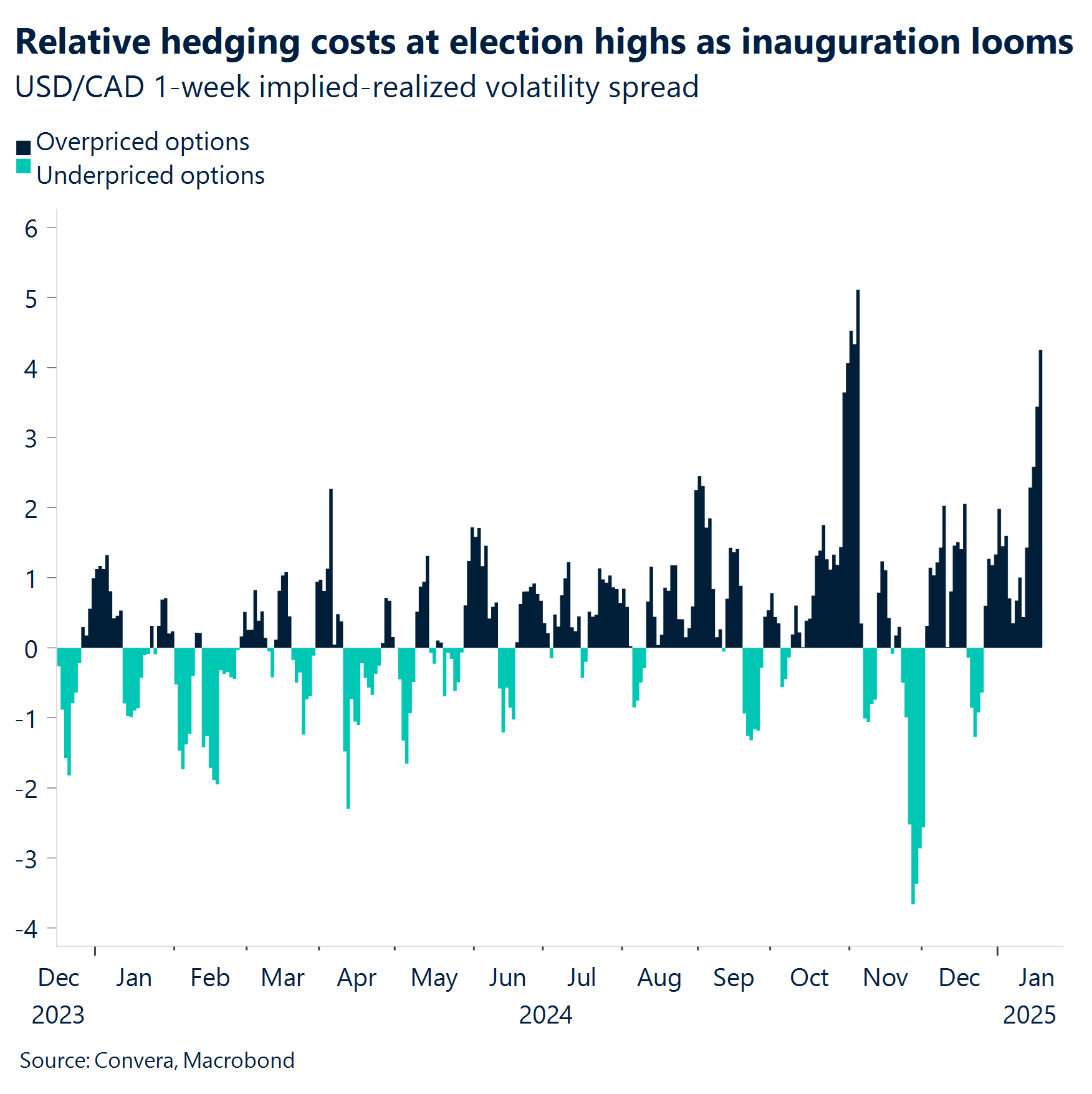

CAD Bracing for possible tariff action. The slight decrease in the US CPI has been a significant catalyst for North American equity and fixed income markets. However, this change did not impact the Canadian dollar, which continued trading within a narrow range of 1.4447 to 1.4302. The pair has paused near five-year highs as markets await potential US tariffs on Canadian exports. Investors and businesses will focus on Monday’s inauguration in the US. Should new US policies and trade tariffs be disclosed, a spike in volatility is anticipated. Rumors about tariffs range from those limited to critical imports to stricter tariffs on sensitive sectors like Energy, Manufacturing, and Automotive. Next week will reveal how the Canadian government handles the Trump 2.0 era, including potential retaliation reminiscent of the 2017-2020 regional trade war. Technically, the uptrend in USDCAD persists, with the pair above key 20-, 50-, and 100-day moving averages. Looking forward, USD buyers are targeting the lower trading range at 1.4280, while CAD buyers aim for 1.4470. On the macro front, two major data releases next week could add to volatility: Canadian CPI on Tuesday (expected YoY CPI: 2.2%) and retail sales figures on Thursday.

AUD Robust labor market data supports bullish technical setup. The Australian employment landscape showed remarkable resilience in December 2024, with employment growth outpacing the year’s monthly average at 0.4%. While the unemployment rate edged slightly higher, this was primarily attributed to record-high participation rates and minor historical revisions. The strength in hours worked, expanding 0.5% versus the year’s 0.3% average, further reinforces the labor market’s underlying vigor. From a technical perspective, AUD/USD exhibits a compelling falling wedge pattern with a projected target of 0.6421. Current positioning suggests favorable entry around 0.62-handles, with downside protection at 0.6100. A decisive break above the 20-day SMA would significantly reinforce bullish momentum. However, vigilance is warranted near the lower support trendline, as any breach would invalidate the constructive outlook. Market focus shifts to upcoming NAB business confidence readings for additional directional cues.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.