Written by Convera’s Market Insights team

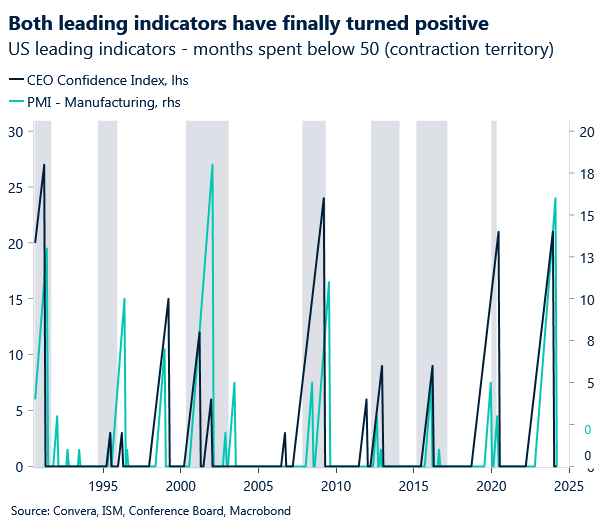

The US manufacturing recession is over

Boris Kovacevic – Global Macro Strategist

The week began with Europe and large parts of the world still enjoying their extended Easter holiday. However, the lack of economic data releases outside of the US did not mean that price action would be muted. The upside surprise on the ISM manufacturing PMI that we were looking for induced some volatility into currency markets and catapulted the US Dollar Index and US 10-year Treasury yield to four-and-a-half and three month highs.

The US manufacturing sector managed to grow in March with the Purchasing Manager Index rising from 47.8 to 50.3. The monthly increase follows 16 months of contraction and is a testimony to how the pro cyclical and rates sensitive parts of the economy are starting to recover. Most sub-indicators from employment to new orders improved last month. Most notably, price pressures and production levels increased to 55.8 and 54.6 and therefore remaining well in expansion territory. This upside surprise sets us up nicely for the upcoming data. The ISM services PMI, job openings and the non-farm payrolls report will be closely watched in addition to the plethora of Fed officials taking the stage this week.

After just one trading day, the US dollar has risen more this week than it has during the whole last one, highlighting how surprised markets were by the PMI beat. Equity markets started the week on the back foot as the probability of the Fed cutting interest rates in June briefly fell below the 50% mark. EUR/USD is on track to fall for a fourth consecutive week if the data continues to come in dollar positive. This holds true especially as the incoming European inflation data is expected to put pressure on the European Central Bank to cut rates sooner than the Fed. Market pricing continues to see three rate cuts as likely, in line with the Fed’s dot-plot published at the last meeting in March.

Where will volatility come from?

Boris Kovacevic – Global Macro Strategist

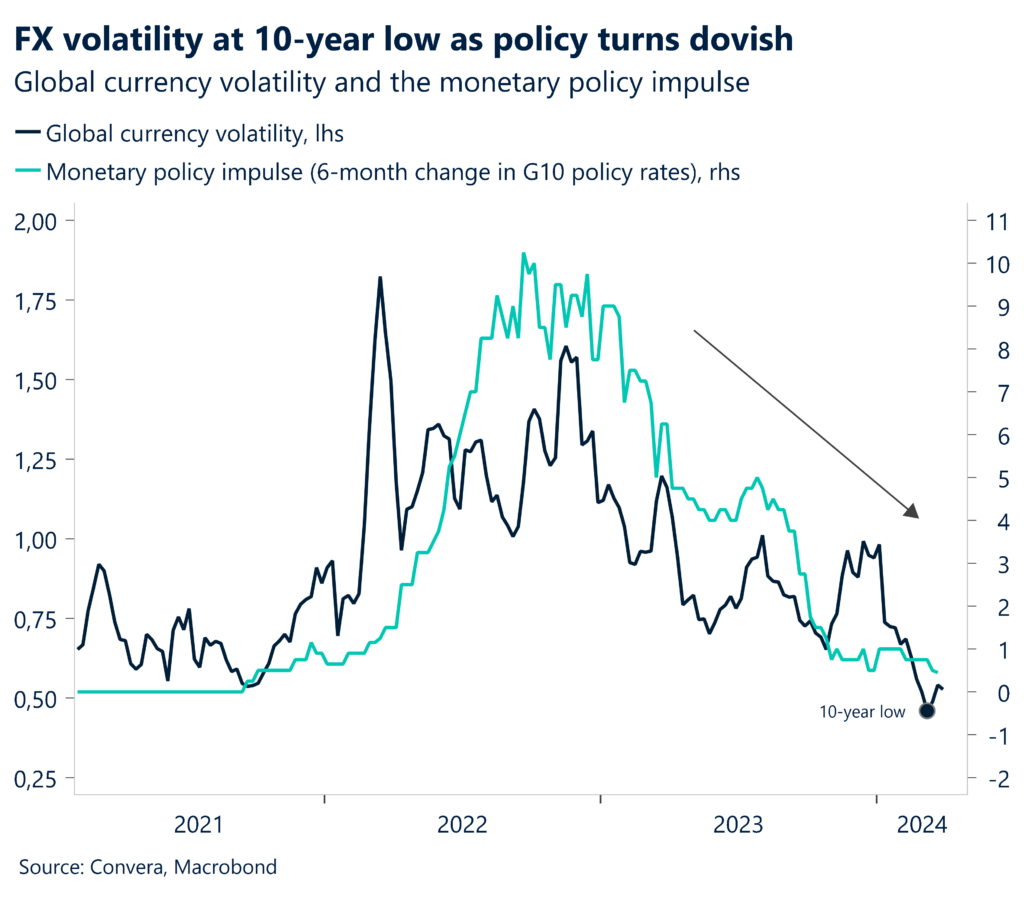

We have recently argued that the eventual policy divergence between G10 central banks is unlikely to cause a significant increase in volatility if inflation remains anchored. In low-inflation regimes, monetary policy has the ability to turn accommodative as soon as volatility rates spike, essentially functioning as an absorber of external shocks. This was not possible in 2022 and 2023 as high inflation prevented policy makers to react to increased volatility by cutting interest rates.

However, as price pressures dropped, policy turned dovish again, leading volatility rates lower. In this dovish policy regime, characterized by a bias to ease policy, only a renewed spike in inflation or an external shock (geopolitics, elections, market crash) would be able to meaningfully lift volatility rates from current levels. While important for FX trends, the divergence of policy rates seemingly won’t do the trick of bringing back volatility.

The upcoming elections in Europe and the US are major candidates for becoming volatility catalysts. In the short-term, any inflation and macro data suggesting that we are moving into a higher inflation for longer regime would increase volatility. Much stronger than expected data would postpone the already priced in rate cuts, effectively dampening risk sentiment and putting pressure on equity valuations. This explains why yesterday’s US PMI beat rattled markets as it reduced the probability of the Fed cutting rates in June.

Deeper drop due for sterling?

George Vessey – Lead FX Strategist

Amidst the stronger US data at the start of the week, the British pound has broken below some key moving averages against the US dollar in a bearish move which signals the potential for a deeper drop in GBP/USD in the short term. The currency pair has fallen almost 3% from its 7-month high recorded in early March and is close to testing its 2024 lows nearer $1.25. Hopes for $1.30 trading this spring are fast evaporating.

Traditionally, the pound performs the best against the US dollar in the month of April, but the opening day of the month saw GBP/USD slump around 0.7% and close below its 200-day moving average for the second time this year. Last time the pound closed below this key level it rebounded and trended gradually back into the top half of its year-to-range near $1.28. But this time, it’s also broken below its 50-week moving average – a support level that’s been in place since mid-November. These technical indicators on the charts don’t look promising for sterling, especially at a time when speculators are so bullish on GBP. From a fundamental standpoint, falling UK inflation has brought forward UK rate expectations, on par with the Fed and ECB in June. Traders are even placing a small, but nonetheless noticeable, bet the BoE could be the first of the three to cut in May.

The absence of any top tier economic data from the UK this week, bar final PMI numbers, means GBP/USD will be at the mercy of US data. Yesterday’s upbeat US ISM print sent US yields to 3-month highs and strengthened the dollar. Could a strong round of US jobs figures this week accelerate the decline in cable and bring into focus the 100-week moving average located near $1.23?

Dollar jumps around 1% across the board

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: April 1-5

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Join us for Convera Live! A series of in-person events discussing the future of global payments.