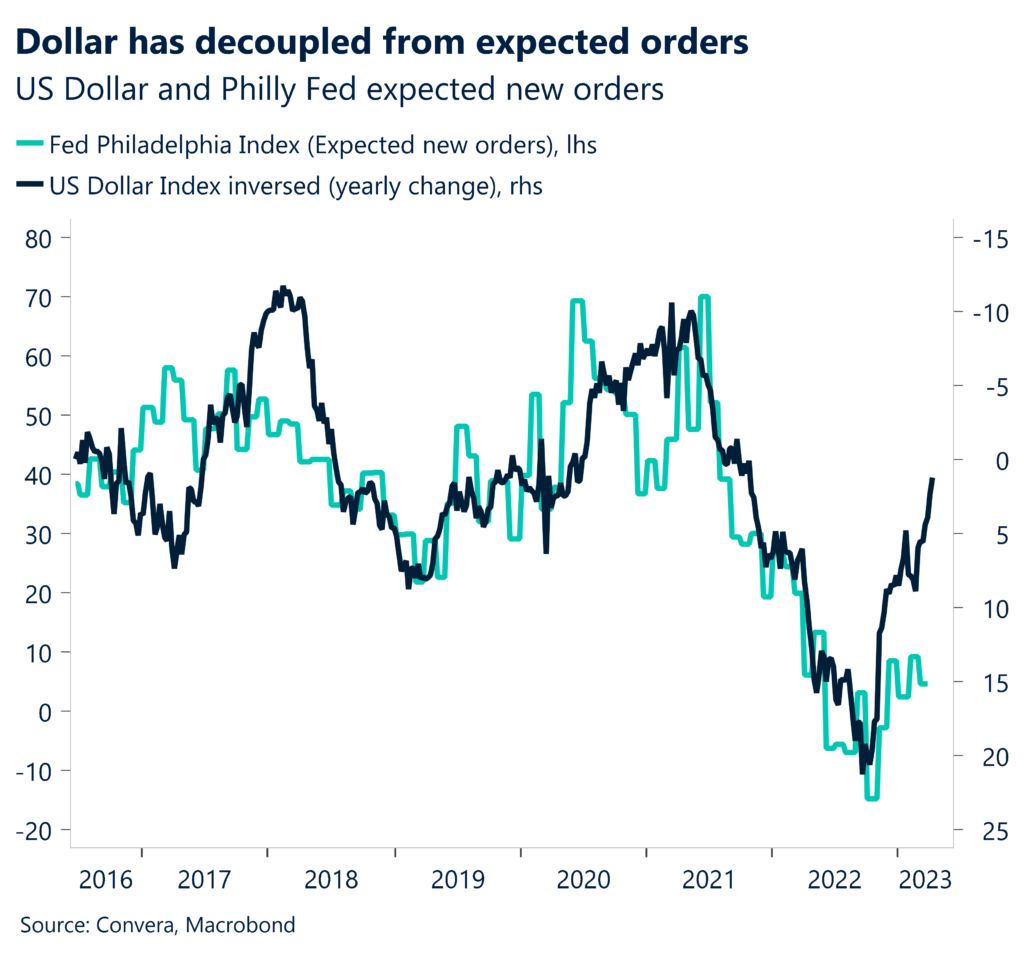

Dollar cushioned by falling rate-cut bets

The US dollar is making a mild comeback against many peers this week as the probability of interest rate cuts by the US Federal Reserve (Fed) has faded modestly. The Fed Beige Book of economic conditions was published last night and revealed the banking turmoil had little impact on economic activity or credit availability, which helps the central bank’s view that US rates will have to stay higher for longer to tackle sticky inflation.

Since the banking sector turmoil erupted, volatility in rates markets soared as traders bet on the Fed cutting interest rates aggressively from as early as July this year. Now, the Fed funds rate is seen just below 4.6% at the end of this year, the highest since the banking turmoil began and implying markets are pricing only two full cuts from the Fed’s peak in 2023, rather than three. The dollar has strengthened, lifted by rising Treasury yields, though the pound has stayed firm after UK inflation remained above 10% in March keeping the pressure on the Bank of England (BoE) to continue raising rates. We still think that the US dollar should continue to weaken against many currency peers over the medium to long term though if the Fed’s hike in May proves to be the last in its tightening cycle.

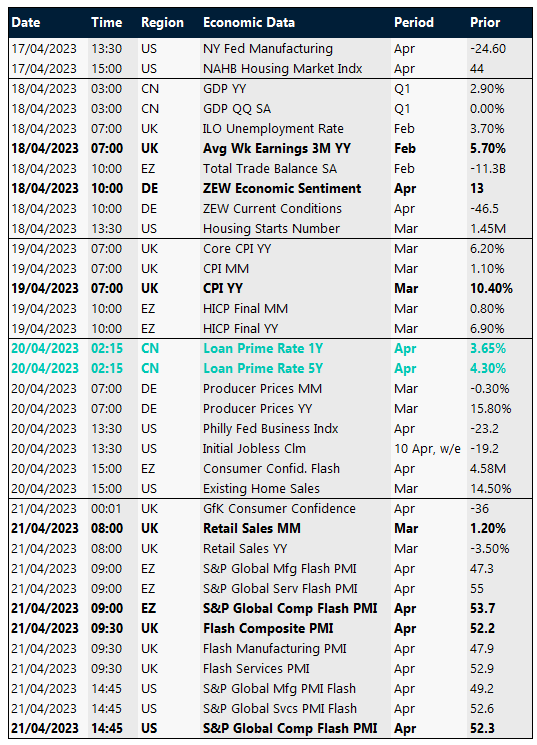

Today, we have the Philadelphia Fed index, which will be closely scrutinised, initial jobless claims and existing home sales data from the US. And with two weeks to go before the Fed meeting, central bank speakers have their last chances to steer market expectations before the quiet period starts.

UK interest rates to peak at 5%?

Sterling is stabilising above $1.24 versus the US dollar, helped by UK data this week showing unexpectedly high wage growth figures and above-consensus readings in both headline and core inflation. Financial markets have thus fully priced in a quarter-point Bank of England (BoE) rate rise for May and further hikes to bring the rate close to 5% by the end of the year.

The consensus view according to market pricing is for the Fed to end its hiking cycle after next month’s rate rise and the BoE to continue raising rates, therefore money market and government bond yields currently favour a further leg up in GBP/USD. The two-year yield differential between the US and UK is at its lowest since November 2021 (barring last year’s mini-budget turmoil), at which point GBP/USD was trading well above $1.30. With GBP/USD struggling to break north of $1.25, the pound appears cheap at current levels. That’s not to say we expect sterling to continue appreciating though. Whilst the economic outlook has improved in the UK, stubborn inflation in both goods and services (35% of the 270 items in the UK’s inflation basket are above 5%) met with more BoE rate hikes, will only exacerbate the cost-of-living crisis and increase recession risks in the UK. Moreover, should global recession fears grip markets once again, the risk-sensitive pound is likely to be punished given its strong positive correlation with global equities over the past month or so.

No significant data is due out of the UK today, but several BoE speakers are scheduled. On Friday, we see if UK consumption is struggling with retail sales, which have been in the negative for 11 months, published first thing, followed by flash PMIs.

Euro shrugs at plunge in producer prices

Markets expect another 75 basis points of rate hikes by the European Central Bank (ECB) this year, with the deposit rate rising to a peak in the autumn. Alike the pound, the euro is benefiting from such pricing as US/EZ rate differential narrow. EUR/USD continues to struggle to hold above the $1.10 mark but remains supported by a softer dollar environment overall.

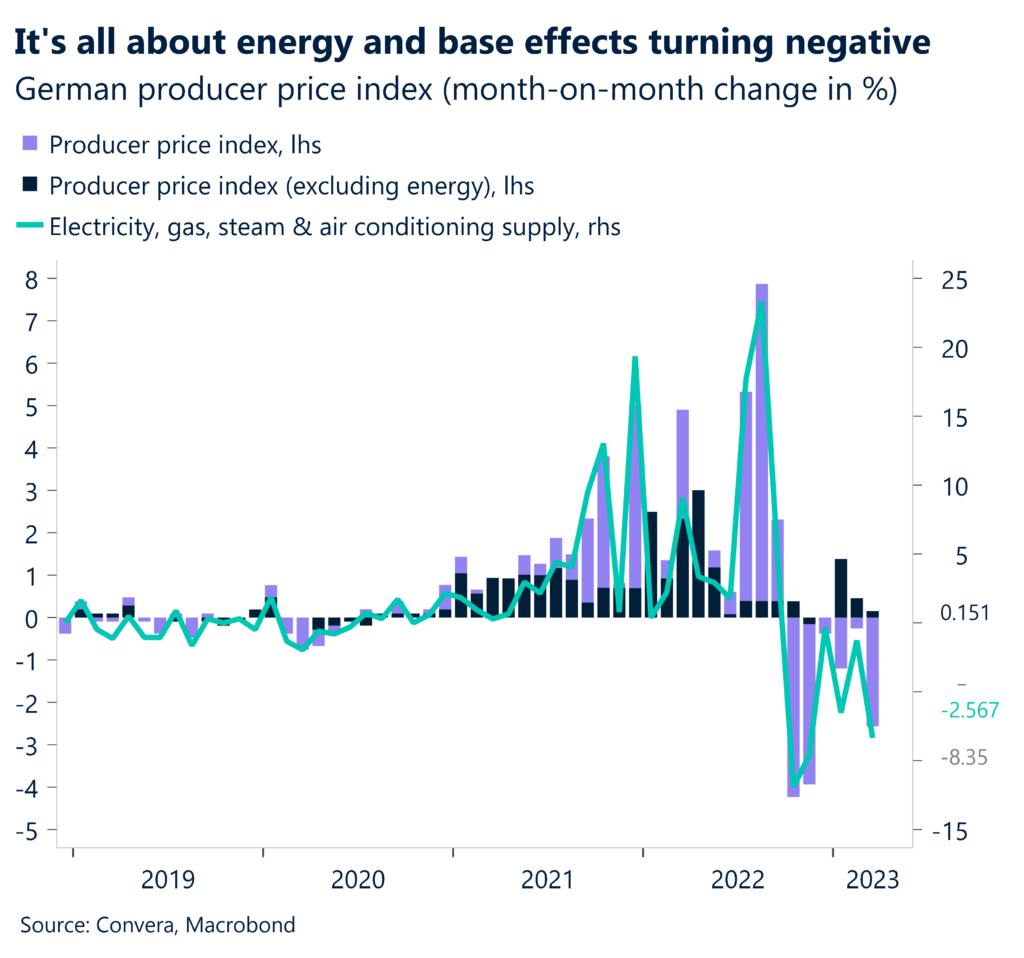

Across the FX markets there appears to be some stabilisation though. Volatility in the rates markets has subdued and this has helped to soothe currency markets as investors await the raft of key central bank meetings at the start of next month. Recent data from Europe has also been largely overlooked. German ZEW surveys were mixed, with expectations dropping sharply but the current situation index recovering much more than expected. This morning, German producer inflation slowed for a sixth straight month to a 22-month low 7.5% in March. This is over half the pace of the previous month and significantly lower than September’s peak of 45.8%. Falling producer prices should feed through to consumer soon enough, but the Eurozone still does not have inflation under control and its core rate was steady at 5.7% in March – above the US core rate of 5.6%.

The focus in Europe today is on the March ECB meeting minutes, which could shed more light on the decision process for May. ECB hawk Isabel Schnabel is also scheduled to speak, and flash consumer confidence data drops in this morning. We expect the euro to remain range-bound in the short-term though, between $1.09-$1.10 versus the USD and €1.13-€1.14 versus the pound.

FX volatility eases ahead of CB decisions

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: Apr 17-21

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.