Written by Convera’s Market Insights team

Check out our latest Converge Market Update Podcast where our Global Macro Strategist, Boris Kovacevic, breaks down this week’s most notable macroeconomic news.

Dollar rises the most in a month

Boris Kovacevic – Global Macro Strategist

Investors have welcomed the Federal Reserve’s (Fed) lack of pushback against the recent easing of financial conditions with open arms and feel reassured in their hopes that the peak of the global tightening cycle lies behind us. The European equity benchmark rose for a seventh consecutive week and has extended its gain since November to 18%. The S&P 500 pushed higher as well and has now risen in 18 out of the last 21 weeks with a 10% year-to-date gain under its belt. Bond yields across countries and the curve fell against the backdrop of this week’s dovish central banks deliveries. The US dollar did manage to rise despite its Fed-induced fall on Wednesday, mostly due to idiosyncratic weakness from the pound, yen, and euro, but with U

This week featured some second tier economic data from the US that painted a slightly better picture of the world’s largest economy than the recent news flow would have suggested. All five economic releases surprised the consensus to the upside with housing and manufacturing data continuing to distance itself from the recent bottom as labour market data remains robust. The NAHB Housing Sentiment Index improved across the board, something that was echoed by both housing starts and existing home sales being up 10.7% and 9.5% last month. Initial jobless claims remained low at 210 thousand, while the forward looking components of the Philadelphia Fed Manufacturing PMI surged. This barometer is the first leading index published for the month of March and is setting the scene for a positive close of the first quarter for the US manufacturing sector. The uptick in sentiment got confirmed by the ISM PMI showing the manufacturing sector expanding by the most this year.

The US dollar recorded its biggest daily rise since early February on weak data from Europe and a dovish delivery from the Bank of England (BoE). However, the Greenback’s sensitivity to strong macro data has been underwhelming, showing the clear bias of investors against the US dollar. The reaction function of the dollar to incoming data is asymmetric in the sense that weaker data seems to be moving the currency more than upside surprises. This does not mean that the dollar cannot rise from current levels, especially as US inflation is expected to remain higher than in the Eurozone and UK. However, the extent of positive data surprises needed for a substantially higher dollar has risen in recent weeks.

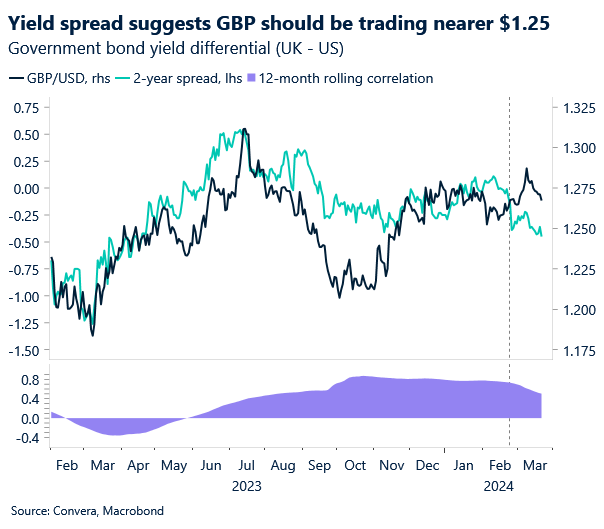

BoE’s dovish hold dents pound

George Vessey – Lead FX Strategist

As expected, the Bank of England (BoE) left its Bank Rate at 5.25% yesterday, but it was a dovish hold given the Monetary Policy Committee’s 8-1 vote split. The two previously hawkish dissenters voted with the majority to keep rates unchanged this time, while Swati Dhingra once again voted for a cut. GBP/USD suffered its worst day in over a month, while GBP/EUR slipped to its lowest level in three weeks. This morning’s UK retail sales data came in slightly stronger than expected, but stagnated in February, offering the pound little support.

We highlighted recently that risks to the pound lean asymmetrically to the downside in the short term given policy pricing and stretched positioning. The risk of a dovish tilt by the BoE also increased after the bigger-than-expected fall in the UK inflation rate this week, from 4% to 3.4% y/y. The flash PMI figures released before the meeting also pointed to slowing momentum in the UK’s dominant services sector, although it was the fifth month of expansion in the country’s private sector overall. The forward guidance from the BoE remained unchanged stating that rates need to stay sufficiently restrictive for an extended period of time, but BoE Governor Andrew Bailey said things are moving in the right direction. As a result, UK gilt yields and sterling tumbled as the probability of a June cut increased to 75% from 60% pre-BoE and markets even put a relatively small (15%) probability on a May rate cut.

The UK-US yield spread fell to a 1-year low, which saw GBP/USD extend its drop from a daily high of $1.28 to $1.2620. The currency pair continues to oscillate between its 200-week ($1.2858) and 50-week ($1.2575) moving averages for now, still lacking a decisive breakout higher or lower. The next key support lies at the 200-day moving average, currently located at $1.2591.

Euro pares post-FOMC gains

Ruta Prieskienyte – FX Strategist

Thursday was yet another busy day with plentiful monetary policy action. First up, in an unexpected move, the Swiss National Bank (SNB) cut its main policy rate from 1.75% to 1.50%, becoming the first G10 central bank to kick off the monetary policy easing cycle. The SNB’s tone and the huge downward revision to inflation forecasts suggest that a further cut in June is very likely. In response, EUR/CHF rallied 1.1% to a 7-month high of CHF0.9787, but further gains will depend on how quickly the ECB will follow suit. Meanwhile, Norway’s central bank kept its benchmark interest rate unchanged at a 16-year high of 4.50%, signalling intentions to cut only once by year end. The Norwegian crown initially strengthened to NOK11.51 against the euro based on seemingly hawkish remarks, before dropping to a 4-month low as the core inflation remains almost double the rate observed across the common bloc.

On the data front, the preliminary figures showed that the private sectors across the Eurozone continued to stabalise over the month of March. The preliminary composite PMI reading for the bloc rose to 49.9, up from 49.2 in the previous month and slightly surpassing the market expectations. Although the latest reading was the highest for nine months, manufacturing output continued to decline for the twelfth consecutive month, albeit at a slightly slower pace. Hopes for a quick economic recovery continue to fade, replaced by reality of a Q1 economic stagnation. The survey also indicated that services inflation eased, which helps support the view of a June rate cut from the ECB.

EUR/USD erased all post-FOMC gains, and then some, following a wave of upbeat US economic data. Analysis of historical data showed that on average US dollar tends to sustainably recoup its losses against the euro after initial post-FOMC price volatility, where we tend to see USD depreciate against most of its G10 peers. Looking ahead, the pair is entering the final day of the week with a bearish conviction, eyeing the 200-day SMA at $1.0838 as its next support level.

Global stocks up 1.6% on dovish central banks

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: March 18-22

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Join us for Convera Live! A series of in-person events discussing the future of global payments.