Written by Steven Dooley, Head of market Insights

Global overview

The US dollar ended strongly higher on Friday after the hotter than expected US inflation reading last week. The Aussie and kiwi both neared lows although the NZD/USD has gained in early Monday trade.

USD stays strong after CPI

The US dollar remained strong at the end of last week after the hotter than forecast inflation reading.

On Thursday, headline annual inflation was higher than expected at 3.7% in annual terms. The market forecast was for 3.6%.

The news saw short-term expectations for further US Federal Reserve rate hikes rise moderately but, on balance, the market still sees the Fed as more likely to hold.

The rising Fed expectations saw the US dollar stronger with the biggest gains versus the Australian and New Zealand dollars. The AUD/USD and NZD/USD both neared 11-month lows.

However, the NZD/USD jumped this morning, up 0.5%, after the weekend’s election results suggested a strong win for Christopher Luxon’s National Party.

The big win suggests Luxon might be able to quickly form government with traditional partner ACT rather than engaging in the weeks of horse-trading that is usually seen after NZ elections.

Bond markets doubt Fed’s resolve

While the last few days saw a jump in near-term Fed expectations, the base case remains that the US Federal Reserve is near an end to its rate-hiking cycle.

Real-time inflation statistics indicate a persistent deflationary tendency, which the Fed’s Raphael Bostic appeared to admit when the government shutdown threatened the release of the October data.

The macro indicators generally indicate a near-term expansion, which is supported by the IMF’s recent upgrade to the US economic forecast.

The most recent Fed commentary suggests that the cycle of rate increases is coming to an end, but bond markets could be waiting for something more formal. All eyes are on this week’s commentary from Fed chair Jerome Powell due on 19 October.

The market is currently pricing in a scenario for 2024 for three rate cuts versus the Fed’s indication of two rate cuts. That said, we are still positive on the DXY index currently.

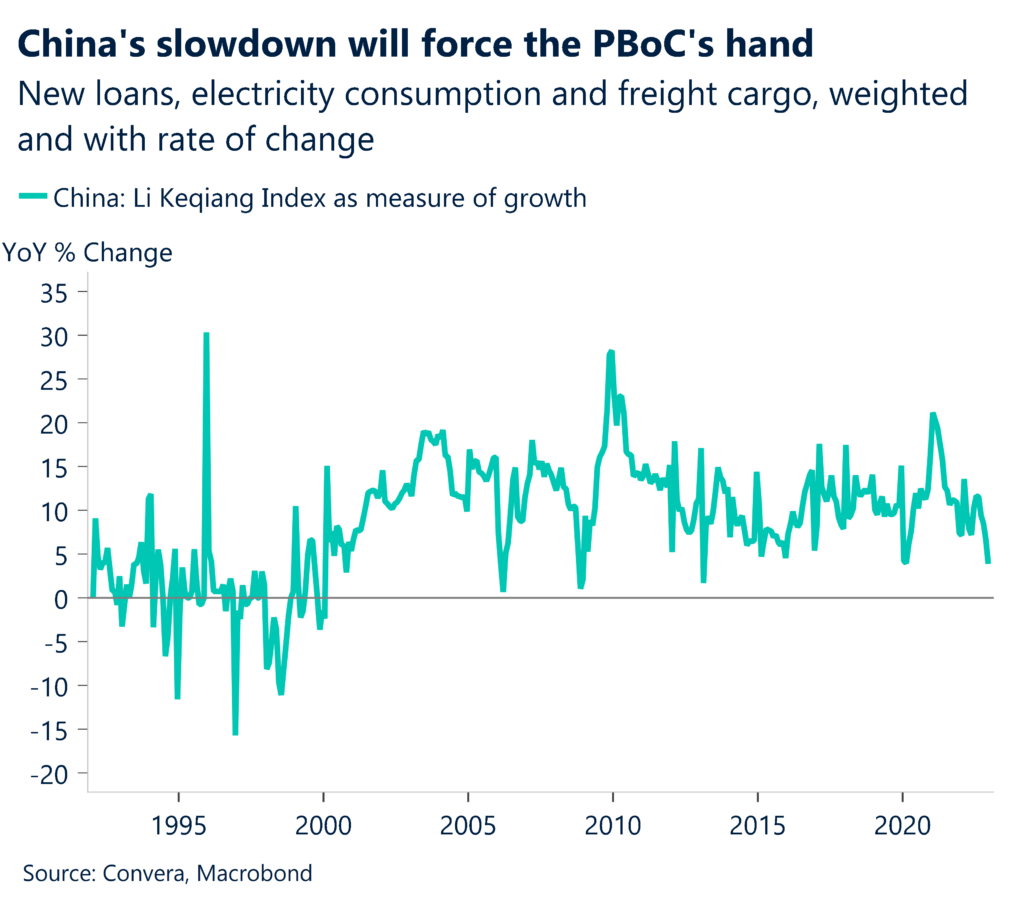

Chinese GDP due

The NZ economy remains in focus early this week with the September-quarter inflation reading due on Tuesday.

The headline quarterly inflation report is forecast to jump sharply – up from 1.1% in the June quarter to 2.0% in September – while the annual rate is forecast to remain broadly steady at 5.9%. A higher-than-expected number might boost the NZD.

From Australia, the highlight is Thursday’s employment report.

In China, it’s a big week, with the crucial September-quarter GDP numbers due on Wednesday. The market is looking for a drop in annualised growth from 6.3% in June to 4.9% in September.

China’s monthly interest rate decision – the loan prime rate – is due on Friday.

Kiwi jumps after election

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 16 – 20 October

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.