US shares refocus on economic data

Markets steadied overnight after the heavy risk sell‑off earlier in the week, even as oil prices continued to climb.

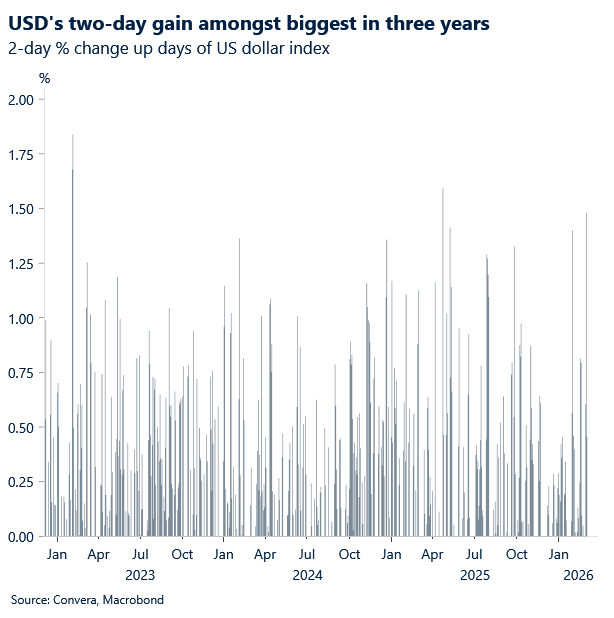

The US dollar eased, with the USD index pulling back after touching its highest level since 27 November during yesterday’s Asian session.

European and US equities rebounded, reversing the sharp declines seen across Asia where Japan’s Nikkei fell 3.6% and the Australian ASX lost 1.9%.

Stronger US data helped lift sentiment. PMIs beat expectations, and the ADP report showed 63k new jobs versus the 50k forecast.

The Australian dollar rose 0.6% against the US dollar, while the New Zealand dollar gained 0.9%. European currencies lagged.

In Asia, USD/JPY fell 0.4%, USD/CNH slipped 0.4%, and USD/SGD eased 0.1%.

Trump warns of Iran leadership risk

President Donald Trump warned that Iran’s new leadership could prove as challenging as the outgoing regime. “The worst case would be we do this, and then somebody takes over who’s as bad as the previous person. That could happen,” he said.

Speaking alongside German Chancellor Friedrich Merz, Trump said he still hopes a more moderate figure emerges, though noted that some of his preferred candidates had been killed. He added that oil and gas prices will stabilise, while offering no clear timeline for ongoing military operations, according to Bloomberg.

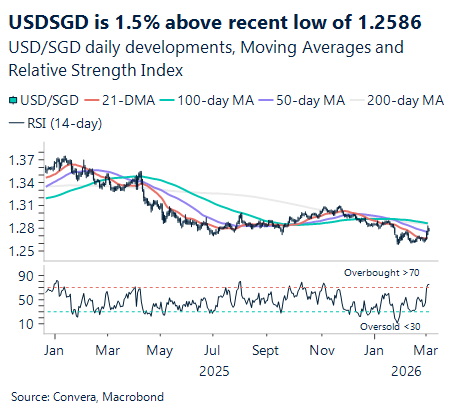

The USD/SGD has risen 1.5% from its recent low of 1.2586 on 28 January.

The next resistance level is the 100‑day moving average at 1.2810.

China PMIs split as private survey outperforms

China’s official manufacturing PMI fell to 49 in February, missing expectations of 49.2 and down from 49.3. New orders weakened to 48.6, and export orders dropped to 45.

Non‑manufacturing PMI, covering construction and services, slipped to 49.5, also below forecasts. Officials attributed part of the softness to the Spring Festival holiday.

In contrast, the private RatingDog survey showed a strong improvement. Manufacturing PMI surged to 52.1, well above the 50.1 forecast, while services PMI jumped to 56.7 against expectations of 52.3. RatingDog said manufacturing is likely to maintain moderate growth in the near term.

The widening gap between official and private surveys highlights uneven momentum across China’s economy.

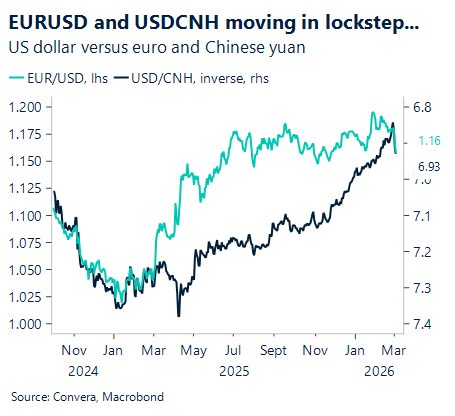

USD/CNH has rebounded 1.4% from its recent low of 6.8267 on 26 February.

The next resistance level is 6.9954, near the 100‑day moving average.

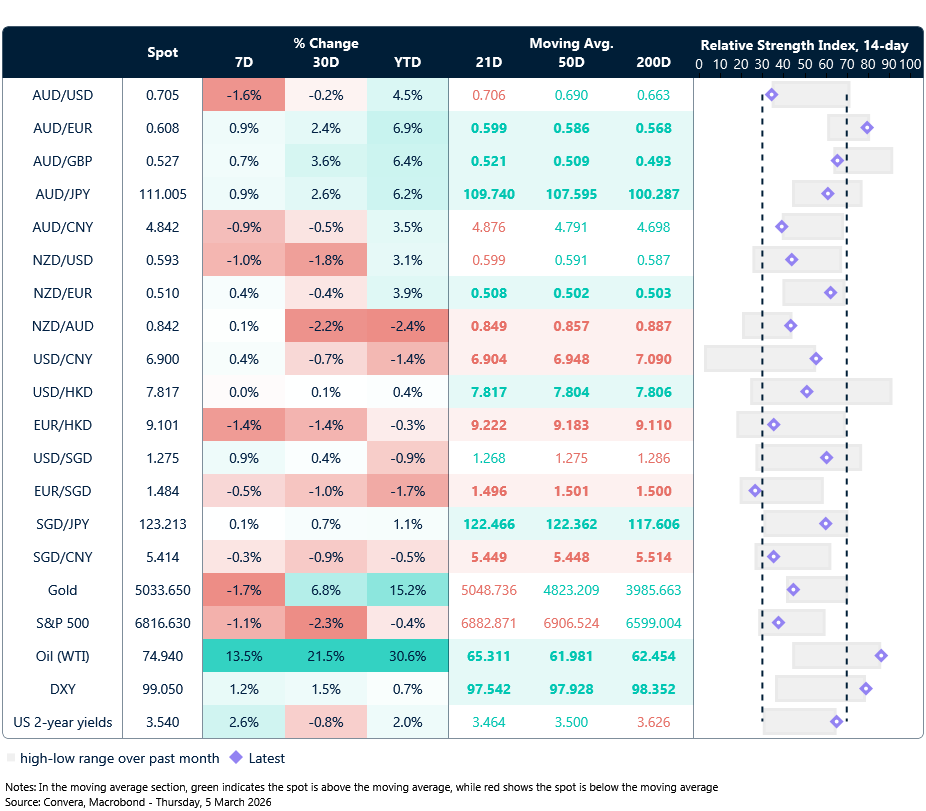

AUD/USD lower, but Aussie gains strongly in Europe, Japan

Table: seven-day rolling currency trends and trading ranges

Key global risk events

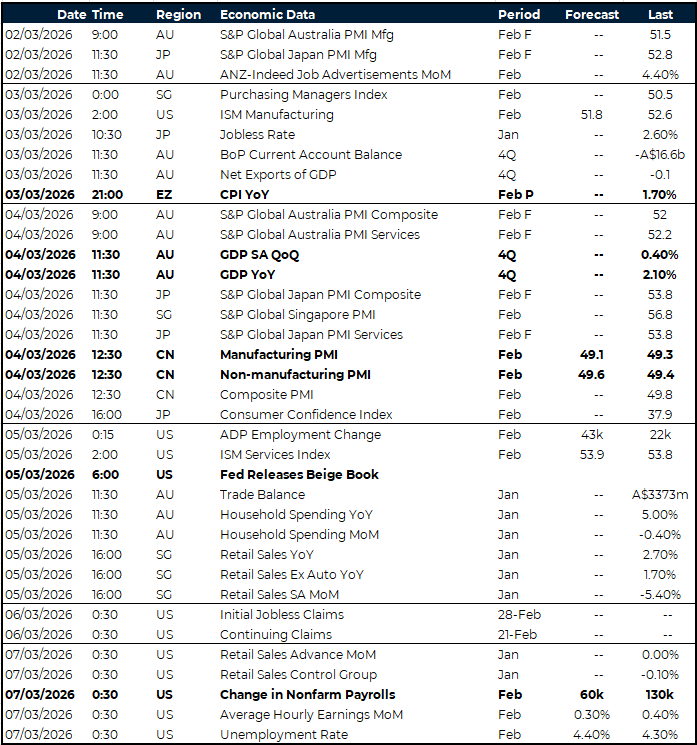

Calendar: 2 – 7 March

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.