Written by Convera’s Market Insights team

Dollar slides into holiday-shortened week

George Vessey – Lead FX Strategist

After a huge week of central bank focus, the new trading week started on a mixed tone. Stocks in the US slipped whilst Bitcoin gained as much 7% on Monday. The yield on the US 10-year Treasury note was little changed around 4.23% and the US dollar index reversed from 1-month highs. We’ve seen a slightly stronger yen as Japanese government officials continued their jawboning to defend the currency.

While the Federal Reserve (Fed) stuck to its projection of three rate cuts this year, other major central banks similarly signalled that an easing cycle was in play. Investors await further catalysts to assess the timing of the Fed’s rate cuts as a slew of mostly second-tier economic data drops in this week. One might argue that the Fed will now be more sensitive to downside risks in the economic data flow than upside outcomes in the data, which could trigger some volatility across the FX space. This is because we’re seeing evidence that the reaction function of the US dollar to incoming US data is asymmetric – whereby the dollar’s sensitivity to strong macro data has been underwhelming relative to its reaction to weaker data, which seems to be moving the currency more. Yesterday saw the Chicago Fed national activity index edged up to a 3-month high, but measures of manufacturing activity in Texas showed concerning declines whilst new home sales unexpectedly fell, which dragged the US dollar lower. Today we have the Richmond Fed index, consumer confidence, durable goods and Case-Shiller home prices to digest.

It’s hard to bet against the USD significantly in the short-term given its high growth and yield appeal, but we do expect its strength to moderate further and a downtrend to resume in the second quarter as investors position for more rate cuts by the major central banks.

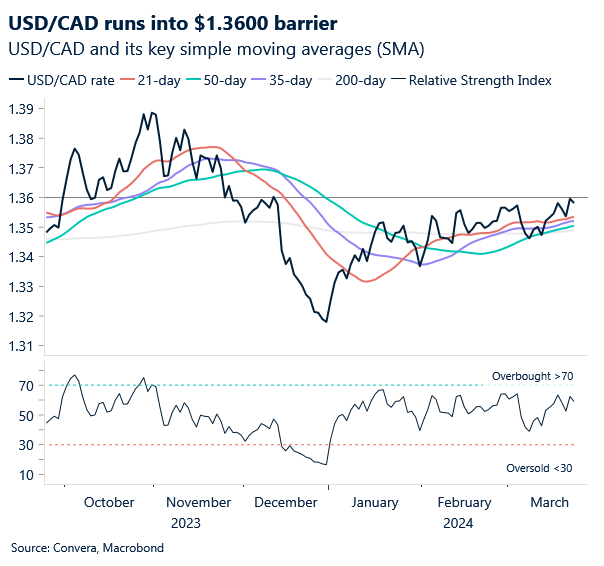

Canadian dollar consolidates losses

Ruta Prieskienyte – FX Strategist

USD/CAD maintains its position in positive territory after paring back some gains on Monday. The pair bounced from $1.3600 threshold, following hawkish remarks from Federal Reserve Bank of Atlanta President Raphael Bostic on Friday. Moreover, the Canadian Dollar continues to face downward pressure as the Bank of Canada (BoC) hinted at potential rate cuts in 2024 in its latest meeting minutes. Deputy Governor Toni Gravelle reaffirmed the central bank’s intention for quantitative tightening to conclude by 2025, highlighting its sustainability amidst gradual interest rate reductions.

The Canadian dollar received support from higher Crude oil prices, which in turn limits the losses of the USD/CAD pair. WTI crude futures rose above $82 per barrel on Tuesday, extending gains from the previous session as various supply-side concerns continued to support oil prices. The Russian government ordered oil companies to reduce their output in the second quarter to meet an OPEC target of 9 million barrels per day after producing about 9.5 million bpd in February. Ukrainian attacks on Russian oil refineries also affected about 12% of the country’s oil processing capacity. In the Middle East, the UN Security Council passed a resolution calling for a ceasefire between Israel and Hamas, although analysts were doubtful that it would stop Houthi attacks on Red Sea shipping that disrupted supply routes.

USD/CAD remains in a bullish trend channel in place since Dec 27, and for now there are few reasons to challenge that. In the short term, $1.3600/$1.3610 looks to be a very firm resistance level, with the pair managing to close above this threshold only 5 out of the past 60 trading days. As the USD/CAD gain in Q1 of +1.85% exceeds the interquartile range for YTD performances over the past 70 years, we should expect to see a slowdown in the velocity of USD/CAD appreciation as it edges towards the elusive $1.3600 barrier.

German consumer confidence at 3-month high

Ruta Prieskienyte – FX Strategist

European equity markets started the holiday-shortened week on a slightly positive note, extending a streak of nine consecutive weeks of gains. The euro bounced off the $1.0800 support level against the US dollar thanks to a broad US dollar weakening and profit-taking ahead of month-end, despite dovish comments from a typically hawkish ECB policymaker fuelling hopes that the bloc’s central bank might start cutting rates soon.

Over the weekend, Bundesbank President Joachim Nagel confirmed that the probability of the Governing Council cutting rates ahead of the summer recess is increasing, as recent inflation print continued to edge closer towards the bank’s 2% target. Nagel’s sentiment aligns with a growing chorus of policymakers advocating for a potential cut in June. Currently, markets are pricing in an 86bps reduction in rates for the year, equivalent to at least three 25bps cuts, with the first anticipated in June with a 72% probability. However, the policymakers continue to caution markets that the June rate cut is not done deal as certainty that inflation would continue to decline is crucial for this to happen. Despite that, the expanding camp dove membership across the Governing Council saw the yield on the 10-year German government Bund dip to around 2.32% during Monday’s trading session, a near-two week low.

Despite yesterday’s bounce, the euro remains fragile to further weakness over the short-term. The latest Gfk print for April saw a third consecutive rebound, but disappointed market expectations dampening EUR/USD ascent. Later today, US durable goods report comes into focus. An upward rebound from last month’s print, which marked the most substantial monthly decline since April 2020, could see EUR/USD break below the $1.0800 barrier and test a 5-week low. Meanwhile, the surprise SNB rate cut last Thursday has heightened speculations that the ECB will soon follow in its neighbour’s footsteps. The two central banks have a history of mimicking each other, although it is normally the SNB which follows the ECB. As markets continue to price in additional policy easing in Q2, further EUR/USD upside remains capped, and the euro is likely to struggle to gain against the US dollar without a fresh impetus.

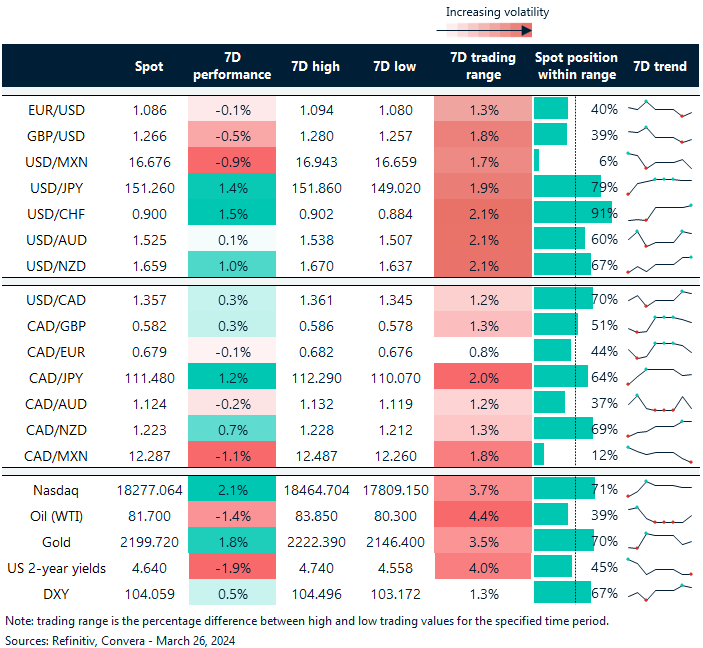

Swiss franc and Japanese yen both down over 1% against the dollar

Table: 7-day currency trends and trading ranges

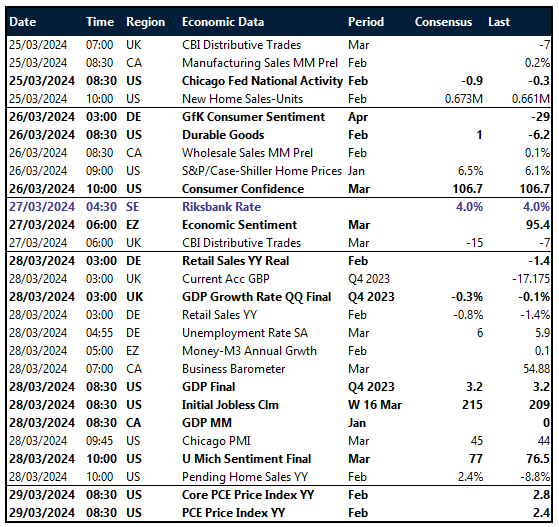

Key global risk events

Calendar: March 25-29

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Join us for Convera Live! A series of in-person events discussing the future of global payments.