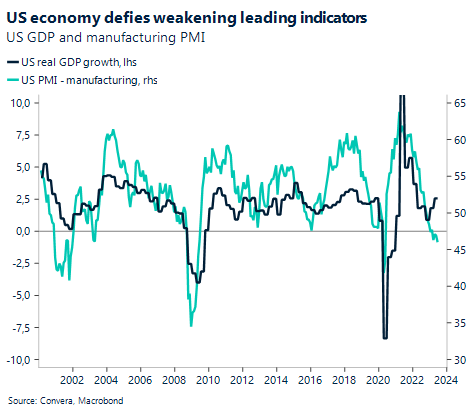

US resilience in the face of a global slowdown

The US economy is much stronger than analysts would have expected going into 2023. This remains the conclusion of this year so far, with yesterday’s data patch confirming the resilience of the world’s largest economy to the tightening of monetary policy over the last 12 months. And while inflation continues to weaken, alleviating some pressure off the Federal Reserve (Fed) to continue raising interest rates, stronger macro data has not given investors much room for pricing in rate cuts for the next several meetings.

The US economy grew by an annualized 2.4% in the second quarter of this year, beating expectations of an 1.8% increase and accelerating from the previous growth rate of 2.0%. New orders for durable goods jumped 4.7% on a monthly basis in June as well, recording the strongest bounce since the middle of 2020. The data patch was accompanied by the release of initial jobless claims, which once again, surprised to the downside. Instead of the expected 235 thousand claims for unemployment benefits, only 221 thousand people registered, the lowest level in five months. While inflation has dominated the debate about how much rates should rise, macro data will decide when which central bank will ease monetary policy again. So far, calls for Fed cuts have faced strong resistance from a resilient economy.

The US Dollar Index is staging a comeback this week, following a strong positive response from the Greenback after a slightly dovish European Central Bank (ECB) surprised markets to the downside. Investors are coming around to the idea that the Fed is not the only central bank starting to think about pausing its tightening cycle. In fact, recent macro data suggests that the possibility of the ECB cutting rates before the Fed are rising, taking the wind out of the euro’s sails.

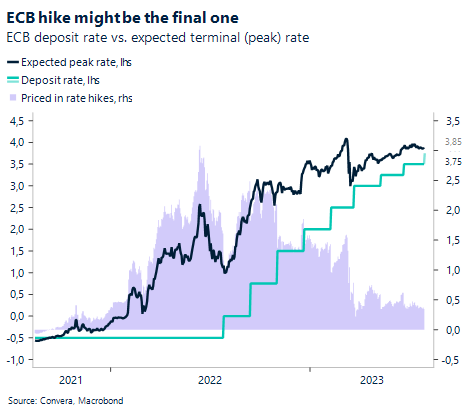

ECB hikes rates amid a weak economy

The ECB raised its benchmark interest rates by another 0.25% at yesterday’s meeting, bringing the cumulative tightening to 425 basis points and lifting rates to the highest level in 22 years. However, Christine Lagarde did raise the possibility of a pause in September given disinflationary forces spreading and economic activity starting to weaken. The euro quickly fell below $1.10 against the dollar following the meeting.

The interest rate decision has been well communicated and anticipated by markets. However, the dovish tilt from Lagarde and the policy statement, which acknowledged the weak economic outlook, dampening optimism, and tighter lending conditions, has made the September meeting an open one. This makes clear that the Fed is not the only central bank that is at or close to the rate hiking peak. The possibility of another increase at the next meeting has fallen to less than 75%. A continued fall of inflation rates will make the current interest rate more restrictive, even if the ECB is done hiking. Coupled with the latest bank lending survey, which showed a continued fall in 1. businesses demand for loans and 2. banks willingness to lend to businesses has confirmed the view that the transmission from tighter policy to tighter private lending conditions has already started.

EUR/USD is trading just below the important $1.10 mark and has closed the short-term gap with our fundamental model for the currency pair. In recent days, we have warned about the move above $1.12 not being driven by rate differentials and that the risk of a correction has increased. At current levels, extreme movement is less likely but today’s releases of German GDP and inflation and US inflation will act as the main catalysts for the common currency.

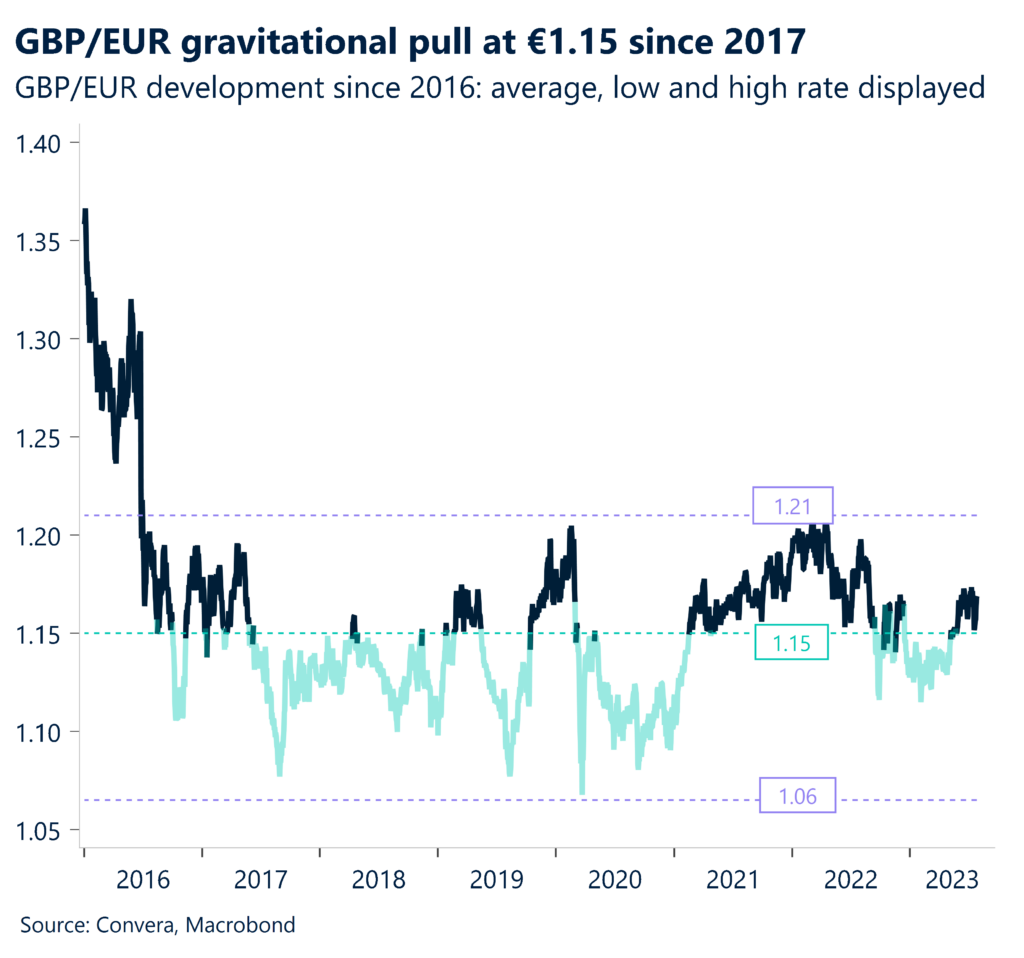

GBP/EUR recoils from €1.17

After the ECB hike yesterday and dovish remarks from Lagarde, GBP/EUR climbed for several hours to brush the €1.17 handle. Momentum to the upside stalled though as sterling traders prepare for the Bank of England’s (BoE) meeting next Thursday.

After dropping over 2% in six trading days from a circa 10-month high, the pair found support at €1.15 last week – its key 100-day moving average. Sterling then retraced up to 76.4% of that drop before recoiling in the later hours of yesterday. The technical set up on the daily chart looks bearish, but the higher low and higher high on the weekly chart is bullish. Thus, amidst hints of market indecision, we expect a continuation of the €1.15-€1.17 range for now. The BoE decision next week is the next important trading point for sterling. With the better news on UK inflation recently and investors reining back rate expectations, a 25-basis point hike looks marginally more likely than a 50-basis point hike. However, the strength of the services sector continues to drive strong pay growth and input costs, mitigating disinflationary pressures elsewhere, and likely keeping the pressure on the BoE to hike again after next week. This should be supportive for sterling in the short-term.

Meanwhile, although GBP/USD has fallen under $1.28 (after strong US GDP data yesterday), the currency pair has bounced off the support of an upward sloping trendline that’s been intact since last October. Unless we see a clear break to the downside, this could be seen as a decent entry point for GBP bulls.

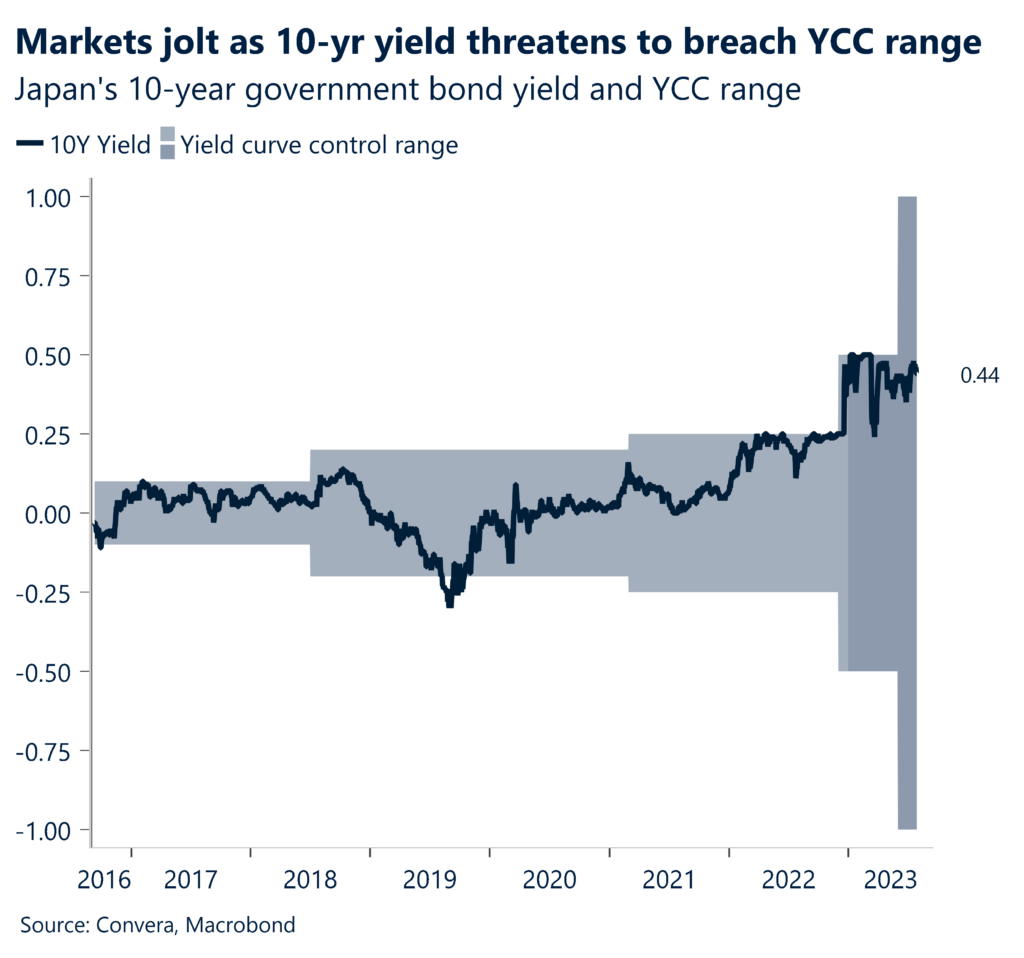

Yen rallies after BoJ tweak

Finally, we witnessed volatile swings in financial markets over the Asian trading session after the Bank of Japan (BoJ) announced it will make its yield curve control policy more flexible. The Japanese yen has already swung over 2% today against many peers including the USD, EUR and GBP.

Japan’s central bank kept its short-term interest rate target at -0.1% as expected and the target for 10-year government bond yields around 0%. However, it also added that its 0.5% ceiling was now a “reference point, not a rigid limit” and it will manage the curve “flexibly” by buying government debt at 1% each day rather than 0.5%, suggesting this might be the new line in the sand. This is what caught investors off guard, sending the benchmark yield surging and the yen into a spin, diving lower at first before reversing course and rallying.

It’s not a clear tightening step by the BoJ, hence the whipsaw reaction across financial markets, but the surprise move calls into question the BoJ’s Governor’s communication and raises the probability of an end to its yield curve control policy, which should ultimately favour the yen.

Dollar rebounds after strong US data

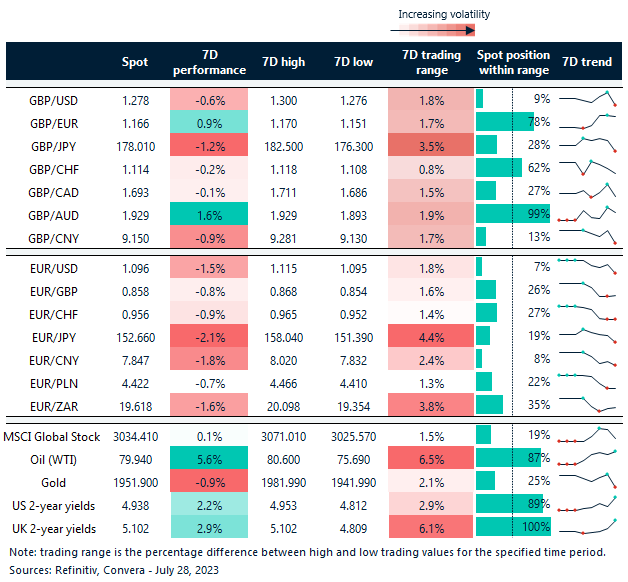

Table: 7-day currency trends and trading ranges

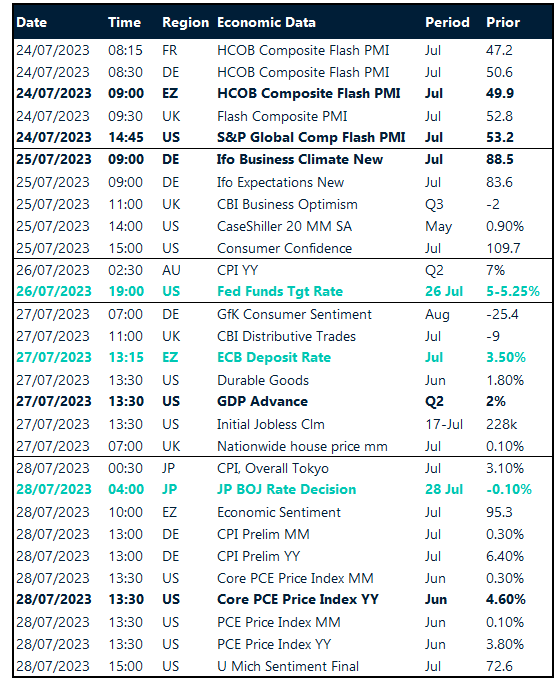

Key global risk events

Calendar: July 24-28

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.