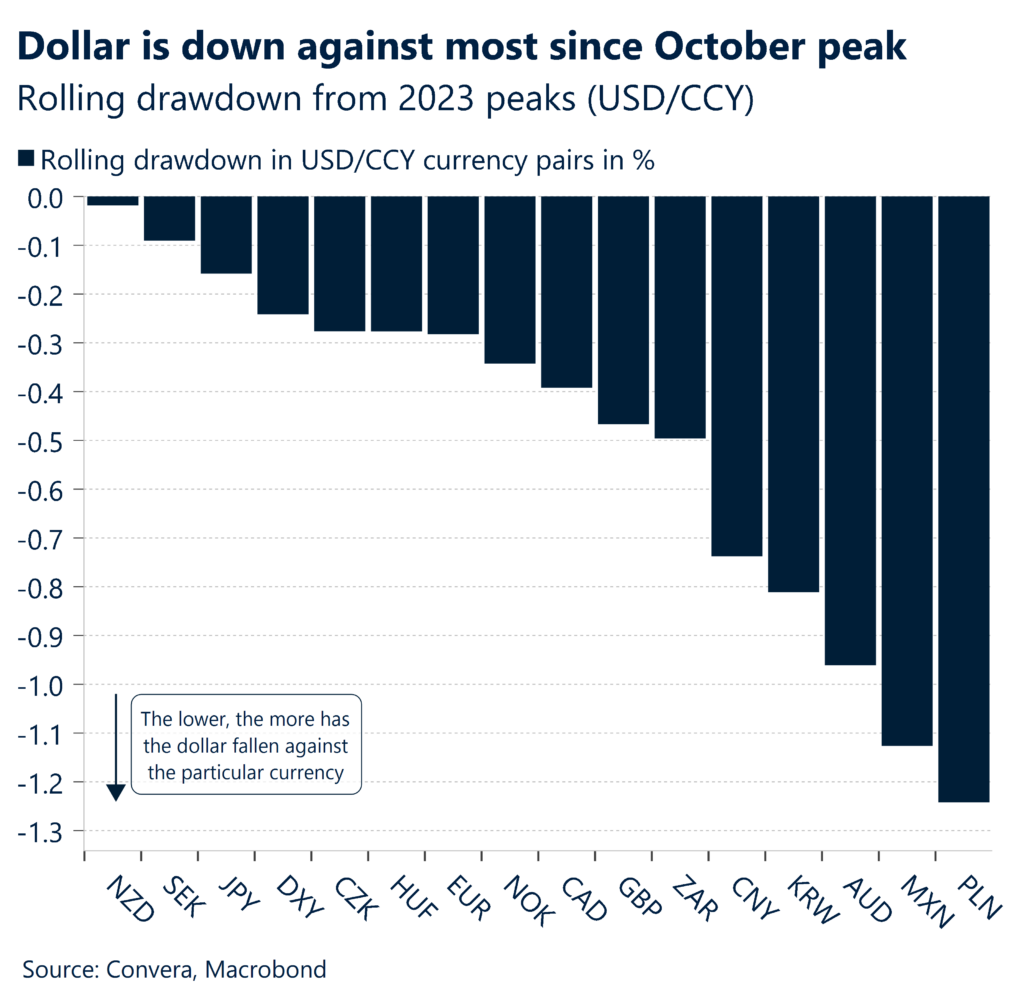

Equity rally helps Aussie, kiwi find support

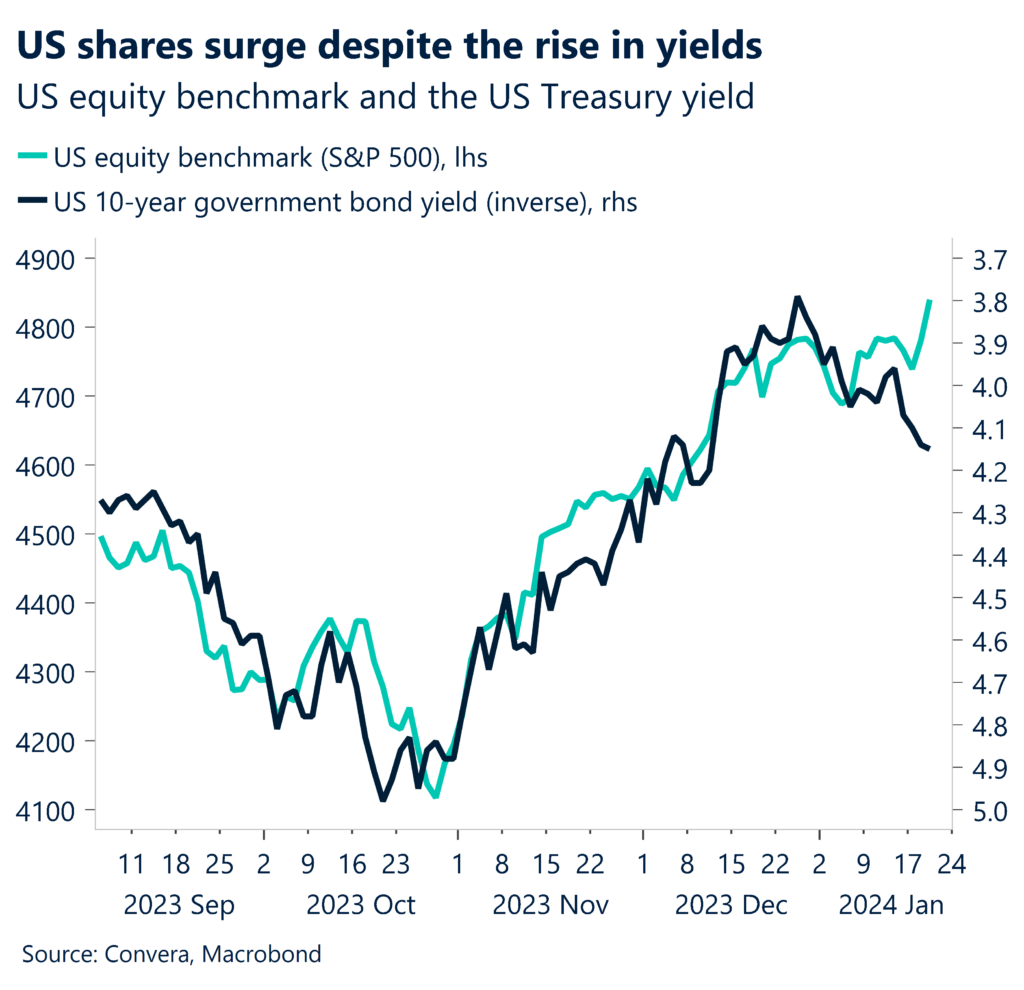

US shares hit new all-time highs on Friday as a combination of better US economic data and hopes for Federal Reserve rate cuts buoyed sentiment.

The positive environment helped risk-sensitive currencies like the Australian and New Zealand dollar outperform on Friday after a mostly negative week.

Both the AUD/USD (at 0.6520) and NZD/USD (at 0.6080) found support at the two-month lows. These levels will be key for the currencies’ performance this week.

Also key across markets, this week’s procession of major central bank decisions, with the People’s Bank of China decision due on Monday, Bank of Japan on Tuesday, Bank of Canada on Wednesday night and European Central Bank on Thursday night.

US dollar short-term strength nears extreme

Growing monetary headwinds, diminishing fiscal offsets, and post-pandemic tailwinds should all cause US GDP to drop to below trend in 2024. We do not see inflation returning to 2%, and a weaker labor market will be necessary to achieve the “last mile” of lower inflation. The Fed might be forced to maintain mildly tight policy .

In the end, the development of data will continue to present two-way risks for the FX market, despite the efforts of certain Fed officials to moderate the overall dovish message to little effect. Furthermore, risk aversion may temporarily strengthen the USD in the event that growth begins to stall more noticeably, especially when compared to higher beta currencies. For the time being, other anticipated concerns pertaining to US elections, commodity prices, and global economy are still there.

Nevertheless, in the short term, with the DXY’s relative strength index move towards the 70 – a sign of stretched momentum – there’s growing risk of reversal lower for the greenback.

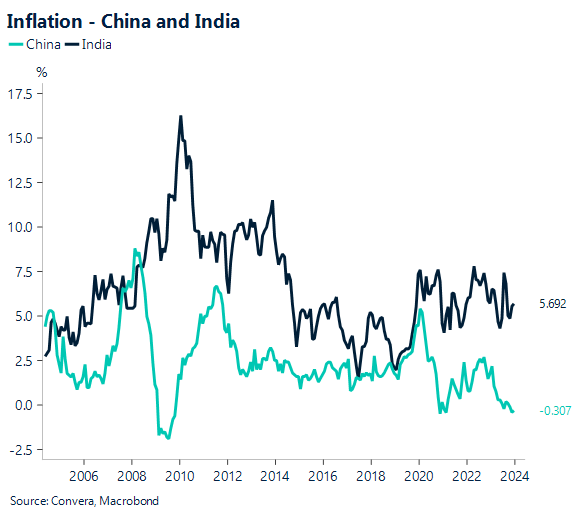

China policy in focus

Today’s major decision from the People’s Bank of China is seen as key after the central bank defied market expectations last week and kept the medium-term lending facility (MLF) steady.

The Chinese economy might see a small lift in the first half, before moderating in the second half of 2024.

Because of the shifting dynamics in the price of commodities globally, we anticipate that deflation will cease in 2024. Despite this, low inflation in China will likely continue because of policy assistance that is skewed toward production rather than consumption.

A worsening net foreign direct investment picture, increased portfolio outflows, and a growing tourist deficit might jeopardize CNY’s growth trajectory.

On the other hand, a more thorough and persuasive governmental response may tip the odds in favor of a greater and longer-lasting CNY appreciation.

Aussie, kiwi find support at two-month lows

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 22 – 27 January

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.