Global overview

US shares extended their monster winning streak after last week’s Federal Reserve decision boosted optimism. The US dollar, however, rebounded from two-month lows as European data disappointed and commodity prices fell.

US shares hit record winning streak

US shares completed their seventh straight winning session overnight – the best run in two years – as markets cheered hopes that the US Federal Reserve might be near the end of their rate-hiking cycle.

The S&P 500 gained 0.4% while the Nasdaq jumped 1.0%.

In FX markets, however, the US dollar’s recent weakness paused, with some poor European data, falling commodity prices and a cautious statement from the Reserve Bank of Australia weighing on key markets.

Most notably, weaker commodity prices have dominated headlines, with crude oil down another 4.2% overnight, and falling to three-month lows.

In Australia, despite a 25-basis point rate hike from the Reserve Bank of Australia, the Aussie couldn’t hang onto recent gains.

New RBA governor Michele Bullock took a step to a more “data dependent” phase by saying, “whether further tightening will be required…will depend on the data.”

The AUD/USD fell 0.9%

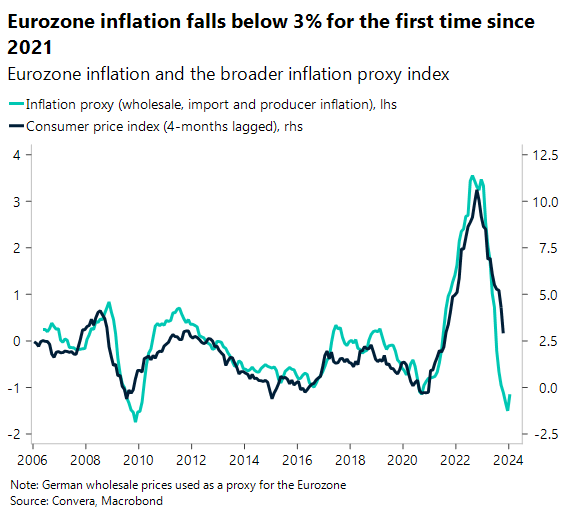

Consumer inflation expectations a risk for ECB

The euro might see further weakness today. As spot inflation has been declining since the euro area’s inflation high in October 2022, we anticipate that the ECB’s consumer forecasts survey for September will reveal a fall in one-year inflation forecasts.

The ECB, on the other hand, will pay more attention to longer-term expectations. Longer-term expectations increased in the last two polls, and the ECB will obviously like to see this start to decline once again.

The risks look skewed to the downside for the EURUSD in the medium term (given growth underperformance vs the US).

UK jobs key for GBP

Given the partial incapacitating effects of the UK’s official Labour Force Survey (LFS) (recent changes have impacted the data), further attention will be paid to alternative labor market information, such as the Report on Jobs, a co-release from KPMG and the UKK’s Recruitment and Employment Confederation.

To get a better idea of the UK’s economy position, we’ll be looking at these three issues. 1) Has the permanent placements index bottomed out, having rebounded to 45.1 in September? 2) The wage and salary growth index is still slowing down; it is currently at 57.6, only a point above its pre-Covid average; 3) The demand for workers also declined, falling below 50 for the first time since early 2021.

In terms of monetary policy, the BoE is somewhat more aggressive than the ECB. Although the UK and the euro area are both experiencing slow economic development, we believe that the UK is less likely to have a recession.

From a technical analysis standpoint, the risk-reward on a downward move seems greater since EUR/GBP is now around the peak of its range over the last six months. This suggests a period of GBP outperformance – at least in Europe.

USD bounces back

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 6 – 11 November

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.