Dollar shines on robust US economy

The US dollar climbed to a 6-month high against a basket of currencies following US data that showed the services sector surprisingly picked up steam last month. New orders and prices paid in the high 50s were the standout contributors to the ISM services PMI. Short-dated Treasury yields climbed, and the 10-year remains around 4.3%.

The services PMI reading above 50 indicates growth in the services industry, which accounts for more than two-thirds of the US economy. The prices paid component rising to 58.9 from 56.8 is a concern for the Federal Reserve (Fed) and is likely to keep the hawks wary even if there does seem to be a consensus amongst officials that it can afford to pause in September and assess the situation again in November. The market continues to discount rate cuts, but nowhere near to the extent they once were. In fact, the path of least resistance is pointing higher for US yields, which should keep the dollar well supported over the next few months.

Fed policymakers view the services sector as key to bringing inflation down to their 2% target, and so the ISM report does little to bolster the view that any slowdown is underway. The main focus on Thursday is likely to be the US jobless claims data and another busy slate of Fed speakers.

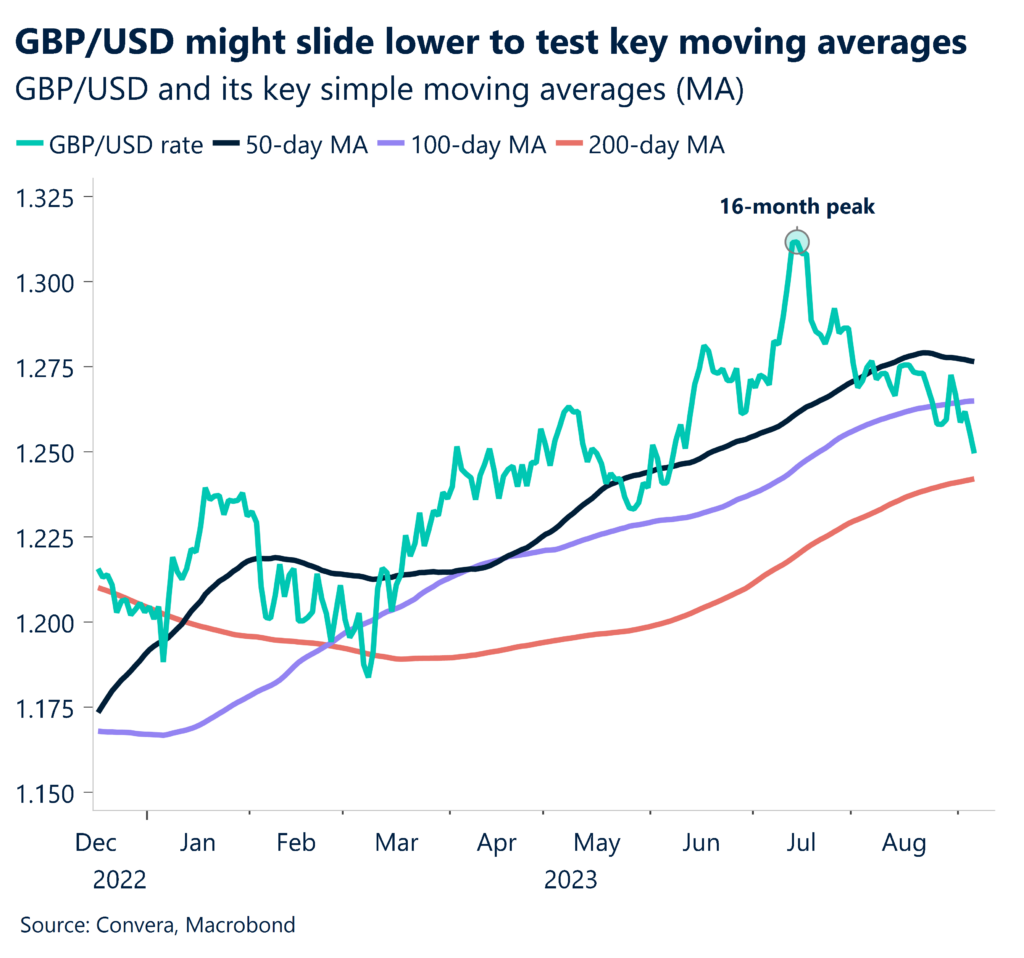

$1.25 gives way, what next for GBP/USD?

As we warned yesterday, a test of the $1.25 level for GBP/USD was brewing and the key psychological level did indeed give way. The 200-day support, located at $1.2425, could be the next short-term target as questions about the UK interest rate trajectory weigh on sterling. GBP/EUR also suffered, sliding back into the €1.16 area.

Bank of England (BoE) policymakers have recently taken a less hawkish stance, with Governor Andrew Bailey yesterday stating that a large amount of the impact of past rate rises are still to come and we are much nearer the peak of rates. Although the UK economy has been resilient so far, we think it will struggle to generate momentum due to the effects of higher interest rates ratcheting up, persistent inflation, and tight fiscal policy. There does seem to be a belated sense that BoE hiking is biting as there are more signs of a looser labour market both in terms of demand and supply. However, strong wage growth and core and services inflation are proving sticky and it seems too early to declare victory over the fight against inflation.

Today, the latest Decision Maker Panel survey from the BoE is due. The survey asks chief financial officers a range of questions about their expectations, notably on inflation. Will cooling inflation expectations send sterling to fresh 3-month lows?

Stagnation worries mount in Europe

Whilst we continue to see US exceptionalism, the situation in Europe remains bleak. German factory orders plunged 11.7% month on month in July, the steepest pace since April 2020. This morning, we’ve seen that industrial production shrunk 0.8% month on month, providing more evidence of elevated recession risk for the German economy. EUR/USD is hanging on to $1.07 by a thread.

Stagnation in industry and the broader economy looks like the new normal for Germany – Europe’s biggest economy. In fact, the full batch of hard German macro data for July suggests that the risk of recession is high again. Retail sales, exports and now also industrial production all dropped in July, giving the German economy a very weak start to the third quarter. Meanwhile, German companies have never been more pessimistic about the country’s international competitiveness. All of this bodes ill for the euro and the negative bias is likely to persist in the short-term. However, the common currency may find support if the European Central Bank (ECB) opts to raise rates this month. ECB policymakers have recently talked up the chances of more rate hikes, even for this month, stating markets were underestimating this probability.

While a continued slowdown in the Eurozone is sure to damp demand, the fight against inflation is far from over and a 10th straight hike by the ECB remains a close call. EUR/USD is on track to slump eight weeks on the trot, shedding nearly 5% in the process. The next key downside target could be the 50-week moving average located at $1.0670.

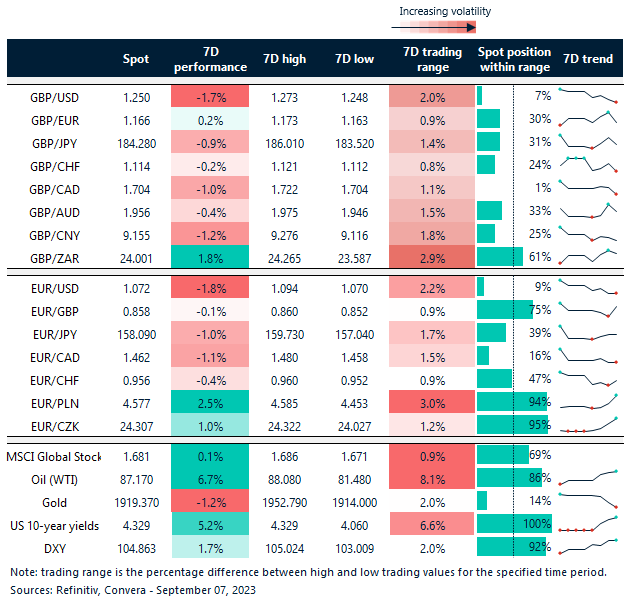

USD up nearly 2% vs. GBP & EUR

Table: 7-day currency trends and trading ranges

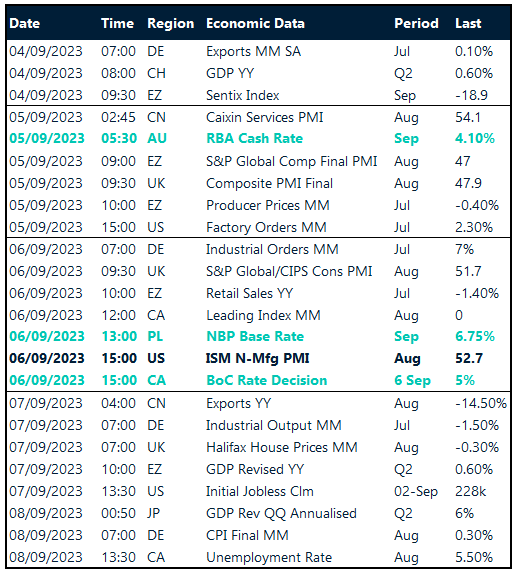

Key global risk events

Calendar: September 04-08

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.