USD: Momentum remains fragile in US labor market

The U.S. labor market showed signs of a modest but uneven recovery in December, with private companies adding 41,000 workers. While this marks a stabilization following the significant contraction in November, which was revised down to a loss of 29,000 jobs, the figure missed economists’ median forecast of a 50,000 gain. According to the data released by the ADP Research Institute in collaboration with the Stanford Digital Economy Lab, the print landed within the lower end of the forecast range (+10,000 to +80,000), suggesting that while the bleeding from the previous month has stemmed, momentum remains fragile as the year turns.

The recovery was driven entirely by the service sector and medium-sized businesses, masking profound weakness elsewhere. Service-providing industries added 44,000 jobs, effectively offsetting the loss of 3,000 positions in the goods-producing sector. By firm size, medium-sized establishments (50-499 employees) were the primary engine of growth, contributing 34,000 jobs, while small businesses added 9,000 and large corporations remained essentially flat with just 2,000 additions. Regionally, the data reveals a stark geographic divide: while the South (+54,000) and Northeast (+40,000) posted solid gains, the West was a massive drag on the national total, shedding 61,000 positions.

Financial markets reacted defensively to the softer-than-expected data, signaling concerns over the pace of economic growth. In the Treasuries market, the 10-year note rallied, with yields declining by 3 basis points as investors sought safety. Meanwhile, equity futures pointed to a lower open, positioning stock markets for their first retreat of 2026. Despite the lackluster jobs numbers, the greenback was fairly unchanged immediately following the release but remains well-bid for the week, holding onto recent gains.

Despite the softer ADP print, the implied probability of a rate cut at the January 28 meeting held steady at 16%. Investor focus now shifts to the week’s primary catalyst: the December Non-Farm Payrolls (NFP) report. Consensus estimates project an addition of 66,000 jobs, with the unemployment rate expected to edge lower to 4.5%. These figures will be critical in determining whether the Fed views the current labor cooling as a controlled descent or a signal for further easing.

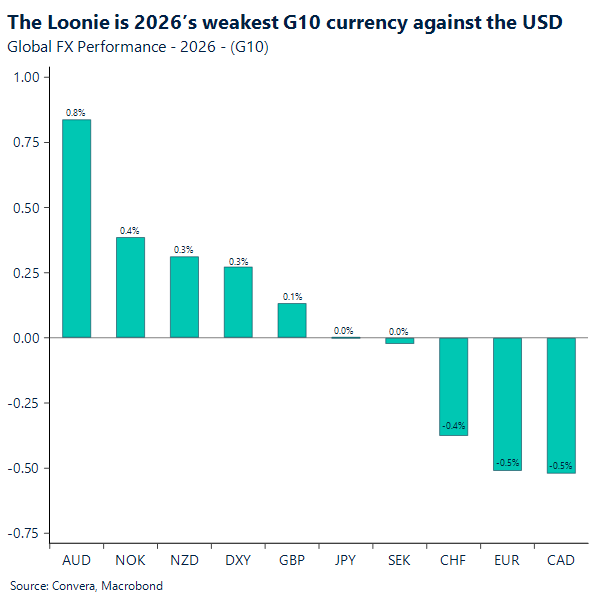

CAD: Tail risks back on the table

Since the start of the year, the Canadian dollar has led G10 currencies in losses against the USD. On one hand, the prospect of Venezuelan oil replacing some Canadian supply has prompted a reassessment of previously bullish 2026 CAD views. While most Canadian crude shipped to the U.S. moves through the Midwest, not the Gulf Coast, where competition with Venezuelan barrels would be more direct, markets are still pricing in a loss of leverage ahead of the CUSMA review. It may feel far off, but the process begins this summer, and trade risks are once again making the CAD less attractive.

Local markets are also turning cautious ahead of Friday’s domestic employment report, where the unemployment rate is expected to show a modest year‑end uptick for 2025. That added layer of uncertainty is reinforcing the defensive tone around the currency.

At the same time, the first full trading week of 2026 is seeing renewed USD demand ahead of key U.S. employment data due Wednesday and Friday. Markets aren’t jittery, but with the geopolitical landscape being reshuffled, previously flat tail risks are back on the table, prompting investors to reassess their early‑year views.

MXN: EM smash records to start 2026

Emerging markets have delivered a historic performance in the opening days of 2026, with the MSCI EM index (MXEF) surging 4.25% in just four trading sessions—the strongest start for the asset class since 2009. This breakout marks a definitive “regime shift” away from the decade-long dominance of US equities, as investors rotate into undervalued international assets. The rally is being powered primarily by the Asia tech sector and AI-linked semiconductor stocks, which have attracted massive inflows and pushed regional indices like South Korea’s KOSPI to significant gains. While this concentration in tech has left momentum indicators like the 14-day RSI in overbought territory, market participants are currently prioritizing high-fidelity earnings delivery and supportive global financial conditions over technical overextension.

This broad enthusiasm for emerging markets has translated into a robust start for the Mexican Peso, sustaining the “Super-Peso” narrative via a “carry-plus-credibility” framework. As the US dollar softens against emerging currencies—evidenced by the USD/CNH breaking below 7—the Peso has benefited from its status as a high-yielding, policy-supported currency. However, this strength faces a dual-threat “bear case” that could test its resilience: a widening policy divergence between a cutting Banxico (currently at 7.00%) and a pausing Fed, and the potential for a rapid reintegration of Venezuelan heavy crude. If the U.S. administration successfully “fast-tracks” Venezuelan infrastructure reconstruction within a 24-to-36-month window, the resulting supply glut could squeeze Mexico’s trade surplus and trigger a “haven rotation” back to the USD, potentially pushing the MXN past the 18.00 support level toward a fundamental re-rating.

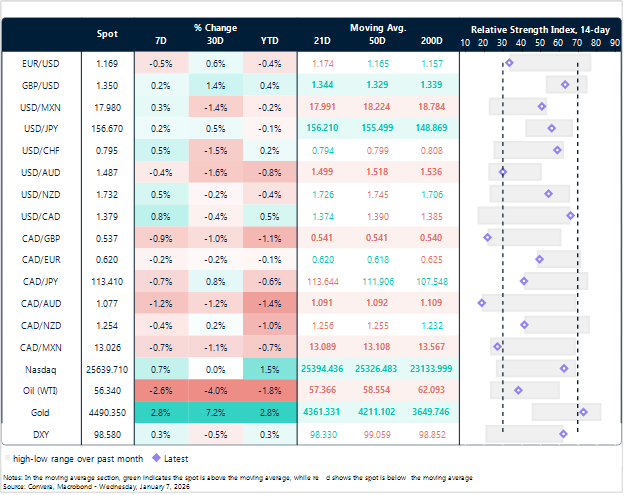

Market snapshot

Table: seven-day rolling currency trends and trading ranges

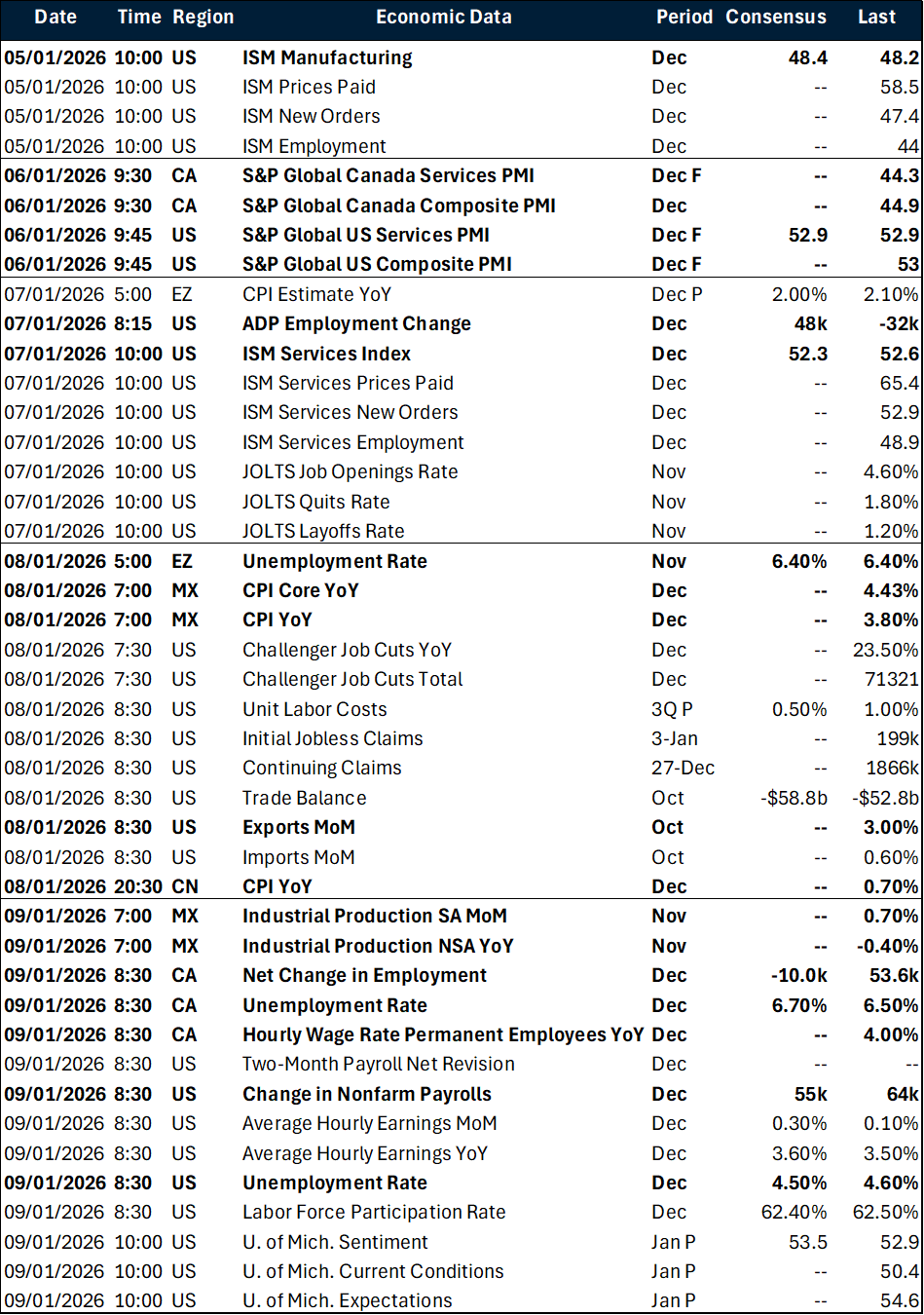

Key global risk events

Calendar: January 5 – 10

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.