Dollar flops after NFP miss, inflation eyed

The US dollar came under selling pressure last Friday following the relatively benign jobs report. There was a modest relief rally in stocks and a slight unwinding of the recession trade in the bond market, whilst EUR/USD jumped back above $1.09 to secure a secondly weekly rise in a row.

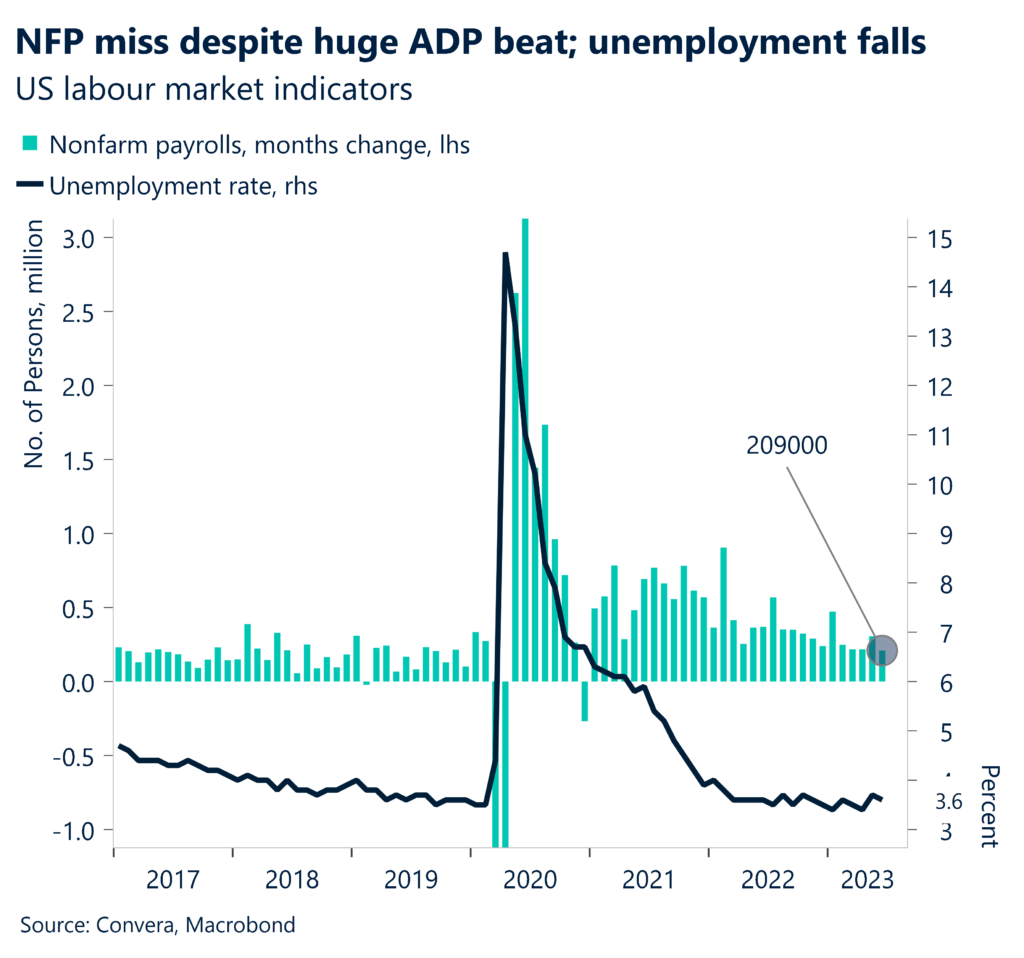

Despite the huge beat in US private payrolls, the non-farm payrolls (NFP) figure increased 209k in June, the weakest increase since December 2020 and missing market expectations for the first time in 15 months. Moreover, job growth for the previous two months was revised down significantly. Downside surprises are relatively rare these days, so the cooling of jobs growth came as a welcome relief as it did not further inflame inflation fears. However, while the US Federal Reserve (Fed) will be encouraged by the slowdown in job growth, details in the employment report reflected persistently strong wage growth and a tick lower in the unemployment rate to 3.6%, both pointing to still-tight labour market conditions. The 2-year Treasury yield, which is highly sensitive to policy expectations, slipped back under 5%, weighing on the US dollar, although after weak China inflation data this morning, the dollar is back on the offensive whilst the yuan and Antipodeans soften.

This week, the primary focus in the US will be on the CPI figures. The headline annual inflation print is projected to decline to 3.1% in June from 4% in the previous month, while the core index may fall to 5% from 5.3%. We’ll also keep a close eye on producer prices and the preliminary estimate of Michigan Consumer Sentiment. Finally, the second-quarter earnings season will start, with reports from prominent financial institutions, which could drive global risk sentiment too.

Strong sterling awaits UK labour market data

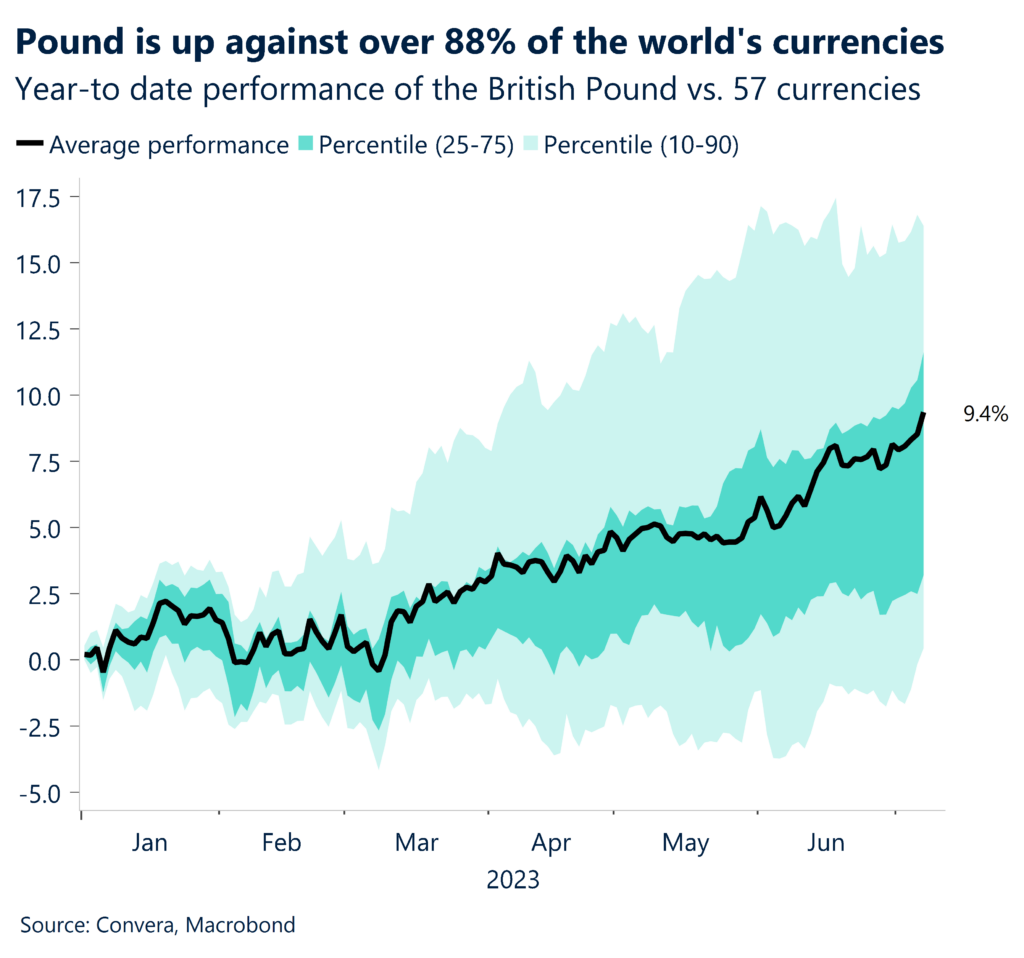

Despite the lack of UK data last week, bets on Bank of England (BoE) rate hikes continued to rise – with peak rate expectations of 6.5% being priced in for early next year. The difference between the 12-month expected policy change of the BoE and Fed has risen markedly as a result and has led the interest rate-sensitive two-year bond yield in the UK to rise above 15-year highs, boosting GBP/USD towards fresh 15-month highs atop $1.28.

GBP/EUR also rose to its highest level since early September last year as the pound remains stronger than 88% of 57 currencies globally year-to-date, averaging over an 8% gain against these peers. Versus its one-year average rates, currently, GBP/USD is 5.7% higher, GBP/EUR is 1.8% higher, while GBP/JPY is a massive 10.3% higher. Interestingly, because of surging UK gilt yields amid rising interest rate expectations, the FTSE 100’s dividend yield has fallen below the UK 10-year yield. Hence, demand for UK stocks remains subdued, whilst demand for sterling remains buoyant as it’s the highest nominal yielder within the G10. However, as speculative positioning on the pound appreciating has shifted higher by the most out of any other major currency recently, this brings with it a downside risk due to a potentially overcrowded trade spurring profit taking in the near future.

UK jobs data, and in particular wages, will be a focus early tomorrow morning. Rising wages remains a concern for the BoE and its fight against inflation, hence money markets are currently pricing a near 70% chance of the BoE hiking by another 50 basis points next month. We also have monthly UK GDP data on Thursday, but this is unlikely to impact the BoE’s decision, with focus primarily on Tuesday’s jobs report.

Euro jumps on weaker US jobs report

Last week’s macro data continued to highlight the slowdown of economic activity in Europe, with the block’s purchasing managers index (PMI) falling to the lowest level year-to-date. Recently, we asked the question if it would be more likely for the services sector to fall to the recessionary level of manufacturing or for manufacturing to be pushed up into expansion again by the resilience of services. The recent data releases point to the former, with the services PMI having fallen from 55.1 to 52.0 in June.

Weaker economic data has so far gone unnoticed at the European Central Bank, which is forced to continue hiking interest rates against the backdrop of elevated core inflation. While both the Fed and ECB are expected to raise policy rates in July by 25 basis points, the meetings in September seem to be more open for surprise. Members of the Governing Council have clearly stated their commitment to fight inflation going forward. However, some policymakers have suggested that nothing is set in stone after the July hike and that the central bank will remain data dependent.

Policymakers have tried convincing markets that the duration of the high-rate regime matters more than where rates will peak in the end. However, the euro has been much more sensitive to developments in the US and China, as the reaction of EUR/USD to the US jobs report on Friday revealed. The weaker number was able to push the currency pair up above $1.0950 again, something that no hawkish ECB member has been able to achieve during the last week.

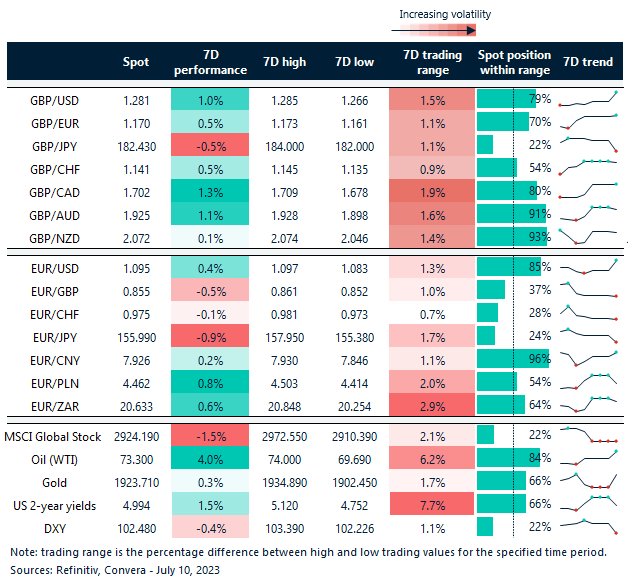

Dollar slumps; GBP/USD up 1% in a week

Table: 7-day currency trends and trading ranges

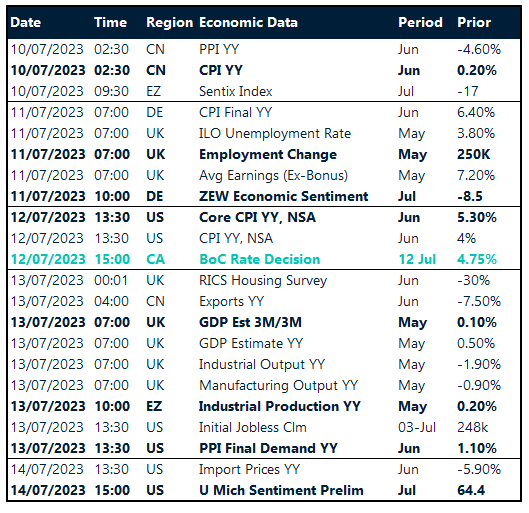

Key global risk events

Calendar: July 10-14

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.