Dollar’s reaction function is now asymmetric

Risk assets including the euro traded slightly lower at the beginning of the week, with attention turning to the release of US inflation. Investors have recently got comfortable with the idea that the Federal Reserve (Fed) would be done raising interest rates. Markets are currently pricing in two rate pauses in June and July, followed by six consecutive rate cuts. The likelihood of this scenario will depend on the incoming data, giving economic figures a significant weight.

US inflation is expected to have remained at 5% in May. If the consensus forecast holds true, this would constitute the first month since June 2022, where headline inflation did not cool on a year-on-year basis. Core inflation is expected to slow from 5.6% to 5.5% and, with little progress in underlying inflation, continue worrying investors about the stickiness of price pressures in the US. Data released on Monday showed how credit conditions continued to tighten during the first three months of the year. In the so-called SLOOS survey (Senior Loan Officer Opinion Survey), which is conducted quarterly, 46% of the banks stated that they had tightened the conditions for loans to medium-sized and large companies. US firms demand for loans declined to the lowest level since 2009.

The US Dollar Index has recently been range bound between 100.80 and 102.40 and has only marginally reacted to incoming data. Given how much rate cuts by the Fed have already been priced in, there seems to be a bias when it comes to data. Better-than-expected economic data will move EUR/USD and other dollar pairs more strongly than data disappointments. This could be beneficial for the dollar, if the data continues to hold up. This gives us an asymmetric reaction function for the US currency.

Rising UK wages to pressure BoE?

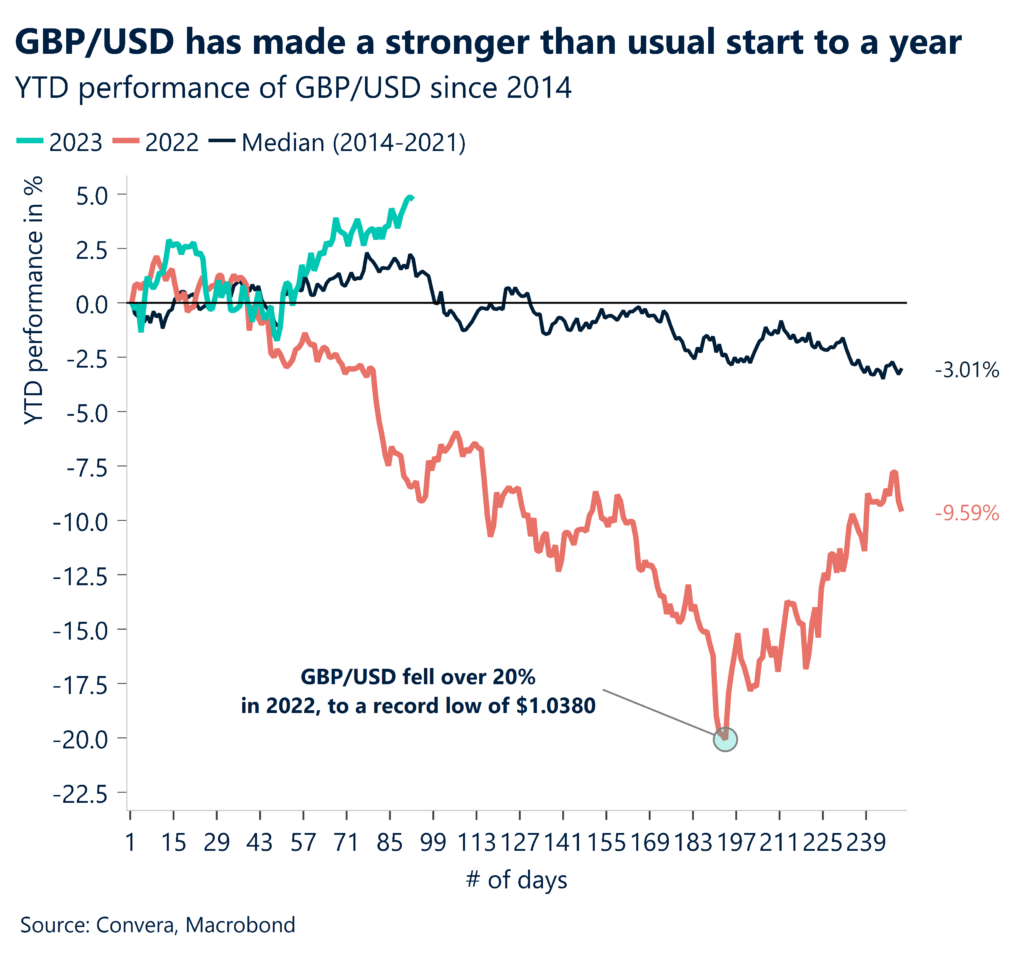

GBP/EUR has opened above €1.15 for the first time since mid-December last year as the euro comes under selling pressure. Sterling is one of the best performing currencies of 2023 though and GBP/USD has risen for seven out of the last eight weeks, consolidating above $1.26 ahead of the Bank of England’s (BoE) pivotal interest rate decision tomorrow. Markets are nearly fully pricing a 25-baiss point hike to 4.5% after hawkish UK inflation and wage data recently.

Reed Recruitment’s job vacancy data through April showed rapid salary gains in the UK as switching jobs appears to have paid off for millions of middle-income UK workers. Wages soared 10% in the past year, just shy of inflation, but pointing to a still red-hot UK labour market. This will concern BoE policymakers, who may look to keep the door open to a June hike after tomorrow’s expected rate rise. The probability of a June hike currently stands at 65%, while a 5% terminal rate is priced at 43%. Some argue that the pricing of BoE interest rate expectations looks excessive, leaving the pound vulnerable. Simply put, given the current market pricing, if the BoE doesn’t deliver on expected rate hikes, or even steers towards a dovish hike tomorrow with a 6-3 vote split, sterling could take a tumble across the board.

Nevertheless, despite the risks skewed to the downside based on market pricing and positioning, the pound appears resilient and may look to test its 100-week moving average just above $1.27 at some point soon. Will the pound’s ~8% rise in six months against the US dollar extend enough to challenge $1.30 this year though?

Positioning is another risk to euro

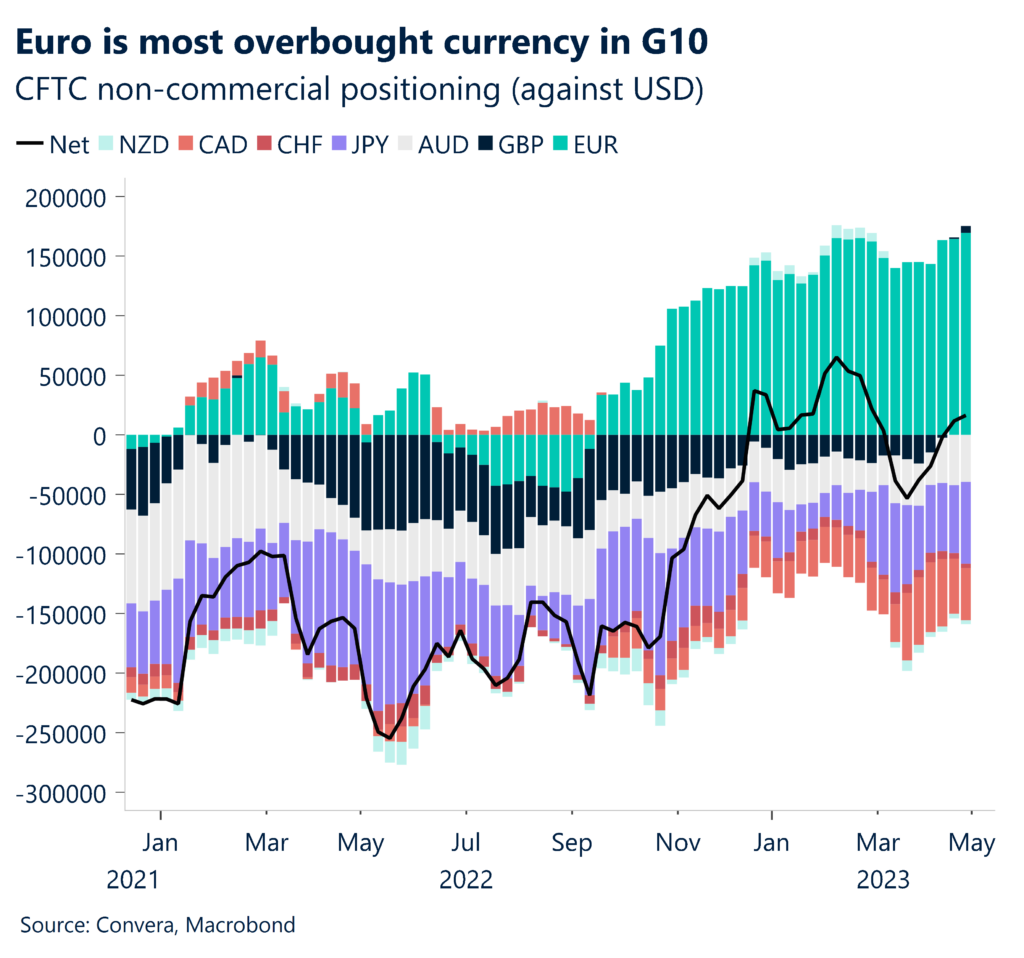

Macro data from Germany has been disappointing lately and markets are paying close to attention instead of listening to the flurry of European Central Bank (ECB) hawks. But another weight on the euro is the fact that the common currency is the most overbought currency in G10 according to the latest CFTC data.

Speculators continued to add net-long positions in EUR/USD over the past few weeks, meaning traders are betting on the euro appreciating against the dollar. This isn’t a major surprise and is a similar story for other currencies versus the dollar, however, the net long positions of euros are now worth 22% of open interest, which is the highest since January 2021. Although this paints a positive view of the euro, it also increases the risk of corrections lower in EUR/USD in the short term. In the longer run, pending divergence in the US-Eurozone economic and monetary outlooks, EUR/USD is still expected to climb towards $1.15, but as ever, timing is everything and since losing its grip on $1.10 this week, EUR/USD may be at risk of sliding further in the near term.

Another risk to the $1.15 call for this year would be spill-over effects from the US regional banking crisis and a global credit crunch, which would likely spur safe haven USD demand. Moreover, the greater the risk of a US recession, the more likely is Europe to be dragged into it as well, as evidenced by the slew of weak European data over the past month.

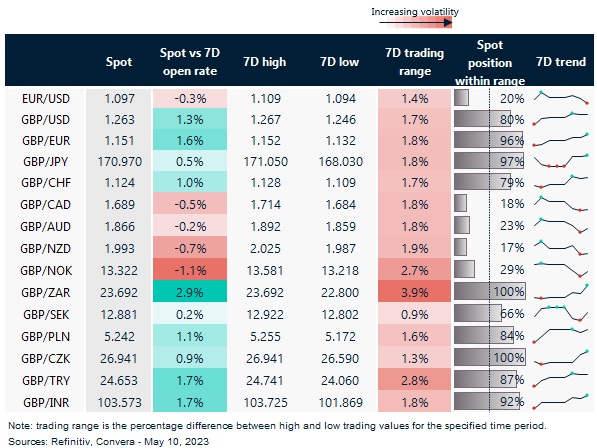

GBP/EUR up 1.6% from last week

Table: 7-day currency trends and trading ranges

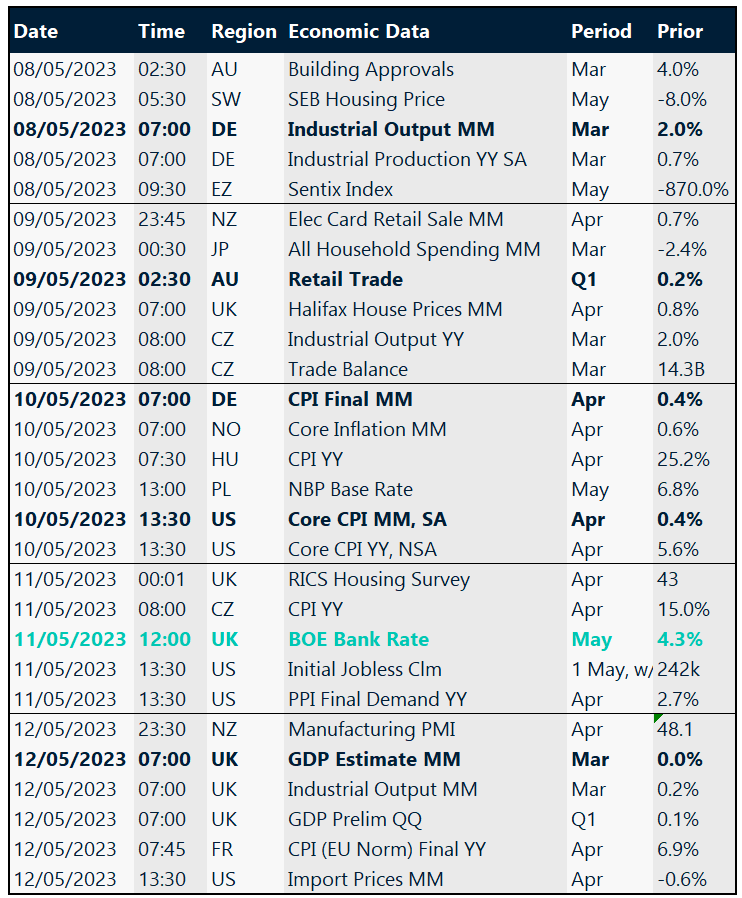

Key global risk events

Calendar: May 8-12

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.