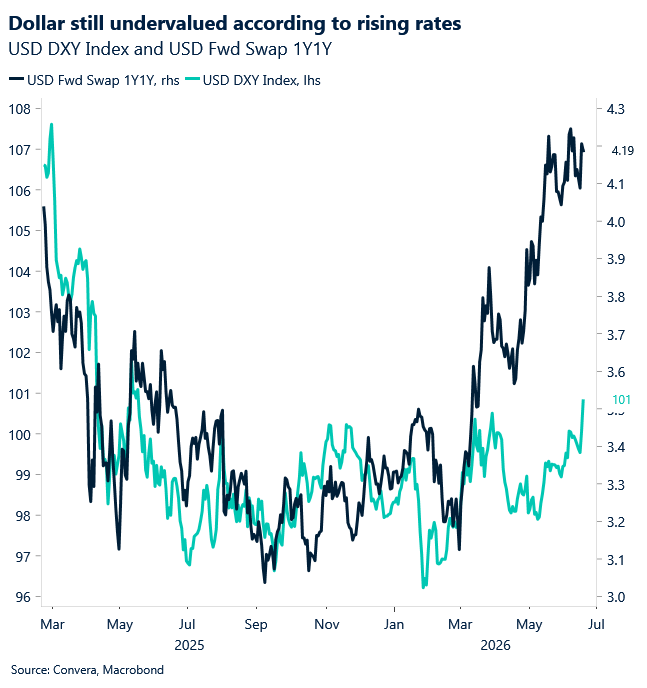

USD jumps to one-year highs

The global focus remains on the US – and not just because of the World Cup — as the US–Iran peace deal took effect, boosting sentiment towards US shares and the US dollar.

The US dollar index hit a one-year high, with the world’s most traded currency also supported by this week’s Federal Reserve decision, which signalled that further US rate hikes are more likely.

After spending the better part of a year trapped in a narrow range, DXY is pressing hard against the 100.50 ceiling. The move reflects a sharper hawkish repricing after the June Fed meeting. By holding rates at 3.50%–3.75% and quietly dropping its legacy easing bias, the Fed forced investors to confront a path they had been reluctant to price: another hike is back in play, and it is no longer a tail risk.

The policy signal, however, is still far from straightforward. Kevin Warsh has already hinted that the Fed’s communication framework may change, leaving markets in an awkward transition. Investors are still leaning on the SEP and the dot plot for guidance, even as the new chair suggests those tools may carry less weight over time. That makes hawkish repricing more potent. When guidance thins out, markets tend to fill the gap themselves, usually with a heavier risk premium.

The front end reacted on cue this week. Two-year yields moved 15 basis points higher, the curve flattened, and the US dollar picked up a clean relative-rate bid. The technical backdrop now gives the US dollar a real shot at testing the top of the range, though calling it a breakout would still be premature. DXY has reclaimed its short-term moving averages and is leaning on the 100.50 level that has capped rallies for much of the past year. Clear that barrier decisively and the market starts talking about a fresh leg higher. Fail here and this starts to look like another failed breakout inside a broader sideways market.

The timing complicates the signal. Month-end, quarter-end, half-year rebalancing and record options expiry are about to hit, which will only add to the noise. Over the next couple of weeks, flows could matter more than macro direction. That is precisely why the latest move matters: a rare two-day dollar surge is testing the range at a moment when conviction and positioning are about to be put under unusual stress.

That leaves the broader macro argument in a tricky place. Crude has retreated sharply from its geopolitical highs, which should, in theory, ease some of the pressure around headline inflation. Markets know that story. More interesting is that the US Dollar rose roughly 2% at the peak of stress in oil and rates back in March, yet it has found a fresh bid even as oil has moved back close to pre-war levels.

The harder question is whether markets are focusing too much on rates and on the broader spread of inflation, rather than on falling oil. Recent US data suggest the pressure is no longer concentrated in energy. It is embedded more broadly across the domestic economy. Core producer measures, including the ex-food, energy and trade-services gauge, are still running hot at 5.1%. That points to inflation that has spread into sticky services, labour costs and the parts of the price basket that do not reverse quickly.

Energy shocks do not disappear cleanly once oil rolls over. Higher fuel costs feed into shipping, insurance, inventory management and operating costs, and those effects tend to linger. Companies rarely rush to hand back margin once a ceasefire hits the tape. By the time crude starts falling, much of the pricing damage has already moved deeper into the system. Until service-sector inflation cools in a convincing way, lower oil looks more like short-term relief than a genuine all-clear in the inflation story.

For the US dollar, that still leaves room to at least consolidate recent gains. The Fed has turned less forgiving. The market is still adjusting to a chair who may say less and ask investors to infer more. The inflation pipeline does not look ready to reflect lower oil prices any time soon. The US consumer has also stayed resilient through the first half of 2026. That is enough to keep the US dollar bid alive.

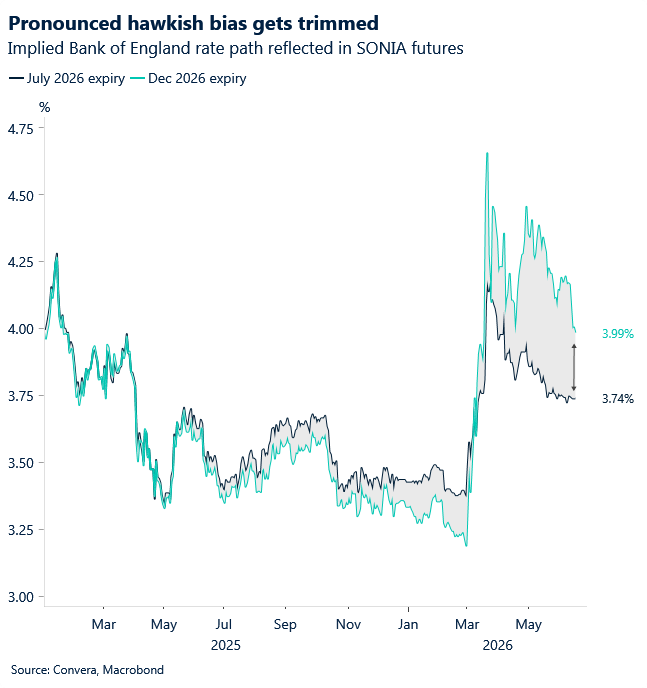

GBP weaker after BoE

The Bank of England left rates unchanged at 3.75% yesterday. The vote split was 7–2, with Megan Greene and Huw Pill voting for a hike, in line with expectations.

Governor Bailey described the decision as an active “hold”, noting that tighter financial conditions have helped contain inflationary pressures. The pound weakened following the decision, while markets pared back some expected tightening in the BoE outlook for the year.

The BoE had seen one of the sharpest hawkish repricings in the G10 since the conflict began in late February, leaving room for a gradual unwind as the labour market continues to show signs of cooling and inflation comes in softer than expected.

Despite maintaining a cautious tone, Governor Andrew Bailey noted that “oil prices have fallen in recent days, and that’s encouraging”. This improving geopolitical backdrop, combined with a softer inflation print this week, has helped markets build confidence that further hikes may be off the table in the near term—particularly against an ECB that has already tightened and a Fed that still sees scope for another hike this year.

Greenback extends post-Fed surge in Asia

The US dollar was stronger in Asia overnight with moves also driven by a weaker yen after this week’s Bank of Japan move to hike rates.

BoJ Deputy Governor Himino doubled down on a tightening bias on Friday and stressed that officials will keep a close eye on FX moves. He said currency swings now feed into inflation more strongly, as firms have become quicker to adjust prices.

Himino added that underlying inflation is closing in on the BoJ’s 2% goal, but warned it could push higher as pricing behaviour continues to shift.

His remarks followed a sharp move in USD/JPY, which jumped to 161.81 a day earlier after firmer Fed signals. In a separate comment, Finance Minister Satsuki Katayama said authorities stand ready to act decisively against speculative FX moves.

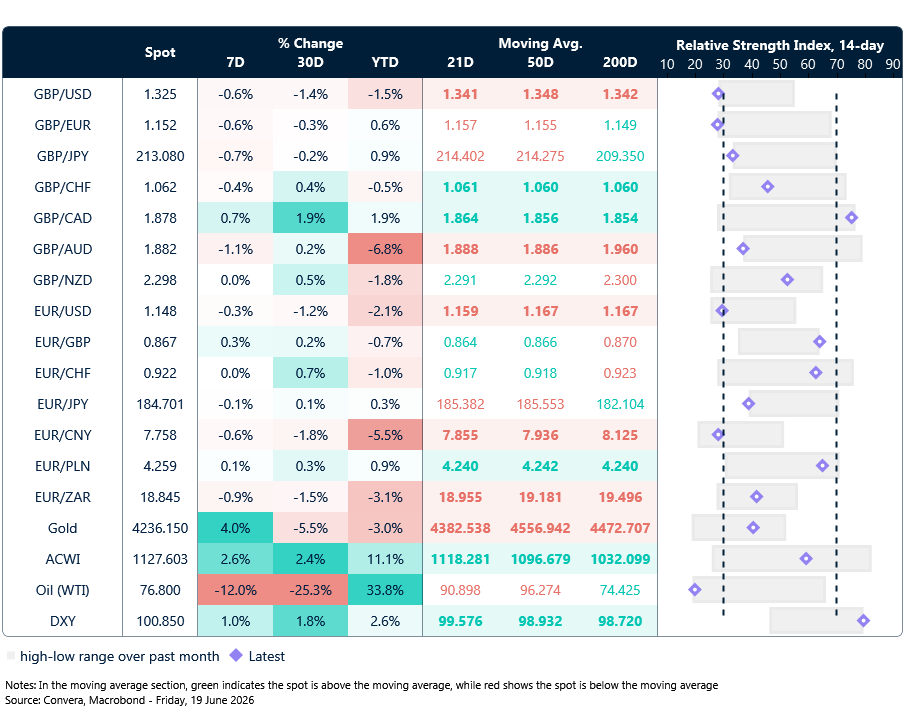

In other markets, USD/SGD increased 0.1%. USD/CNH was flat as yuan outperformance continued.

Greenback extends gains post-Fed

Table: seven-day rolling currency trends and trading ranges

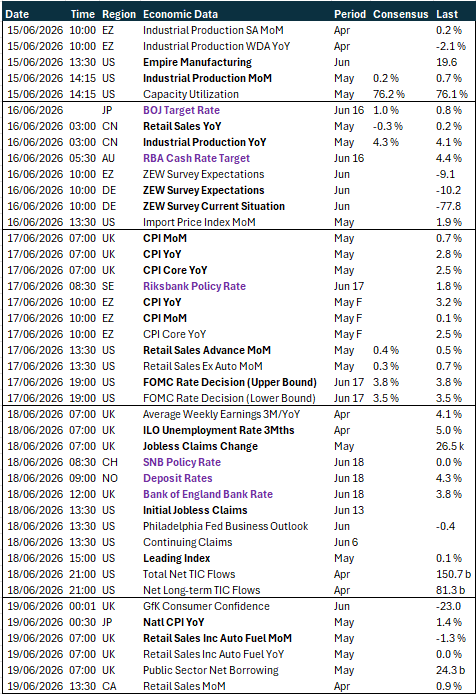

Key global risk events

Calendar: 15 – 19 June

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.