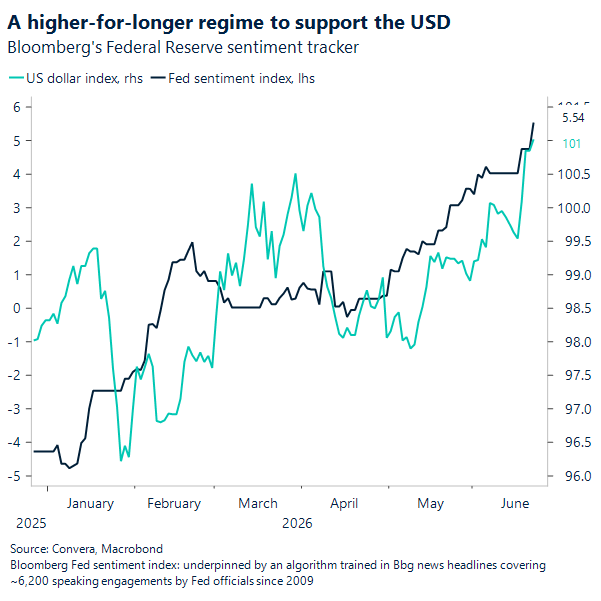

USD: US Dollar breakout puts markets on notice

The US Dollar has finally done what it spent most of the past year threatening to do: push through the top of its range. DXY has cleared the 100.50 ceiling and is trading at a one-year high, helped by a flattening US curve, another leg lower in EUR/USD through 1.14, USD/JPY on upward pressure beyond 161, and a broader risk-off tone. Part of that bid still reflects the Fed’s June pivot, when rates were left at 3.50%–3.75% and the old easing bias was quietly dropped. The market has spent the days since repricing a higher-for-longer path, and the dollar has been one of the clearest expressions of that shift.

Kevin Warsh’s arrival has added another layer. Markets are still leaning on the SEP and the dot plot, yet the new chair has already hinted that the Fed’s communication framework could become less predictable and more conditional. The problem that comes with it, is that thinner guidance usually means a bigger premium for uncertainty, especially at the front end, where two-year yields have shown most of the repricing. The reaffirmation of Fed independence has also helped narrow part of the risk premium that had weighed on the US Dollar earlier this year, giving the greenback another tailwind just as global risk appetite has started to fray.

Still, the move is getting tactically crowded. Oil’s support for the dollar is fading as the US-Iran ceasefire holds and the terms-of-trade boost from higher crude begins to unwind, while bullish dollar positioning and sentiment already look stretched. There is also a case that the best of the US data surprise may be behind us, even if Europe is hardly offering a compelling alternative; softer price signals in recent French and German PMIs, along with a more dovish tone from Lagarde, have only reinforced the rate gap in the dollar’s favour. For now, the breakout is real, but with DXY pressing higher and RSI nearing overbought territory, the next leg will need more than momentum alone.

CAD: Inflation problem is spreading beyond the pump

Canada’s inflation picture turned uglier in May. Headline CPI rose 3.2% from a year earlier, up from 2.8% in April and above the 3.0% consensus. On a monthly basis, prices jumped 1.0%. That pushed inflation back above the Bank of Canada’s 3% upper bound and served as a reminder that the path back to price stability is unlikely to be smooth.

Gasoline was still the main culprit, but the report was not just about the pump. CPI excluding gasoline rose 2.2%, up from 2.0% in April, a sign that the energy shock is beginning to leave a broader imprint. Food, travel and transportation all picked up. That does not yet amount to a generalized inflation problem, though it does suggest the price pressure is no longer as narrowly contained as policymakers would like.

The energy math still matters. Gasoline accounts for only about 4% of the CPI basket, yet it drove roughly 40% of May’s annual inflation rate. Middle East supply fears helped push pump prices 33.2% higher, delivering the biggest jolt to headline inflation. The spillover is now showing up elsewhere. Grocery bills climbed as fresh vegetable prices surged, with tomatoes up sharply on poor weather and US tariffs. Higher jet fuel costs also fed through to airfares, reversing the previous month’s decline.

There were still pockets of relief. Shelter inflation continued to cool, with rent growth easing to 3.5%, the slowest pace since early 2022. Mortgage-interest costs kept decelerating. Core inflation measures also remained near target, which helps explain why this report, while uncomfortable, is unlikely to trigger a policy panic at the Bank of Canada.

That is the balancing act facing policymakers. Inflation is becoming more widespread, yet the economy is soft and the labour market is losing momentum. That leaves little case for a rate hike. A prolonged pause still looks like the more likely path, with officials watching closely to see whether the latest price pressure fades with energy or starts to seep into expectations and wage-setting behaviour.

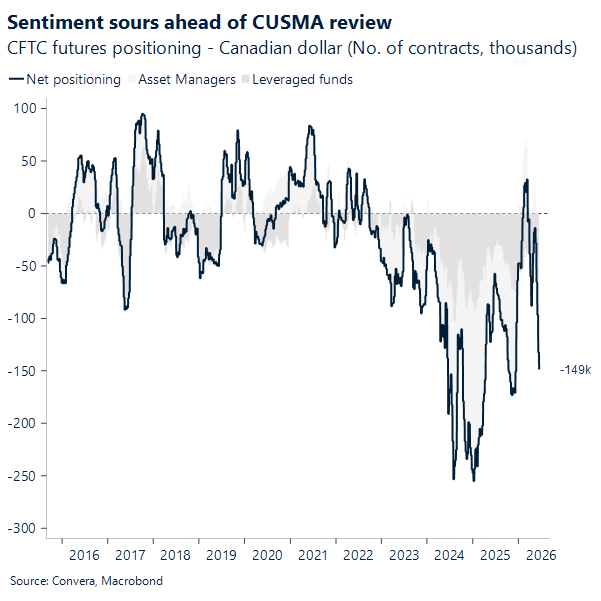

In FX, the USD/CAD has climbed steadily over the past three weeks, rising from around 1.379 to 1.419, a one-year high. That move says less about confidence in Canada’s inflation outlook than it does about the broader macro backdrop. A firmer US dollar, wider yield differentials and persistent trade friction with Washington continue to weigh on the loonie. With the CUSMA deal review drawing closer, investors have found little reason to fight that trend.

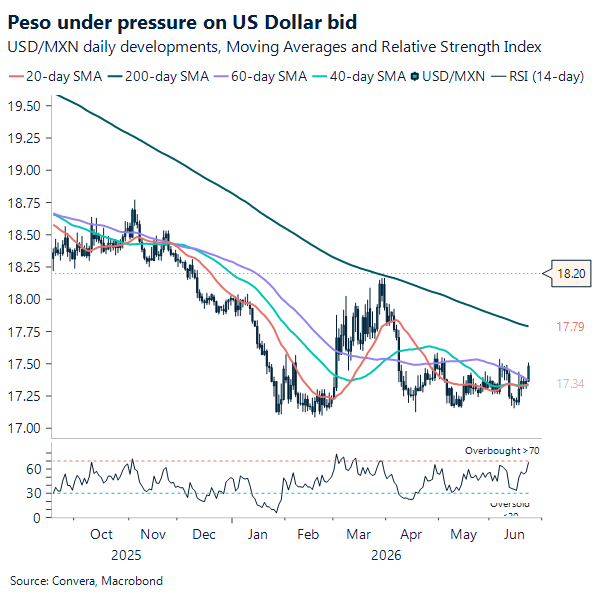

MXN: USD/MXN climbs as policy gaps reopen

USD/MXN is grinding higher, with the dollar’s broader breakout doing most of the work. The pair has climbed back toward 17.48 and is now trading above its 20-, 50- and 100-day moving averages, a sign that near-term momentum has turned more constructive for the dollar even if the longer-term downtrend has not fully rolled over. That fits the wider dollar story: a flatter US curve, a Fed that has revived the higher-for-longer trade, and a market still adjusting to a new Fed era. In that setup, MXN has started to lose some of the carry shine that protected it earlier in the year.

Trade headlines are unlikely to be the main trigger, even as CUSMA deal review move into a key phase. Markets have grown more immune to tariff noise, and investors are treating the talks as background risk rather than a reason to materially reprice the peso. The bigger pressure point sits in monetary policy. If Banxico keeps leaning dovish while the Fed stays hawkish, Mexico’s real-rate advantage starts to look less compelling.

The USD/MXN has regained its short-term footing and is pressing toward the top of its recent range, though it still sits below the 200-day moving average near 17.79, which remains the bigger line in the sand. A strong move through that area would shift the conversation from rebound to trend reversal. Until then, the peso is still under pressure from a stronger US Dollar and a narrowing policy cushion, even if the trade story stays mostly in the background.

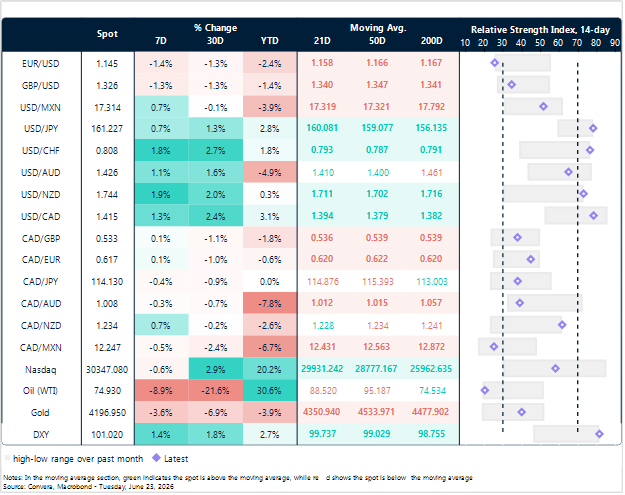

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

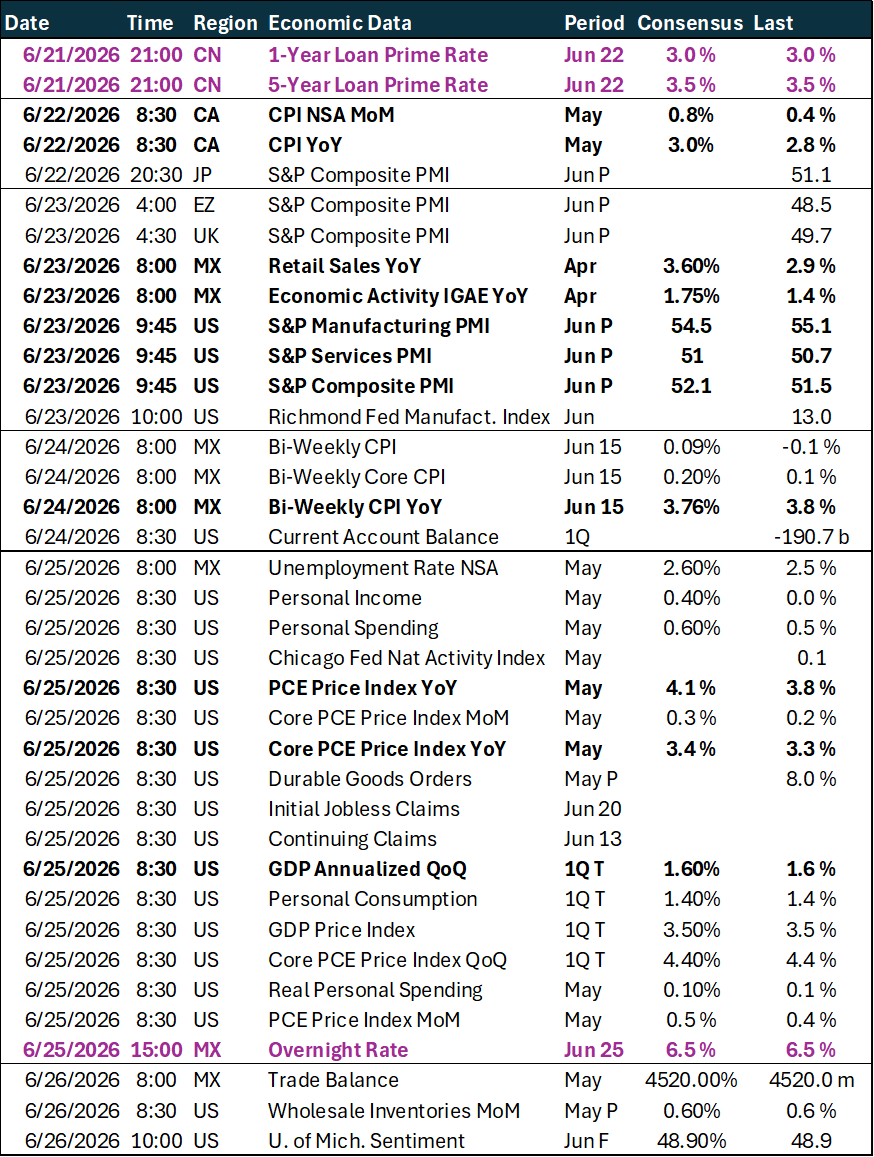

Calendar: June 22-26

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.