Global mood sours

Global markets weakened overnight, with US sharemarkets lower as political protests in Iran continued and oil prices spiked. Crude oil gained 2.6%, reaching its highest level since October.

Meanwhile, the US domestic scene fretted over President Trump’s warning about adding caps to credit card interest charges and ongoing concerns about the prosecution of Federal Reserve Chair Jerome Powell.

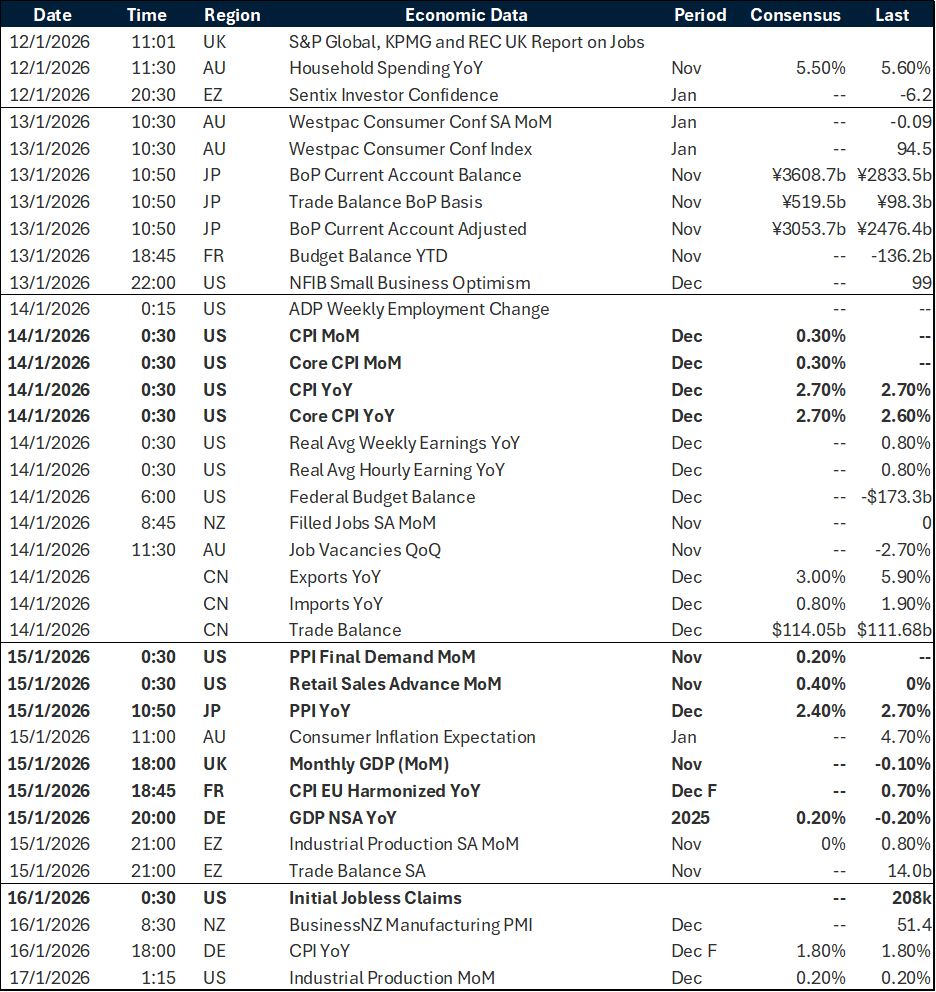

Also, US inflation numbers were broadly in line with expectations, making rate cuts less likely.

The US dollar strengthened as sentiment soured globally, with the USD index closing at its highest level since 12 December.

Gains were most notable in Asia, where USD/JPY surged 0.6% to its highest level since July 2024.

USD/SGD rose 0.2%, while USD/CNH added 0.1%.

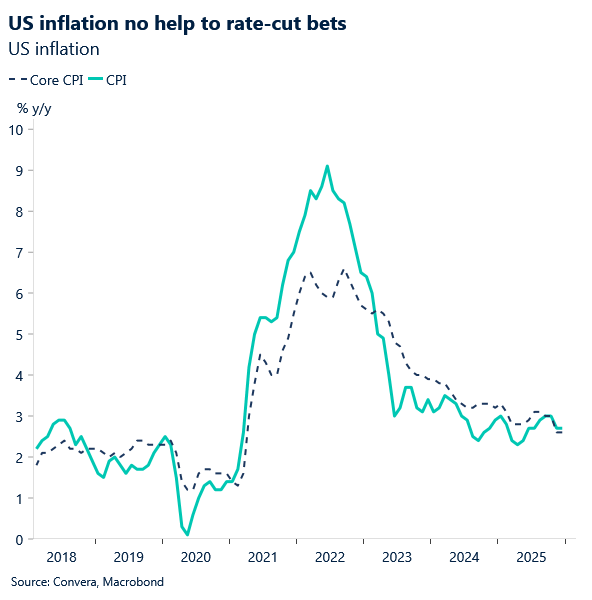

Aussie at two-week lows amid shaky confidence

AUD/USD fell 0.4%, with the pair falling back to two-week lows.

Australia’s consumer mood stumbled into the new year, with two surveys painting a cautious picture.

The Westpac–Melbourne Institute index slipped 1.7% to 92.9 in January, reflecting sharper pessimism about family finances (down 4.5%) and the economy (down 6.5%). Expectations for mortgage rates in 2026 climbed, with about two-thirds of households bracing for increases, while job confidence softened.

The ANZ Roy Morgan gauge for Jan. 6–12 rose three points to 84.5, helped by stronger appetite for major household purchases and less negative views on the economy over one and five years.

Despite those pockets of resilience, the surveys show the weakest new year start since 1991.

Markets see an 87% chance of a rate hike in June 2026. AUD/USD eased from near the top of its six-month range, as shown in the chart.

Key support sits at the 21-day EMA of 0.6682, followed by the 50-day EMA of 0.6633.

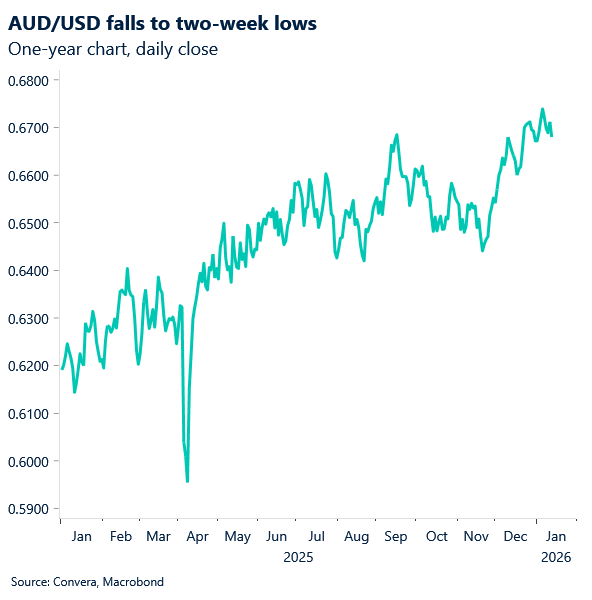

Kiwi dollar boosted by upbeat business mood, but falls later

Across the Tasman, sentiment shifted in the opposite direction. New Zealand’s business confidence surged at the end of 2025, even as real activity struggled to keep pace.

The NZIER Q4 survey showed a net 39% of firms expecting better economic conditions — the strongest reading since 2014 and up from 17% in the prior quarter.

Optimism spread across sectors, with manufacturing swinging from the least to the most upbeat. Construction stayed weak, weighed down by soft demand and falling prices. Hiring and investment plans turned positive, with early signs of skilled labour shortages emerging.

Markets see a potential rate hike in October 2026.

NZD/USD was initially higher in Tuesday’s trade but fell later in line with global moves.

USD higher after CPI

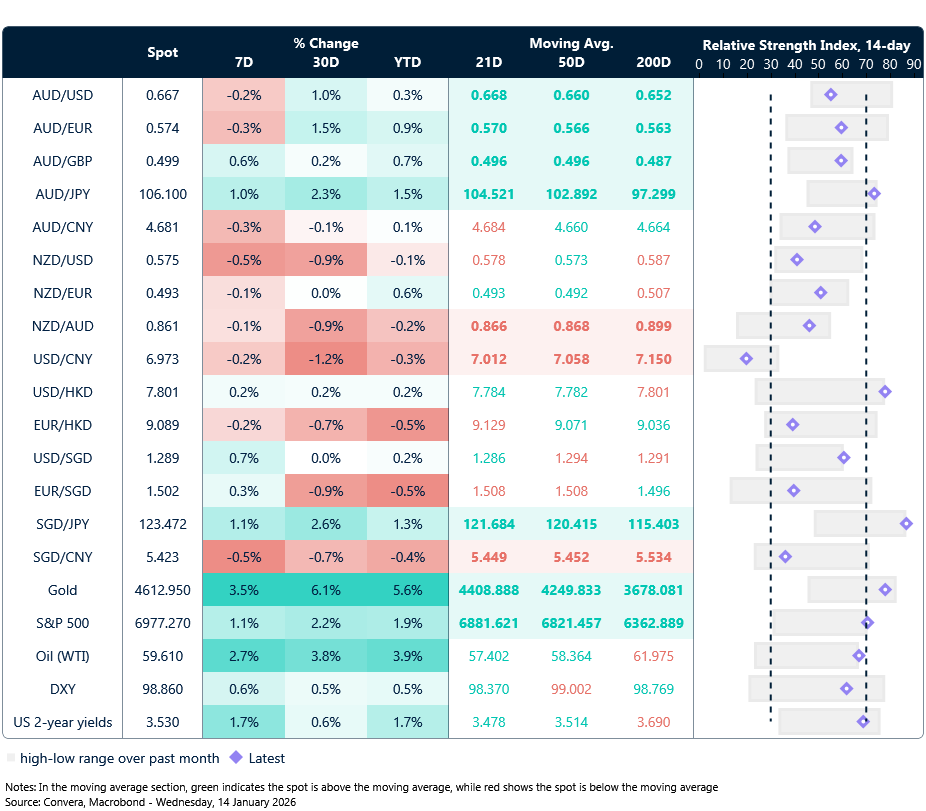

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 12 – 16 Jan