Written by Convera’s Market Insights team

Failed auction, hawkish Powell and a cyberattack

Boris Kovacevic – Global Macro Strategist

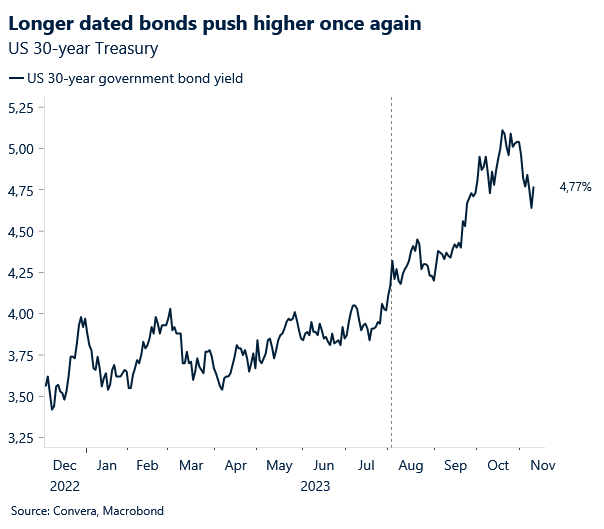

The setup for risk assets going into this week was too good to be true. Last week’s disappointing macro data and the Federal Reserve’s interest rate pause had convinced markets that the majority of the pain had already passed. The S&P 500 had been on track to record its ninth consecutive daily rise with government bond yields continuing to fall against the backdrop of last week’s developments. However, a perfect storm involving a hawkish speech from Jerome Powell, a failed 30-year Treasury auction and a cyberattack of the world’s largest bank have shown investors that uncertainties continue to shape the market environment.

Global equities broadly declined with the MSCI world index dropping by more than 1% intra-day. US 10-year yields pushed higher again after falling to the lowest level in six weeks at 4.38%. The first wave of the sell-off was caused by the poor 30-year government bond auction with the Treasury having to effectively give a 5-basis point concession to markets to shift the debt. Liquidity in the world’s largest financial market has slowly but surely started to deteriorate in recent months with the Bloomberg Treasury market liquidity index rising well above its pre-pandemic levels. The terrible auction was followed by a hawkish speech by Fed Chair Jerome Powell, who refused to close the door on a potential rate increase in the future. His speech pushed the expectations of another hike by the Fed slightly higher across the board. However, the probabilities for January and March still stand at below 25%.

The last shock wave of the day came from China, where the largest bank in the world, the Industrial & Commercial Bank of China Ltd., had been hit by a cyberattack, rendering it unable to process trades of US Treasuries. The attack caused disruptions in the market, as brokerages and banks were forced to reroute trade. It is unclear how much the Treasury market had been affected by the incident as it followed the volatility caused by Powell and the failed auction. However, it does highlight the potential risks financial markets face from such digital attacks. The US Dollar has made up more than half of its losses from last week and as we said previously, investors are finding it hard to let go of the currency in such uncertain and volatile times. The Michigan Consumer Confidence Index will be the last release in the US before the weekend.

UK economy defies contraction expectations

George Vessey – Lead FX Strategist

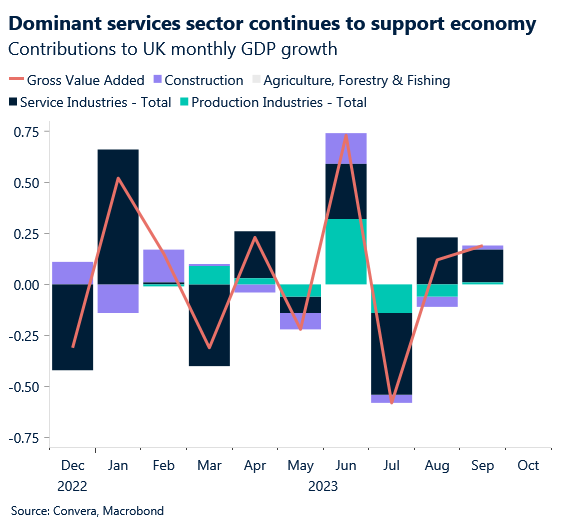

The UK economy flatlined in the third quarter as a whole, defying expectations for a contraction. For September, GDP grew 0.2% m/m, also better than the zero growth forecast by economists and follows growth of 0.1% in August, revised down from growth of 0.2%. Overall, this means the UK could avoid a recession this year, but the pound has barely reacted.

The services sector was the main contributor to the 0.2% growth in GDP in September, but the third quarter readings overall showed services output fell by 0.1%, production output showed no growth, and construction grew by 0.1%. Although better than expectations overall, today’s data batch is far from cheery as the zero growth recorded in Q3 is the UK’s worst quarterly performance in a year. Stagnation fears remain elevated for 2024 as the lagged effects of monetary tightening continue to feed through to the real economy. This evidence may also help to convince the Bank of England that no more interest rate hikes are needed to tame inflation, whilst markets continue to price in the first rate cut from August next year. The British pound has erased over half of last week’s gains against the US dollar, failing to close above key long-term daily and weekly moving averages. The currency pair has declined for four days straight and is now about 1.5% higher than its 9-month low recorded at the start of last month, though it hasn’t dipped back into the descending trend channel yet.

GBP/EUR, meanwhile, has also erased all of last week’s gains and more. The euro usually outperforms in December, likely helped by the fact that we see more positive European data surprises this time of year relative to the UK. Therefore, we eye €1.1440 as the next key support, which if broken decisively, could open the door to a new lower trading range between €1.11 and €1.14.

Weak Chinese data renews stimulus hopes

Ruta Prieskienyte – FX Strategist

Europe was in an upbeat mood on Thursday with all the major European stocks up on the day. STOXX climbed to a fresh 7-week high and oil prices rebounded. The euro held ground above $1.07 for most of the day, until Fed Chair Powell’s pushback against speculations that US interest rates already peaked, sending EUR/USD down by 0.4% and towards $1.065. Meanwhile, the latest inflation data from China could make markets more cautious about China’s growth recovery, but it also fuels hope for additional policy support.

China resumed consumer price deflation in October with the headline CPI index falling into a negative territory of -0.2% y/y due to a slump in pork prices. Combined with the weak PPI reading, this indicates persistently weak demand in the world’s largest economy. While weak data could weigh down on the global growth via the trade channel, it also supports the case for more domestic stimulus. Low inflation has been one of the main reasons cited by economists who argue that China’s economy is growing below its potential and needs more monetary and fiscal stimulus. Beijing has stepped up monetary and fiscal easing in recent months, such as cutting interest rates and the amount of cash banks must keep in reserve, as well as issuing additional sovereign bonds in order to meet its 5.3% GDP target for 2023. Renewed hopes for further stimulus would revive risk appetite and help risk prone currencies such as the Australian dollar and the euro.

EUR/USD is on track to close the week lower, but markets will be keeping a close eye on Christine Lagarde’s interview later today for any comments on the ECB’s future monetary policy path. The president of the ECB is likely to echo her colleagues’ hawkish remarks by pushing back against rate cute expectations. While it is unlikely to cause a material repricing of interest rate expectations, given the mounting evidence of an economic slowdown, it could support the upward momentum enjoyed by the euro since the beginning of October.

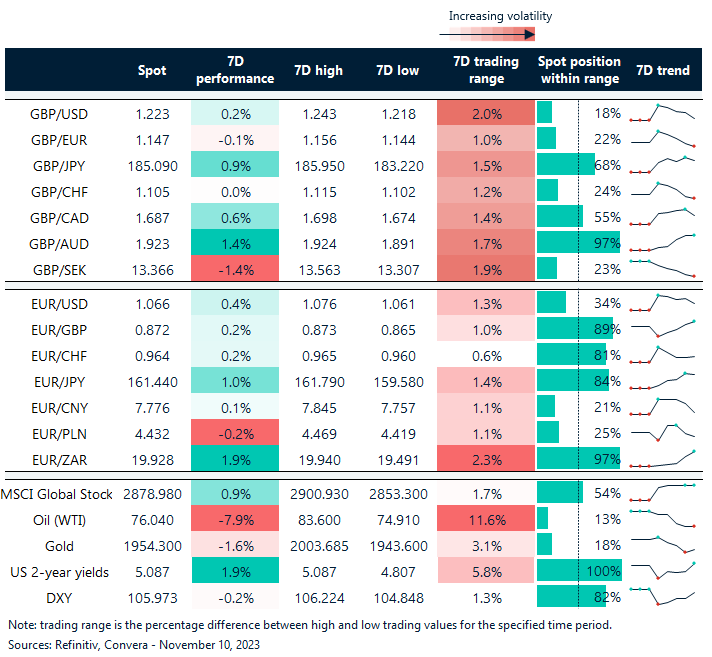

GBP & EUR almost flat compared to last Friday

Table: 7-day currency trends and trading ranges

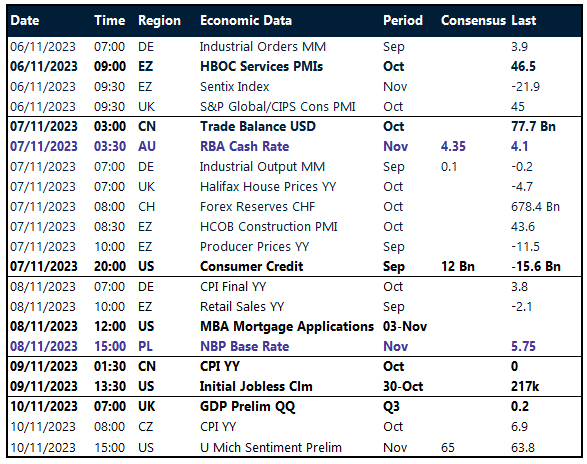

Key global risk events

Calendar: November 06-10

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.