US policy: Trade friction far from over

With the State of the Union address just a day away, the administration is responding to the Supreme Court 6 – 3 decision that struck down its emergency trade powers under IEEPA. The President has called the ruling a disgrace, but the White House has already pivoted to its backup plan. Starting this Tuesday, the administration will implement a global blanket tariff of 15% using Section 122 authority. The Court made it clear that IEEPA does not authorize any tariffs, reinforcing that the power to tax belongs to Congress. But before the first “My fellow Americans” is even uttered ahead of this Tuesday, the executive branch has shown, as it was largely expected, it will find other avenues to keep its trade agenda alive.

While the ruling effectively dismantles the emergency levies tied to fentanyl and border security, it leaves a significant portion of the protectionist landscape untouched. Sectoral tariffs built on older, more specific statutes remain firmly in place because they were not the focus of this legal challenge. Specifically, the 25% to 50% duties on steel and aluminum under Section 232 continue to squeeze global metal markets, and the longstanding Section 301 tariffs on Chinese electronics and technology remain as a barrier. Additionally, significant duties on softwood lumber and certain automobile parts are still active, as these rely on national security or anti subsidy findings rather than the broad emergency powers that the Court struck down last Friday.

The shift to this new 15% blanket rate creates a mixed landscape. According to Global Trade Alert, countries singled out for criticism are actually seeing their average tariff rates drop. Brazil gets a massive 13.6% reduction, and China sees a 7.1% drop. Meanwhile, traditional allies like the European Union, the UK, and Japan are bracing for the biggest hit as they move from historically lower rates straight into the 15% line of fire. US Trade Representative Jamieson Greer has defended the move, stating that the urgency of the situation demanded the jump from 10% to 15%.

For Canada, the situation offers a mix of relief and new challenges. The new Section 122 tariffs will not apply to CUSMA compliant Canadian goods. The small share of non-compliant goods previously faced a 35% levy under the now invalidated IEEPA regime. However, the ruling means the President can no longer use a magic tariff pen to threaten partners on a whim. While the immediate threat of universal fentanyl tariffs is gone, there is a growing sense that losing this broad emergency shortcut might make the administration more desperate to use the upcoming CUSMA review to exert maximum pressure on Canada.

The long-term danger for Canada and other trading partners is adapting to this new, more disciplined but equally aggressive trade reality. The President has promised to launch new Section 301 investigations to sustain these tariffs beyond the immediate horizon, bringing a rigid structure to future trade battles. Importantly, these new Section 122 tariffs are limited to 150 days before they require Congressional approval, setting the stage for a massive legislative showdown. Furthermore, the issue of tariff refunds from the previous IEEPA era will now be heavily litigated in lower courts.

US macro: Growth stays solid, but inflation fears return

Aside from more trade drama, there’s a whole lot going on in the macro front. Last Friday, the Q4 advanced GDP report came out, and it was a sobering reading for many. The US economy experienced a significant deceleration during the final stretch of 2025, with Q4 GDP increasing at an annualized rate of 1.4%. This figure represents a sharp moderation from the 4.4% expansion recorded in the third quarter and fell short of all economist forecasts in recent surveys. A primary driver of this slowdown was a record-long government shutdown that occupied nearly half of the three-month period, which the Bureau of Economic Analysis estimates stripped approximately 1% point from the quarterly GDP. Despite this weak quarterly finish, the broader picture for 2025 remained resilient, as the economy expanded 2.2% over the full year, overcoming a difficult first quarter marked by a massive surge in pre-tariff imports.

The mid-year recovery that bolstered the annual figures was largely attributed to a shift in trade and monetary policy. As the US administration backpedaled on its reciprocal tariffs announcements and the Federal Reserve starting cutting rates, the stock market climbed to record highs, providing the financial cushion for wealthier Americans to maintain their spending levels. Also, factory activity only began to show signs of life toward the end of the year after a long period of stagnation, and the inflation rate remained a persistent challenge, keeping the issue of affordability at the forefront of the national conversation heading into the midterm elections.

Inflation data released alongside the GDP figures confirmed that price pressures remain stubborn. The core personal consumption expenditures price index, which is the Federal Reserve’s preferred gauge for underlying inflation, rose 0.4% in December alone. This monthly increase was the largest in nearly a year and pushed the annual core PCE, which excludes volatile food and energy costs, to 3%, up from the 2.8% level seen at the start of 2025. This upward trend suggests that despite the overall moderation in growth, the path toward the Fed’s long-term targets is becoming increasingly non-linear and more gradual than market participants had initially anticipated.

This combination of shutdown-impacted growth and rising core inflation creates a difficult environment for future monetary policy. The persistent nature of price increases, paired with a labor market and consumer base that have shown historical resilience, may force the Federal Reserve to maintain restrictive interest rates for a longer duration.

What does this all mean for the US Dollar?

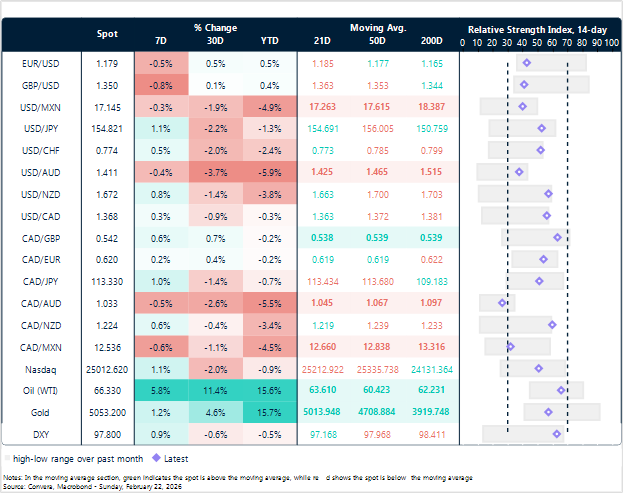

Since last Friday, the US DXY Dollar Index has moved from close to 98.1 to 97.3, dropping around 0.5% in early Asian session. It’s a complex landscape for the Dollar, where hawkish monetary signals and trade policy shifts create opposing pressures. On one hand, last week’s macro data provided a strong case for a resilient greenback after a hotter than expected Core PCE reading of 3% showed that underlying price pressures remain sticky. This inflationary signal was reinforced by surprisingly hawkish Fed minutes which suggested that officials are increasingly wary of cutting rates too quickly. Such macro landscape typically provides a solid floor for the currency as yields climb and investors price out near-term easing.

However, these macro tailwinds will be challenged short-term by a cloud of trade uncertainty that has forced a repricing of the dollar’s path. While the US Dollar DXY index touched 98.1 on Friday, it has since retreated toward 97.3 as markets digest the administration’s pivot toward using new statutory tools for levies. This transition suggests that any immediate relief from lower charges is being overshadowed by the unpredictability of future trade barriers, which dampens the strong dollar narrative. Consequently, while the Fed’s cautious stance on inflation provides a theoretical lift, the lack of clarity on the trade front is likely to remain the dominant weight on the dollar until the political dust settles.

What’s coming up this week?

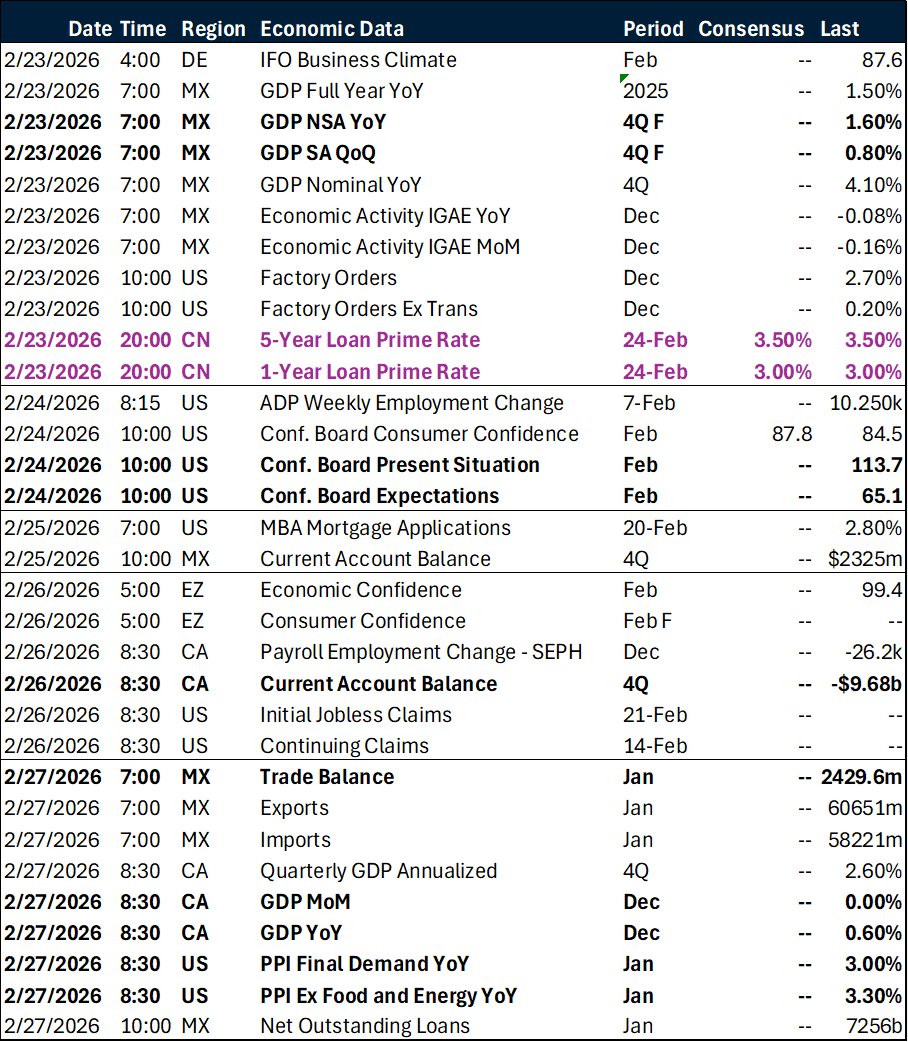

President Trump delivers the State of the Union address (Tue) where he’s expected to discuss policy priorities like tariffs and affordability ahead of the November midterms. Markets will pay special attention to Nvidia earnings (Wed) and the Apple annual general meeting (Tue) while US data releases cover factory orders (Mon), consumer confidence (Tue), and producer price index (Fri). It’s a busy week that balances political rhetoric with major corporate updates and a heavy Fedspeak speaking schedule.

Global focus shifts to inflation readings from Australia (Wed), Tokyo (Fri), and regional Europe (Fri) to gauge broader price trends. Central bank events include remarks from ECB President Lagarde (Mon) and interest rate decisions in Hungary (Tue) and South Korea (Thu). The busy calendar concludes with GDP figures from Mexico (Mon), India (Fri), and Canada (Fri).

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: February 23 – 27

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.