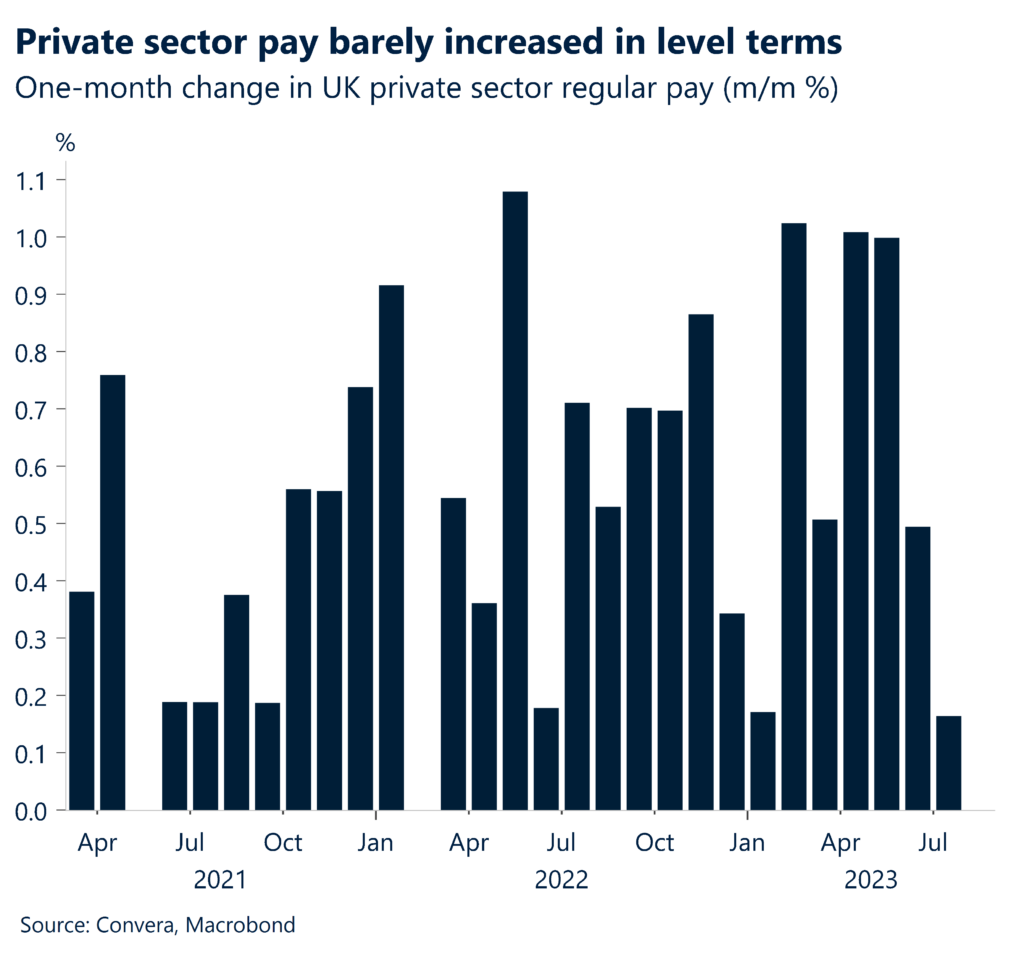

Although UK wage growth remains elevated at a headline level, if you strip out the public sector, private sector pay barely increased in level terms between June and July. Moreover, there are various signals that the labour market is cooling more noticeably. UK inflation data is due next Wednesday before the BoE meeting on Thursday. We believe the BoE will still hike by 25 basis points in Sep, though markets are currently pricing an 80% chance, and a 50/50 chance of another hike in Nov compared to two full hikes previously priced in only a few weeks back.

Labour market weakening

- The UK unemployment rate ticked up to 4.3% in the three months to July from 4.2% a month earlier, its highest since the three months to September 2021.

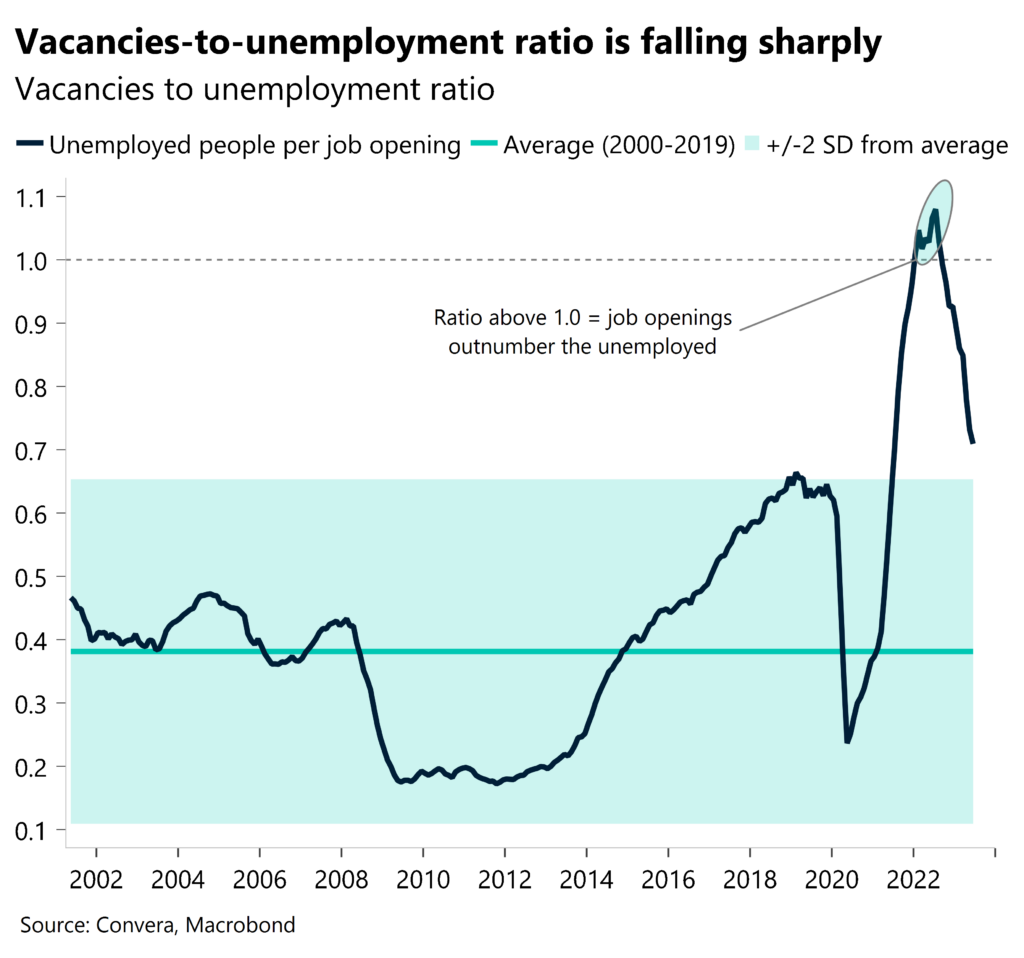

- The ratio of unfilled job openings to the number of unemployed workers, a ratio that BoE Governor Bailey has consistently referenced, is falling quickly now and will more-than-likely be back to pre-Covid levels within the next couple of months.

- The number of people inactive (neither employed nor actively seeking a job) has begun to inch higher again though, driven by long-term sickness and a renewed rise in student numbers. This won’t please BoE officials.

Wages catch up to inflation

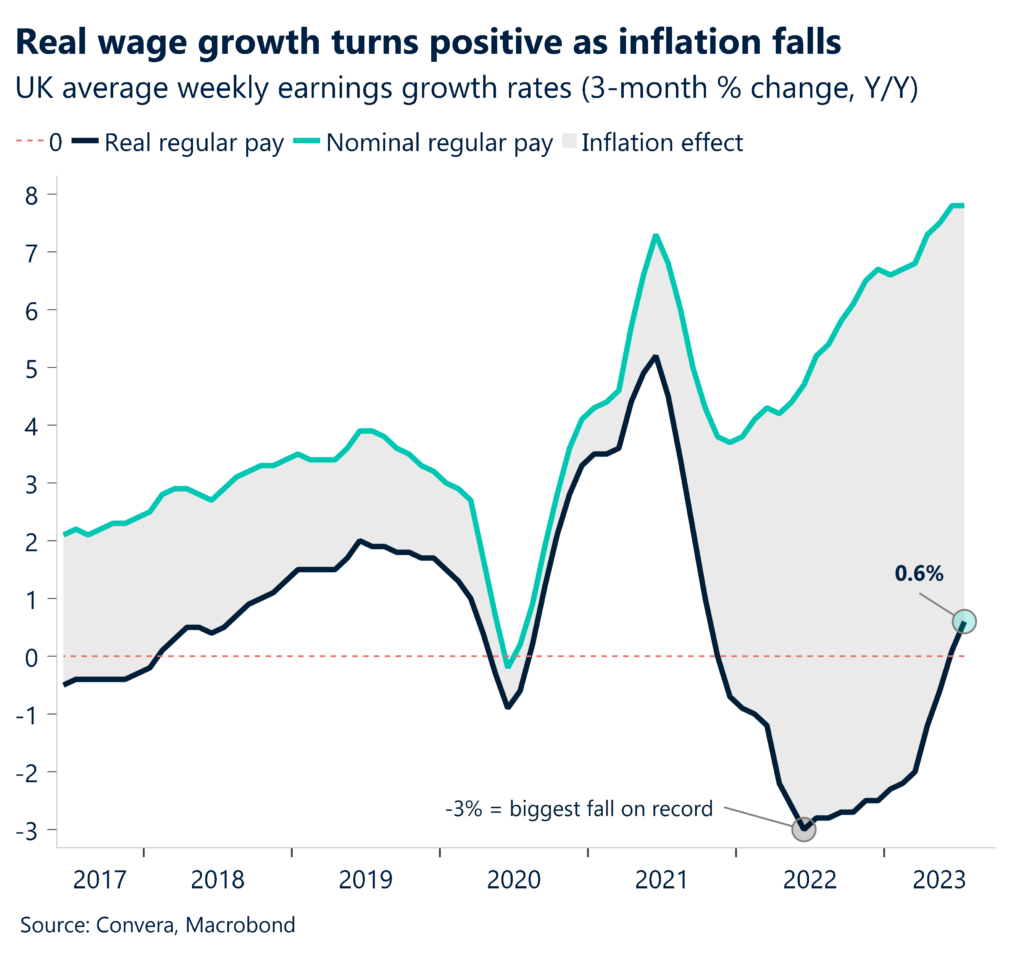

- Wage growth remains a concern for the BoE. Regular pay, excluding bonuses, were 7.8% higher than a year ago in the three months through July, the highest rate since comparable records began in 2001. This means average wage growth is now growing faster than consumer prices.

- But drill down and if you strip out the public sector, private sector pay barely increased in level terms between June and July.

- Still, absent any meaningful weakening of wage growth, the BoE will remain concerned that this will keep core and services inflation sticky and therefore interest rates will have to remain higher for longer.

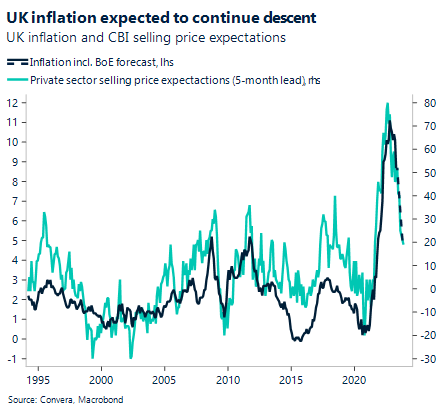

Inflation expectations are key

- Higher inflation expectations among consumers/businesses explain most of the previous rise in wage growth, and by that logic you’d expect pay pressures to abate a fair bit from here on, as consumers and businesses are no longer expecting such aggressive price rises over the coming months.

- The bottom line is that with the jobs market cooling and wage growth, for now at least, not coming in as hot, the labour market data does not scream a need for the Bank to keep hiking rates much further.

Pound at risk

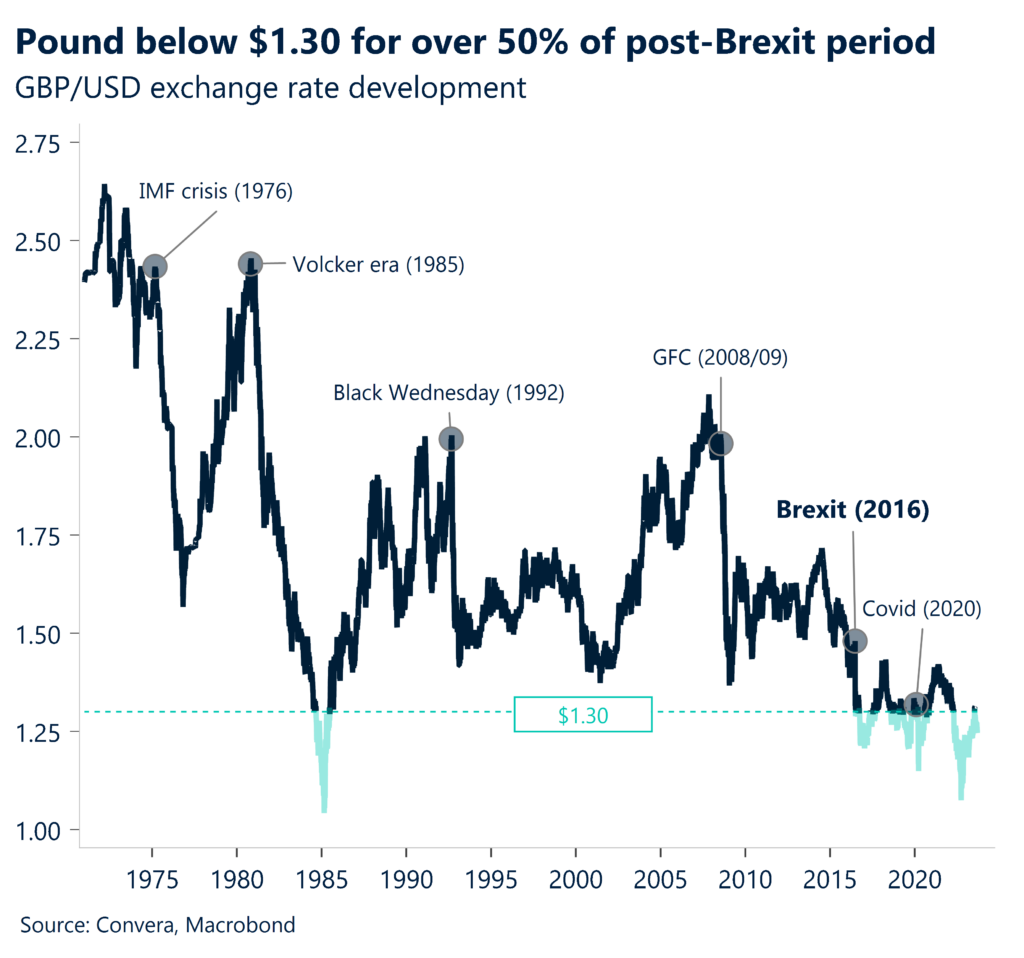

- The British pound has been the best performing major currency for over 60% of this year, buttressed by surging interest rate expectations and the (so far) avoidance of a UK recession.

- Chief among risks for the pound is the lagged effects of higher interest rates. The quandary of UK homeowners, many of whom face massive and potentially unaffordable increases in mortgage costs when fixed contracts come to an end could prompt a housing market recession.

- This could have severe consequences for an economy where big gains in home equity have often heavily influenced consumer trends.

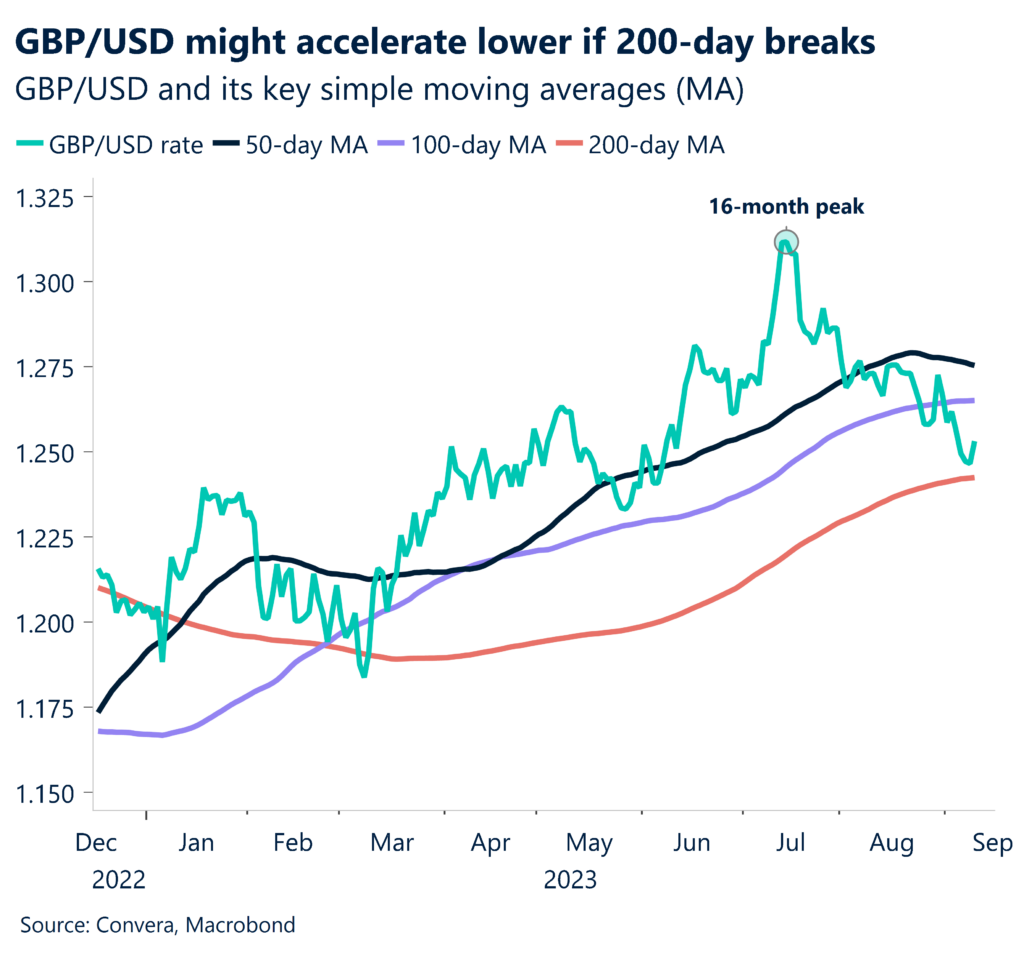

- We’ve already seen GBP/USD fall nearly 5% from its July top of $1.31ish. A meaningful break below its 200-day moving average could open the door to $1.23.

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.