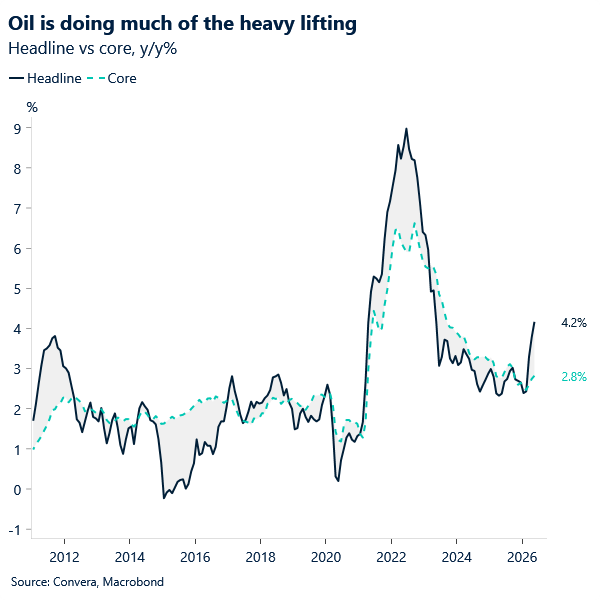

USD: CPI in line, hawkish bias intact, but Warsh test incoming

US headline inflation accelerated to 4.2% in May, up from 3.8%, marking the largest increase in over three years. The print was broadly in line with expectations, although the core monthly figure surprised to the downside at 0.2% against a 0.3% estimate, easing from 0.4% previously. Recent private spending data pointing to softer consumer demand lends further support to the more benign core reading. Treasuries pared earlier losses, while the dollar remained relatively subdued. Given the hawkish momentum that had been building in recent weeks, markets had likely positioned for a firmer outcome, one that would signal broader price pressures rather than predominantly supply-driven dynamics.

On the geopolitical front, the relatively muted upside in oil following the latest exchange of strikes between the US and Iran suggests that investors may be placing greater weight on rhetoric than on the incidents themselves. Efforts by the US administration to frame recent attacks as defensive and temporary in nature may be preventing a more pronounced deterioration in risk sentiment. Equally, there is a high degree of uncertainty around the peace outlook, given the constant back-and-forth on progress toward a more durable resolution, which is limiting markets’ ability to price in further risk-off momentum.

With limited data ahead that could meaningfully reverse recent Fed hawkish repricing, and the ongoing stalemate around Hormuz, the dollar heads into next week’s policy meeting with underlying support. That said, the key test for a more forceful push through the 100 resistance line will be Kevin Warsh’s press conference. Markets are likely to scrutinize both his tone and language closely, amid concerns that he may lean toward political pressure for lower rates.

EUR: Insurance hike, limited lift

EUR/USD edged higher yesterday following a relatively tame US inflation report before pairing back gains on renewed tensions between the US and Iran. The ongoing impasse around Hormuz, combined with a still-resilient hawkish repricing narrative supporting the dollar, continues to cap attempts at a more forceful move back toward the 1.16 handle.

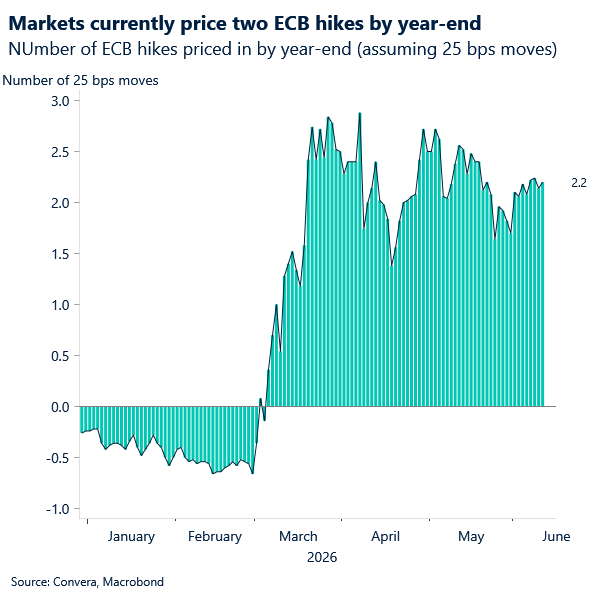

Focus now turns to today’s ECB policy meeting, with markets expecting a rate hike. The move is largely viewed as an insurance step, aimed at signalling readiness in an environment where accelerating inflation dovetails with a deteriorating macro backdrop that could, over time, justify a more accommodative bias. In response, we expect forward guidance to emphasize a data-dependent, meeting-by-meeting approach, with markets likely to place greater weight on updates to the ECB’s staff projections. These may highlight a more pronounced two-sided risk profile, with risks skewed toward higher inflation and weaker growth. Absent a discernible shift toward the inflation side, the event is unlikely to offer meaningful support to the euro.

GBP: Testing key levels to topside

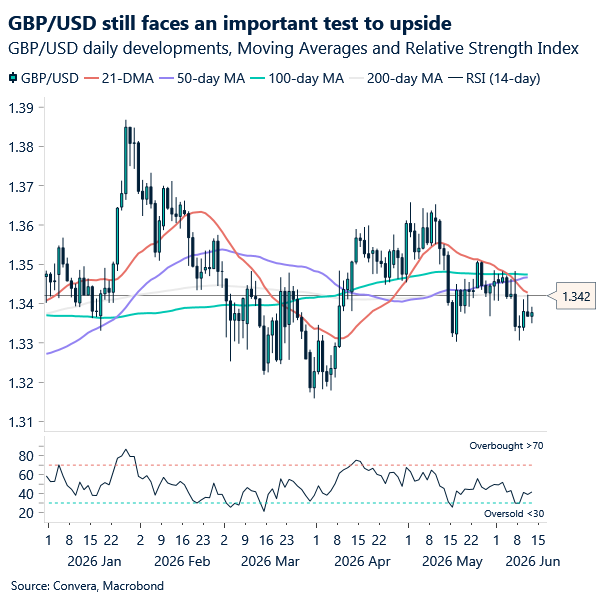

Sterling has remained relatively resilient this week despite an uncertain geopolitical backdrop, softer equity markets and renewed US dollar strength of late. GBP/USD has managed to hold in the high‑1.33s and even climbed following the US inflation release. While the data reinforced expectations for Fed tightening, the market reaction was more nuanced. The dollar softened against parts of the G10 basket immediately afterwards, suggesting much of the hawkish repricing was already embedded.

Technically, GBP/USD still faces an important test near the 200‑day moving average around 1.3420. A sustained break higher likely requires either softer US macro data or a more convincing de-escalation trend in the Middle East.

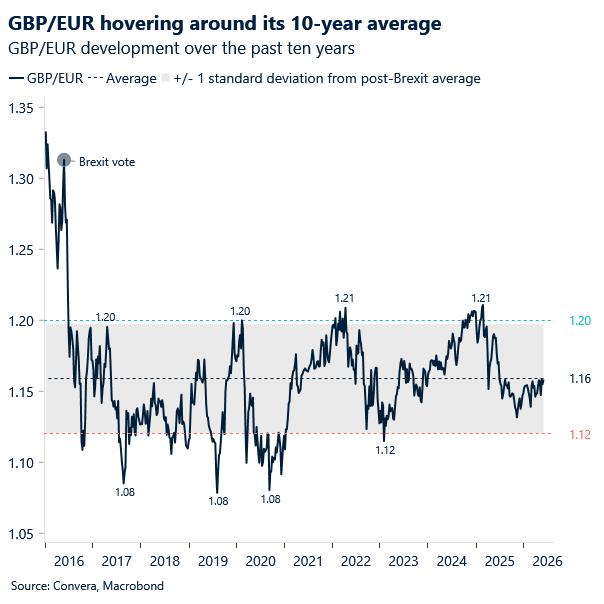

Against the euro, sterling continues to look structurally firmer. GBP/EUR is once again flirting with the 1.16 area, a level that has repeatedly capped upside this year and also coincides with the pair’s long‑term post‑Brexit average. Technically, momentum remains constructive above key moving averages, though the ECB meeting on Thursday now becomes critical. Any pushback against further rate hike expectations could finally allow GBP/EUR to establish a sustained break above 1.16. Conversely, even a modestly hawkish ECB tone could trigger another familiar rejection from that ceiling.

Sterling’s resilience also reflects positioning and relative carry support. Short GBP positioning remains somewhat crowded, while UK yields continue to offer an attractive pickup relative to several G10 peers. That said, we think it’s primarily supported because external conditions have not deteriorated enough to expose the UK’s softer macro and political backdrop more fully.

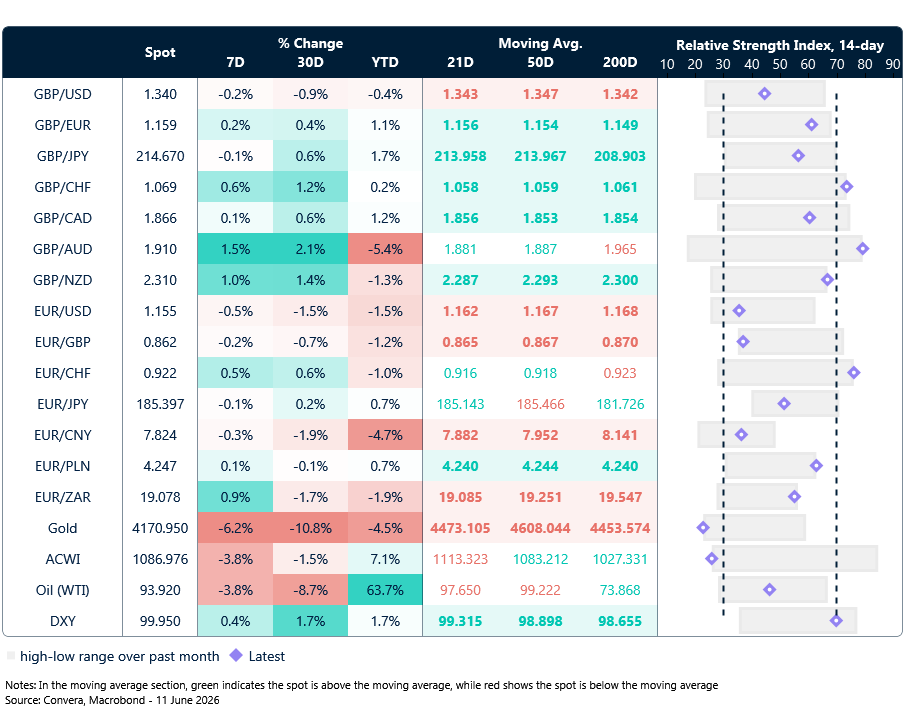

Market snapshot

Table: Currency trends, trading ranges & technical indicators

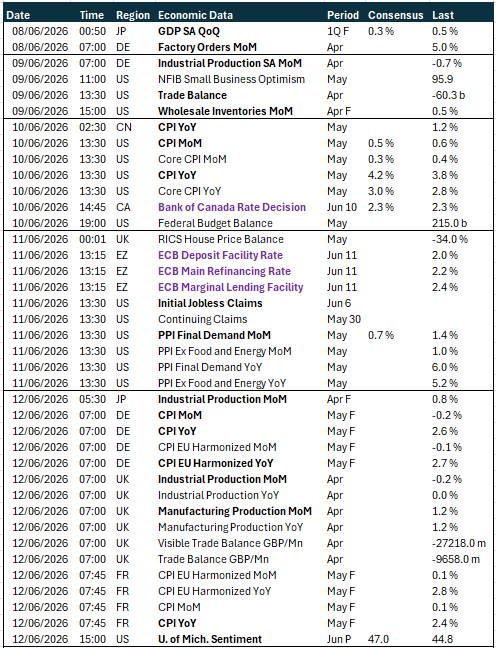

Key global risk events

Calendar: June 8-12

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.