GBP: Sterling firms as Starmer steps down

Sterling enters the tenth anniversary of the Brexit referendum against a backdrop of yet more political drama. While markets had largely anticipated Keir Starmer’s resignation, the initial reaction was nevertheless somewhat surprising. Rather than demanding a higher political risk premium, investors appeared reassured by signs that the transition of power could prove swift and orderly. The pound climbed across the board.

A key factor was former Health Secretary Wes Streeting – previously viewed as a potential leadership contender – throwing his support behind Andy Burnham, reinforcing expectations that Burnham’s path to Downing Street will be largely uncontested. UK gilt yields moved lower in response, and sterling strengthened against all its major peers, clocking its strongest daily gain in over a month versus the euro.

The immediate focus is on the succession process. Starmer will remain in office during the transition, with nominations for a successor opening on 9 July and any leadership contest concluding by 1 September. While markets are currently embracing the prospect of a smooth handover, we should not forget that Burnham has previously unsettled investors with comments perceived as challenging fiscal orthodoxy and the UK’s fiscal rules. As such, the decline in UK political risk premia may prove temporary should concerns reemerge around the fiscal trajectory of a future Burnham government.

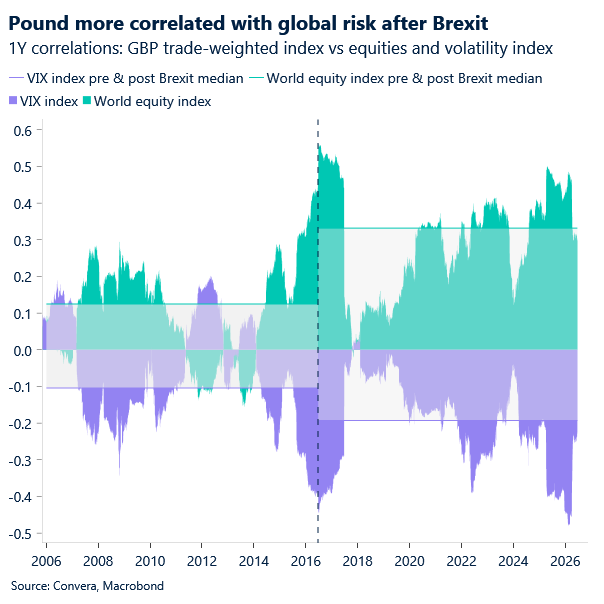

The timing of Starmer’s departure is also particularly notable, coinciding with the tenth anniversary of the Brexit referendum. This serves as a reminder of how deeply Brexit reshaped both UK politics and the broader globalisation cycle. The referendum represented a watershed moment that accelerated political fragmentation, polarisation and electoral volatility, with Starmer becoming the sixth prime minister to exit since the UK voted to leave the EU in June 2016. A decade on, the search for a stable post-Brexit political and economic identity remains unfinished.

For sterling, Brexit did not break the pound, but it fundamentally reclassified it. The currency now trades from a lower structural base, exhibits greater sensitivity to global risk sentiment and commands a higher hedging premium than before the referendum. GBP/EUR averaged 1.27 in the decade before Brexit versus 1.16 since, while GBP/USD has fallen from an average near 1.60 to around 1.30. The challenge for investors is no longer whether Brexit will weaken sterling further, but recognising that it is now a more volatile, risk-sensitive currency whose behaviour reflects the lasting structural consequences of that historic vote.

USD: Hawkish Fed bodes well for dollar

The US dollar remains on a strong footing, with the dollar index up more than 2% month-to-date and on track for its second-best monthly performance in a year. While headlines from the Middle East continue to generate ambiguity, financial markets have become increasingly desensitized to the ebb and flow of geopolitical developments. Still, the conflict remains a key macro driver and risk mood is far from upbeat this week, with equities selling off globally.

The reopening of the Strait of Hormuz and last week’s memorandum of understanding have improved the near-term outlook, but repeated setbacks over recent months have left investors reluctant to fully price a lasting resolution. Much of the optimism surrounding a potential deal had arguably already been reflected in asset prices and the sell-off in tech and AI-linked stocks is likely a blunt reminder of impact of hawkish Fed policy.

Indeed, the US dollar’s recent strength has been driven primarily by macro and policy dynamics. The latest Fed meeting reinforced a hawkish narrative, with Chair Warsh emphasising price stability and maintaining a distinctly data-dependent approach. Markets will have to become comfortable with a Fed that communicates less and that matters because recent data continue to point towards a resilient US economy. Strong retail sales, a firm labour market and persistent inflation pressures have all helped support the view that policy rates may stay higher for longer.

Importantly, the inflation story has not disappeared simply because oil prices have retreated from their highs either. Energy shocks tend to feed through supply chains, transportation costs and services prices with a lag, suggesting inflation pressures may prove stickier than markets had anticipated.

The bottom line, therefore, is the near-term outlook for the dollar remains constructive. One caveat to bear in mind though is month-end, quarter-end and half-year portfolio rebalancing flows, alongside large options expiries, which could create some noise over the coming week. That may limit the dollar’s ability to extend gains immediately, even as the broader backdrop of resilient US growth, persistent inflation and a hawkish Fed continues to provide support.

EUR: Still a laggard after dovish Lagarde

EUR/USD remains under pressure, with the pair showing increasing vulnerability to breaking below 1.14. A key catalyst of weakness yesterday was ECB President Christine Lagarde pushing back against expectations of a more forceful policy response to the Middle East conflict. Her remarks contrasted with the relatively hawkish rhetoric from Chief Economist Philip Lane and other policymakers last week, prompting a decline in both German yields and the euro as markets pared expectations for further ECB tightening.

The move reinforces a theme that has become increasingly evident in recent weeks: EUR/USD is being driven more and more by the rates channel. Following the Fed’s hawkish tone last week, the dollar continues to benefit from strong momentum, and the dovish signals coming from Europe accentuate the euro’s troubles.

That said, downside risks may be more contained than they were earlier in the conflict. Progress in US-Iran negotiations has helped reverse a significant portion of the eurozone’s earlier terms-of-trade shock, with energy prices moderating from their peaks and reducing some of the pressure on the region’s growth outlook.

Attention now turns to today’s PMI releases across the eurozone, UK and US. While the surveys will provide an updated read on economic momentum, they may not yet fully capture the improvement in sentiment following the interim US-Iran peace agreement.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: June 22-26

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.