USD: Dollar positive

Sections written by: Kevin Ford

All macro releases yesterday coming out of the US were dollar positive. Initial applications for jobless benefits in the US fell to the lowest since mid-July, according to Labor Department data. This decline signals a resilient labor market with relatively few layoffs, and the number of claims remains too low to suggest an impending recession. The four-week moving average, a smoother gauge of claims, also dropped to 237,500. Meanwhile, continuing claims, which measure the number of people receiving benefits, were largely unchanged at 1.93 million after the previous week’s data was revised upward.

Furthermore, the revised Q2 GDP reading was updated from 3.3% to 3.8%, marking the fastest pace in nearly two years. This upward revision was driven by stronger-than-expected consumer spending. These recent data points, combined with recent hawkish ‘Fedspeak’, have propelled the USD to climb almost 1% in the last five days.

Since August, we have been arguing that the bar for continued US dollar weakness has risen. The market’s recent dollar depreciation was largely a result of currency hedging and portfolio repositioning, not a wholesale dumping of US assets. While the consensus view still points to further dollar weakness toward the end of the year, we’ve noted several factors that make a continued decline more challenging. These include the resilience of US economic growth, the continuous floor provided by historical fiscal deficit, a cautious Fed, and a market that has already priced in much of the expected easing. The dollar’s performance is now more dependent on actual economic outcomes rather than just market expectations of a dovish Fed.

The dollar’s recent resilience is difficult to ignore. Many market participants had anticipated that last week’s Fed meeting would be the catalyst for the USD to weaken further. However, Fed Chair Powell made it clear that the normalization path isn’t a done deal and the two rate cuts that markets are expecting in the remaining two meetings this year are far from guaranteed.

Today, we got the core PCE report. Consumer spending in the U.S. picked up more than expected in August, showing just how resilient consumers continue to be, even as inflationary pressures remain steady. According to data released Friday by the Bureau of Economic Analysis, inflation-adjusted spending rose 0.4% for the second month in a row. Meanwhile, the core personal consumption expenditures (PCE) price index, which strips out food and energy and is closely watched by the Federal Reserve, ticked up 0.2% from July and climbed 2.9% compared to a year earlier, just as expected.

We’ve been flagging since August that the Fed’s dilemma isn’t going away, and that stagflation, even in a mild form, remains the primary macro risk. This risk could cap the momentum in global equities, which have recently seen indexes around the world hit all-time highs. Given that underlying pressures are broad-based across the US CPI basket, with 72% of CPI components now increasing at an annualized pace above 2%, a level not seen since mid-2023, markets may be in for a reckoning.

CAD: Decent July GDP surprise, new monthly high for the USD/CAD

According to Statistics Canada, the Canadian economy showed a modest rebound in July 2025, with real Gross Domestic Product (GDP) growing 0.2% month-over-month, marking its first expansion in four months. This increase was predominantly driven by a 0.6% surge in goods-producing industries, where the mining, quarrying, and oil and gas extraction sector led the way with a notable 1.4% expansion following a ramp-up in oil sands production. While the services-producing industries edged up 0.1%, propelled by growth in wholesale trade and real estate (which hit a new record high), the overall growth was tempered by a decline in retail trade ($$-1.0\%$$). Furthermore, the manufacturing sector’s 0.7% rise revealed a mixed impact from trade dynamics, as a significant expansion in pharmaceutical manufacturing and motor vehicle parts was partially offset by a sharp decline in primary metal manufacturing that coincided with the doubling of U.S. tariffs on Canadian steel imports.

Although the news has slightly helped ease the pressure on the USD/CAD, net short positioning has returned, and a widening U.S.-Canada yield differential has also helped pushed the USD/CAD closer toward its 200-day simple moving average (SMA) at 1.40. September has offered little support for the Canadian dollar. Recent data has reinforced expectations of a stagnant economy and aligned with the Bank of Canada’s (BoC) view that downside risks have increased. Last week’s dual policy updates from the Fed and the BoC further exposed the Canadian dollar to U.S. dollar strength. The divergence in positioning and central bank tone, with a more dovish BoC and a more hawkish Fed, coupled with hawkish ‘Fedspeak’ this week, helped push the USD/CAD to a monthly high of 1.395. Although the pair is technically overbought in the short term, only a significant upside surprise in Canadian macro data could prevent the USD/CAD from breaking back above 1.40. Also, US macro data hasn’t been of help for the Loonie, as it’s surprised to the upside. While next week’s Canadian manufacturing PMI will be closely watched, the primary focus will be Friday’s U.S. payrolls report, which could confirm the dollar’s recent momentum.

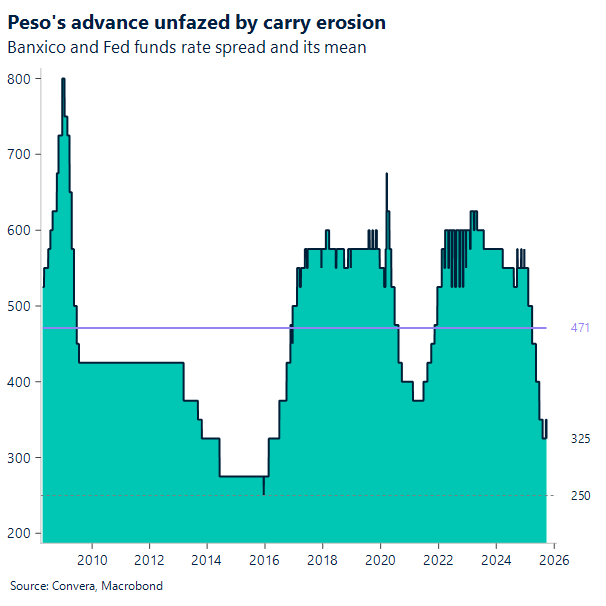

MXN: Peso struggles during the week

In a widely anticipated move, Banxico’s Governing Board voted to cut its overnight interest rate by 25 basis points to 7.50%. This decision marked the tenth consecutive rate cut, bringing the benchmark rate to its lowest level in three years as the central bank continues its easing cycle. The action was largely in line with market expectations, reflecting Banxico’s confidence in the disinflationary process, despite a recent uptick in core inflation, and its commitment to supporting Mexico’s slowing economic growth. The vote was not unanimous, however, with one board member dissenting in favor of holding the rate, highlighting the ongoing debate about the pace of monetary normalization amidst global and domestic uncertainties.

The central bank’s decision on the pace of rate cuts has been influenced by the interest rate differential between Mexico’s overnight rate and the U.S. Federal Funds Rate. This spread, a key factor for the Mexican peso’s stability, now stands at 325 basis points, moving closer to its historical low of 250 basis points. Previous meeting minutes revealed that members view Mexico’s “relative position” as key. One noted that despite the narrowing gap, the peso remains resilient thanks to a competitive volatility-adjusted differential. Another suggested there’s still room for cuts, but emphasized caution, as rates are nearing neutral and market volatility could shift the relative advantage.

In the week leading up to the rate cut, the Mexican peso (MXN) has experienced renewed volatility. After touching a year low, the currency rebounded to around 18.5 from 18.2, as the U.S. dollar strengthened in response to upbeat U.S. macro releases, some nervousness coming back to global markets and dollar strength. This highlights the peso’s sensitivity beyond domestic monetary policy to external sentiment and its relative performance against the dollar. Still, the Peso is up 1% month-to-date versus the US Dollar.

Next week, key domestic releases include the unemployment rate, manufacturing PMI, and gross fixed investment, while the main macro driver will be Friday’s U.S. nonfarm payrolls report.

Tariffs: A fresh round of tariffs

U.S. President Donald Trump announced a significant expansion of his tariff policy on Thursday, September 25, 2025, with new duties set to take effect on October 1. The most striking measure is a 100% tariff on any branded or patented pharmaceutical product, though this will be waived for companies that are actively “breaking ground” or “under construction” on manufacturing plants within the United States. In addition to this major healthcare measure, the administration will impose a 25% tariff on all imported heavy-duty trucks, citing the need to protect domestic producers like Peterbilt and Freightliner from “unfair outside competition” and for national security reasons. Furthermore, the new duties extend to home furnishings, including a 50% tariff on kitchen cabinets and bathroom vanities and a 30% tariff on upholstered furniture. As previous tariff news, this new round of tariffs, intended to accelerate reshoring, immediately raised concerns among business groups and healthcare advocates about the potential for higher costs for consumers and disruptions to essential supply chains. The news has had no immediate impact in FX.

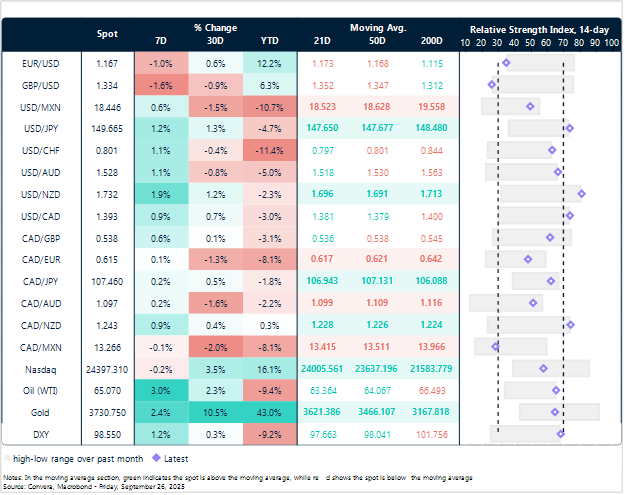

US Dollar recovers against all G-10

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: September 22-26

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.