Written by Convera’s Market Insights team

Check out our latest Converge Market Update Podcast where our Global Macro Strategist, Boris Kovacevic, breaks down this week’s most notable macroeconomic news.

Dollar stronger going into Fed day

Boris Kovacevic – Global Macro Strategist

Global investors have become comfortable pricing in the eventual turn of the global monetary policy cycle to a more accommodative stance at the end of last year. However, the big macro theme in early 2024 has been the paring back of G3 policy easing bets as inflation rates have somewhat rebounded. This has led to a rebound in bond yields and the Greenback, without putting pressure on equity markets. Volatility across assets remains low, though, despite the ambiguity surrounding the future policy path of central banks. One reason for the lack of price movement in FX: the synchronization of policy pricing.

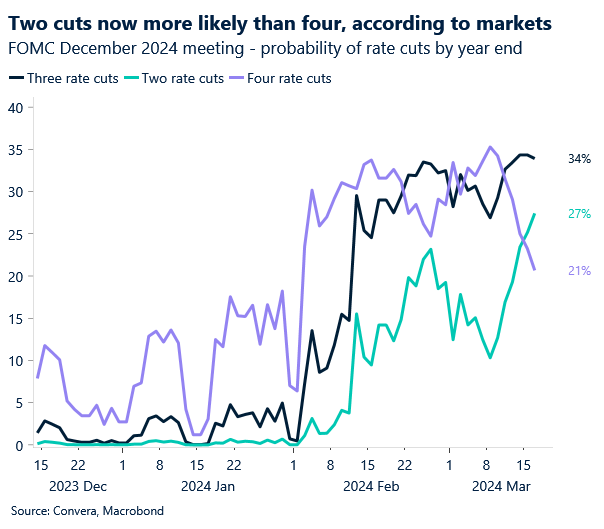

Against this backdrop, today’s FOMC meeting will most likely not move the needle when it comes to this lack of volatility. The March meeting will function as the steppingstone for policy makers to communicate their views on inflation and the economy and will make it easier to gauge how likely a rate cut in June will be. Markets currently see the probability of this scenario at around 55%. There has emerged a debate about the possibility of the FOMC raising the median dot plot to show just two rate cuts for 2024. We do not see this as our base case, given the weakening of leading economic indicators and the moderation of the labor market. However, it can not fully be ruled out as inflation expectations have risen in recent weeks.

The US dollar is going into the meeting with confidence and four daily consecutive appreciations under its belt. A dovish tilt from Jerome Powell during the press conference could induce some weakness into dollar pricing under the assumption that the dot plot remains unchanged. The Greenback is up against 85% of the worlds currencies year-to-date with DXY having risen 2.4% in 2024 so far.

UK inflation slows to 2 ½-year low

Ruta Prieskienyte – FX Strategist

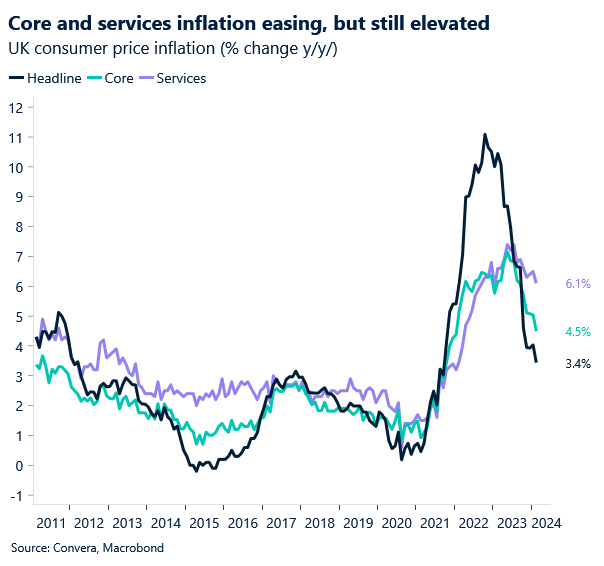

The latest inflation report confirmed an expected slowdown in British inflation rate. The headline inflation rate eased to 3.4% y/y in February, a low not seen since September 2021, while the core rate fell to a two-year low of 4.5% y/y. Both prints came in lower than expected with the slowdown in the headline rate predominantly driven by a slowdown in price increases for food and several service sector components. Despite the lower-than-expected readings, GBP/USD remained largely unchanged around $1.2710 level as investors turn their attention to impending decisions from both the Bank of England (BoE) and the Fed.

The BoE is widely expected to maintain its rates at 5.25% on Thursday, with UK policymakers leaning towards potential rate cuts in August, a departure from the anticipated moves by the ECB and the Fed, both expected to act in June. We expect the BoE to reiterate its previous forward guidance that rates need to stay sufficiently restrictive for an extended period. Markets are currently pricing in 70bps of easing for 2024, with the probability of an August rate cut increasing to 77% on the back of a downside surprise in today’s inflation print.

Looking ahead, on an average FOMC day we tend to observe the British Sterling appreciate against the US dollar and today’s reaction could fit the historical patterns yet again. FOMC is expected to stick to January’s script, but if Powell reiterates that Fed is ‘not far’ from confidence to cut interest rates, this could come across as more dovish than intended, given recent upward surprises in US inflation prints. For now, GBP/USD enters the day with a bearish bias and if the pressures continue to persist, the pair could violate the 50-day SMA and challenge the March support of $1.2600, which lies just above the 200-day SMA. A dive below that region could open the door for the 2024 low of $1.2517.

Euro depreciates on rate cut hopes

Ruta Prieskienyte – FX Strategist

The euro continued to trade cautiously against the US dollar as investors opted to steer on the prudent side despite better-than-expected Eurozone data. The as latest Eurozone wages data cemented the case for the ECB rate cuts in June, but the yield on the 10-year German government Bund remained largely unchanged around 2.45% as traders shift their attention to FOMC rate decision later today.

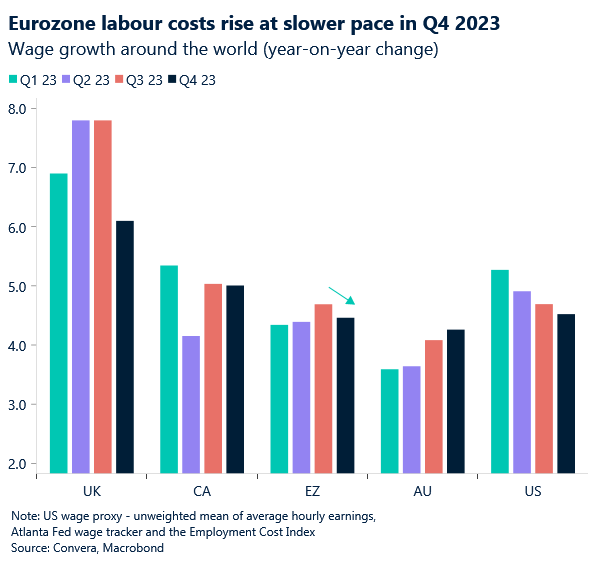

The latest data from Eurozone revealed that bloc’s labour costs rose by 3.4% y/y in Q4 2023, the slowest pace since Q3 2022, and below market expectations of 4.6%. Although the moderation in pay growth strengthens the case for a June rate cut, interest rate traders are hesitant to reprice ECB rate cut expectations ahead of the FOMC decision. Currently the market expects 85bps of cuts by year-end and the first rate cut to occur in June with a 65% probability of a June rate cut. Elsewhere, the ZEW Indicator of Economic Sentiment for Germany reached its highest level since February 2022, but was shrugged off by FX markets as investors are now looking for a larger bone to chew on.

On a typical FOMC day we tend to see EUR/USD appreciate by an average of 0.14% d/d on close-close basis, but could this time be any different? FOMC is expected to stick to January’s script and continue to stress the need of more data to bring greater confidence that inflation has sustainably come down to its 2% target. If Powell continues to emphasise that Fed is ‘not far’ from confidence to cut interest as he did so less than two weeks ago, the comment this time round could be interpreted as dovish given the recent uptick in US inflation data, sending US dollar depreciate lower. However overall risks to EUR/USD appear to be tilted to the downside as reasons for higher ECB’S policy rates beyond June are depleting, while the Fed does not appear to be any closer to cutting rates than it was back in January.

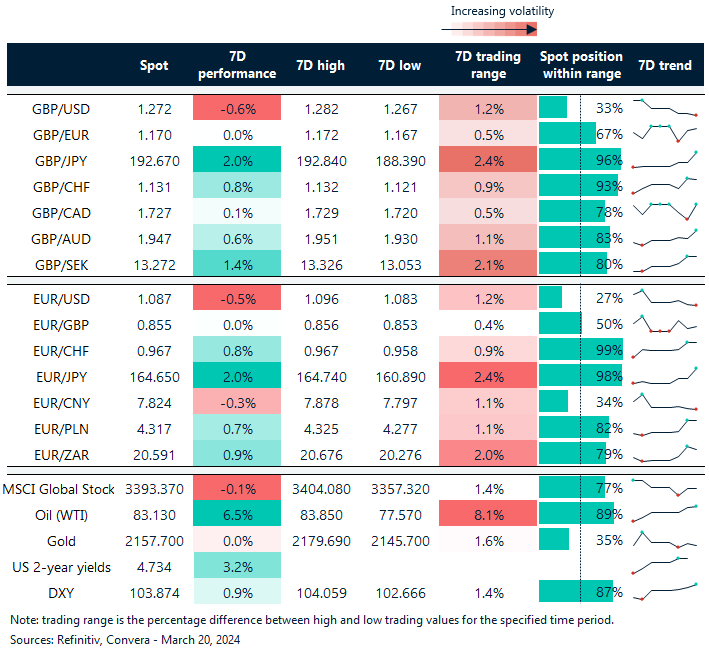

GBP/USD unfazed by lower than expected inflation print

Table: 7-day currency trends and trading ranges

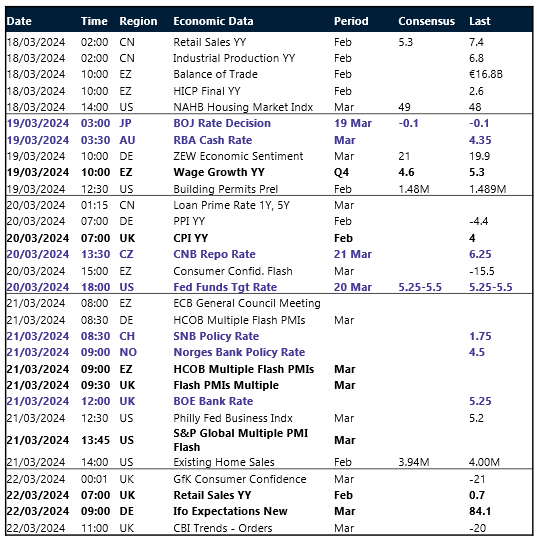

Key global risk events

Calendar: March 18-22

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Join us for Convera Live! A series of in-person events discussing the future of global payments.