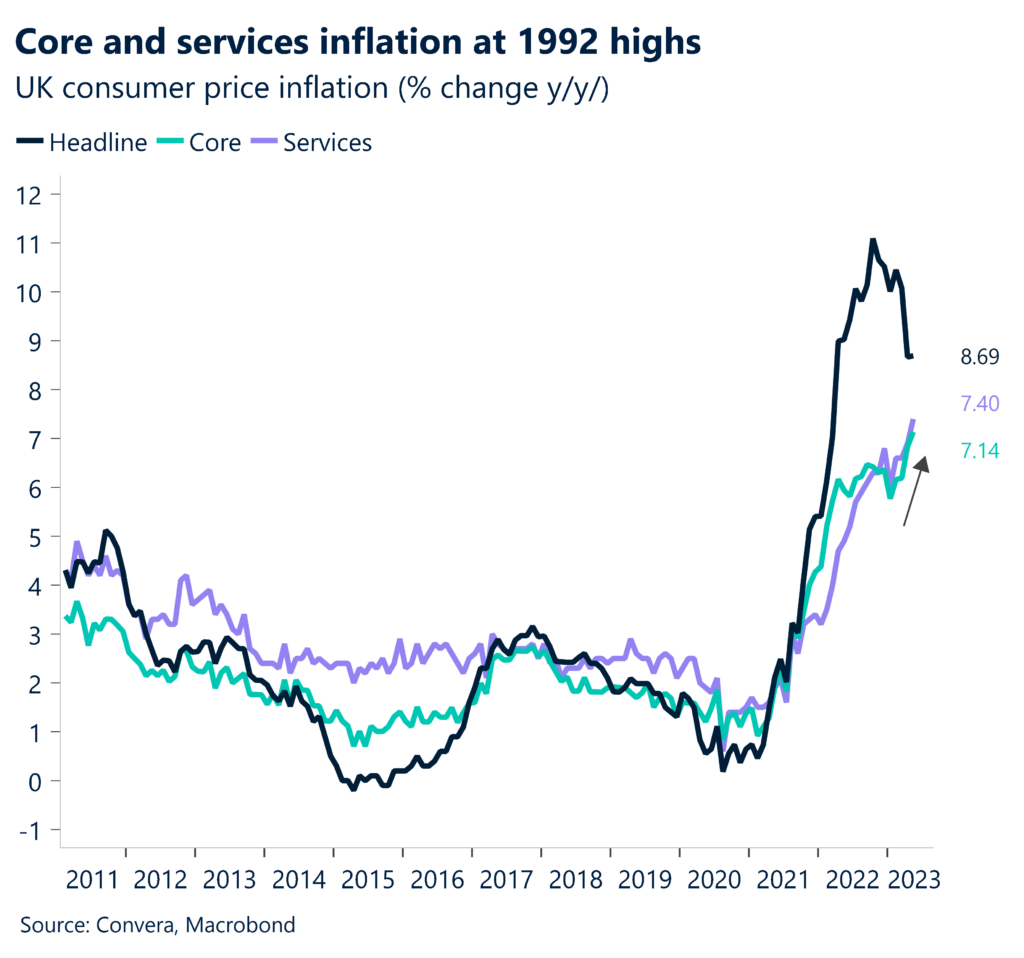

UK inflation above forecasts for fourth month running

Consumer price inflation in the UK held steady at 8.7% in May, unchanged from the previous month and above market expectations of 8.4%. Core inflation came in hotter at 7.1%, and services inflation at 7.4%, both at the highest since March 1992. A 25-basis point rate hike by the Bank of England (BoE) tomorrow is fully priced in, but markets are now pricing a 54% chance of a 50-basis point hike, up from 25% yesterday.

Amongst developed economies, stubborn core inflationary pressures are not unique to the UK (think Austria, Belgium, Finland and Netherlands), but when compared to the US and Eurozone as a whole, where prices have rolled over, price pressures are clearly more persistent. As CPI inflation came in well above the BoE’s forecast for the fourth successive month, with core prices unexpectedly accelerating once again, the pressure is increasing on the BoE to hike rates more aggressively. Investors had already ramped up expectations that the key BoE rate would rise to as much as 6% early next year after a string of hotter-than-expected wage and price data. The latest inflation figures add to this narrative and without push back from the BoE tomorrow, could we see sterling build on recent gains and stretch towards $1.30 versus the US dollar?

It’s not a simple as that unfortunately. Despite diverging monetary policy expectations helping the pound to strengthen, concerns will be mounting about the ability of the BoE to protect the economy from stagnating, which may limit the pound’s appeal.

Strong data before Powell’s testimony

US investors are preparing for the testimony of Federal Reserve (Fed) Chair Jerome Powell before the Senate later today in his first speech after the central bank decided to leave rates unchanged last Wednesday. The data flow since then has been mixed, with retail sales beating (0.3% vs. 0.1%) the consensus estimate, while industrial production for May unexpectedly shrunk by 0.2%.

While regional Fed manufacturing indicators continue to signal subdued growth ahead, with the Philadelphia Fed index staying in negative territory (-13,7) for the tenth consecutive month in June, optimism surrounding the bottoming of the housing market is starting to broaden. Housing sentiment has increased six months in a row, according to the NAHB/Wells Fargo Housing Market Index, rising to the highest level since July 2022. The recovery of the leading indicator has preceded yesterday’s surprise jump in housing starts to 1.631 million in May, a 21.7% increase from the previous month.

The positive macro flow has allowed investors to continue to reprice their expectations of another Fed hike at the July meeting higher. The probability of the central bank raising its interest rate one more time to 5.25% – 5.50% has climbed from 62% a week ago to 79% with markets expecting no rate cuts to materialize this year. For the next 12 and 24 months, around 50 and 170 basis points of cuts are being priced in. The positive repricing has put the US currency on a more solid footing, after the US dollar index recorded three consecutive weekly losses.

Euro stalls despite pricing of 4% terminal rate

The euro fell for a third day on the bounce against the US dollar, but found support just above its 50-day moving average having surged through it last week. EUR/USD is grappling with the $1.09 handle this morning ahead of a fairly packed European Central Bank (ECB) schedule of speakers today. Against the pound, the euro is battling back from 10-month lows although GBP/EUR managed to rebound off its 100-week moving average.

One reason for the euro’s recent weakness relates to the risk-off mood across financial markets as European shares fell for a second consecutive session on Tuesday as investors evaluated the global economic and monetary policy outlook, while also analysing the recent statements made by ECB policymakers. Recent hawkish comments from several ECB officials have led to markets fully pricing in a 4% terminal rate for the first time since March. However, ECB Governing Council member Francois Villeroy de Galhau struck a more dovish tone, stating possible further rate hikes would be less important in fighting inflation than the duration of tight monetary policy. ECB Governing Council members Peter Kazimir and Isabel Schnabel speak today to provide more details on how high terminal rates for the Eurozone will be, and just as importantly, when they will reach that point.

Policymakers and investors continue to be driven by incoming macro data and the global economic outlook. The fact that German producer prices rose at their slowest pace in more than two years in May will be weighed against China’s move to cut its benchmark loan prime rates for the first time in 10 months in its latest attempt to stimulate the country’s slowing recovery – another crucial dynamic for the euro’s outlook.

Risk off mood caps EUR and GBP gains

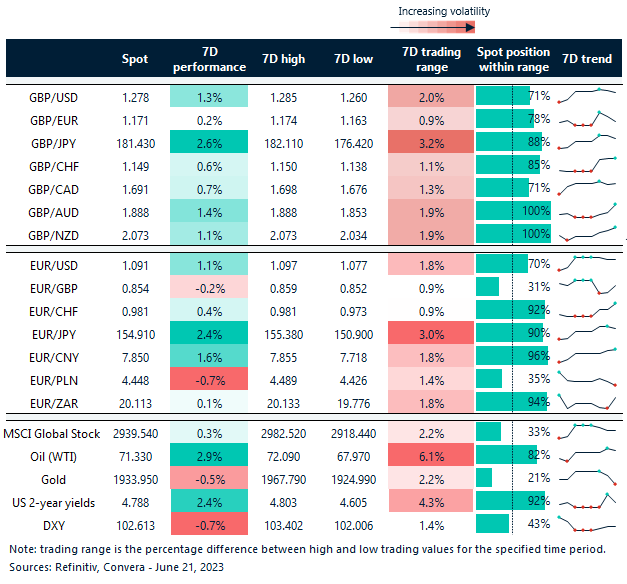

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: June 12- June 16

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.