Dollar whipsaws after solid ADP and ISM

EUR/USD bounced off its 100-day moving average near $1.0825 to clip $1.09 yesterday before plunging back to its low after a string of solid US data. The main focus today is the US jobs report, but expectations will have been impacted by the much stronger than expected ADP data and fewer claims for unemployment benefits than expected.

While the surveyed market consensus for non-farm payrolls (NFP) is 225k, something closer to 300k might be expected given private payrolls surged last month in the biggest increase since February 2022 and significantly above forecasts. In addition, continuing claims fell to the lowest in four months. Meanwhile, June’s ISM services index rebounded from a barely positive 50.3 to 53.9, smashing expectations of 51 and clocking its third biggest monthly change higher since October 2021. At the same time, the ISM survey showed a measure of prices paid by businesses fell to more than a three-year low, a sign inflation should continue to cool. The strong US labour market coupled with the resilience of the services sector continue to challenge recession concerns in the face of tighter monetary policy. However, the New York Federal Reserve (Fed) is still putting the US recession probability at around 70%, the highest level in 40 years, and even if a recession is avoided this year, the Fed may have to keep hiking rates, because of stickier inflation, which would once again increase the recession risk down the road.

Money markets are currently assigning a nearly 90% chance of a 25-basis point rate hike by the Fed later this month, while the odds for another quarter-point increase in September went up to 30% from around 20% earlier. Although the dollar has since surrendered yesterday’s gains, all eyes are firmly fixed on the US jobs report today for further trading impetus.

Euro below $1.09 going into NFP

While the macro data coming out of the US has been overshadowing anything happening in Europe this week, second tier data releases have still been interesting for us. Given the manufacturing recession in Germany, the jump in factory orders by 6.4% in May has drawn attention, given that markets expected demand for German good to increase modestly by 1.2%. However, the optimism did not hold on for too long as today’s industrial production numbers once again surprised to the downside with a monthly fall of 0.2%.

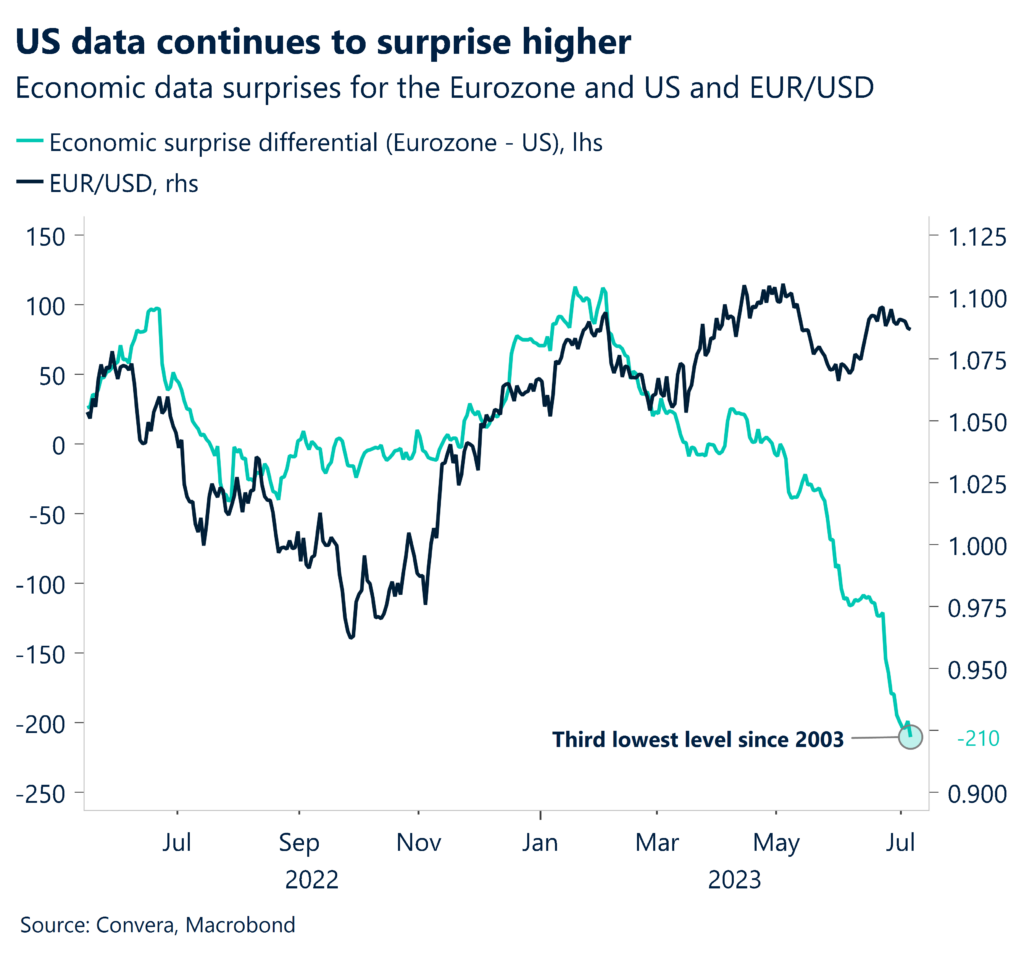

The euro has somewhat decoupled from the incoming macro data, looking at the fading correlation between EUR/USD and multiple variables like our German hard data proxy or the Citi surprise index differential between the Eurozone and United States. The currency pair will still most likely fall this week, given the exceptionally strong data from the US and the expectations that the Fed will have to do more to tame inflation. The same cannot be said about the European Central Bank (ECB). While Christine Lagarde confirmed the institution’s commitment to continue the tightening cycle in a speech given yesterday, some doubts are starting to creep into investors’ minds.

We will hear once more from ECB President Lagarde today, but the main event will most definitely be the US labor market report. Going into the release, EUR/USD remains stuck below $1.09 with a slight downward bias given yesterday’s strong ADP numbers. EUR/CNY is pausing its multi-month rally and is likely to fall on the week for the first time since the beginning of May.

Disconnect between UK stocks and currency

Sterling rose to a two-week high against the euro and US dollar yesterday as financial markets bet that the Bank of England (BoE) will raise rates to 6.5% early next year. Rate expectations eased though following a survey from the BoE showing British companies’ expectations for selling price inflation had cooled. Sterling recoiled but remains on track for a weekly gain against most majors barring the Japanese yen after seven successive weekly rises.

The BoE’s Decision Maker Panel, often cited as a key part of policy discussions, showed expectations for output price inflation in the coming year fell to 5.3% in the three months to June, compared to 5.4% in the three months to May – the lowest reading since March 2022. This mirrors what we’ve seen in some of the other leading indicators of inflation, including producer and import price inflation which have come down dramatically over recent months. The prospect of higher rates has resulted in UK gilt yields surging higher to levels comparable with those seen during the global financial crisis in 2008. Although this has been constructive for the pound, it has weighed heavily on UK stock indices, with homebuilders and construction dragging the FTSE 250 to near its biggest decline since March.

The FTSE 100’s dividend yield has also recently fallen below the UK 10-year yield, which climbed above 4.5% yesterday for the first time since the October gilt crisis. Hence, demand for UK stocks remains subdued, whilst demand for sterling remains buoyant amidst rate and yield differentials. Versus its one-year average rates, currently, GBP/USD is 5.7% higher, GBP/EUR is 1.8% higher, while GBP/JPY is 10.3% higher.

Sterling firms as rate expectations surge

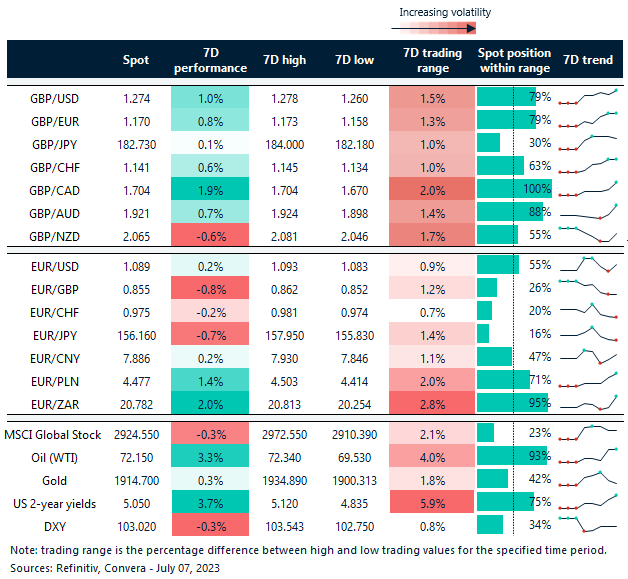

Table: 7-day currency trends and trading ranges

Key global risk events

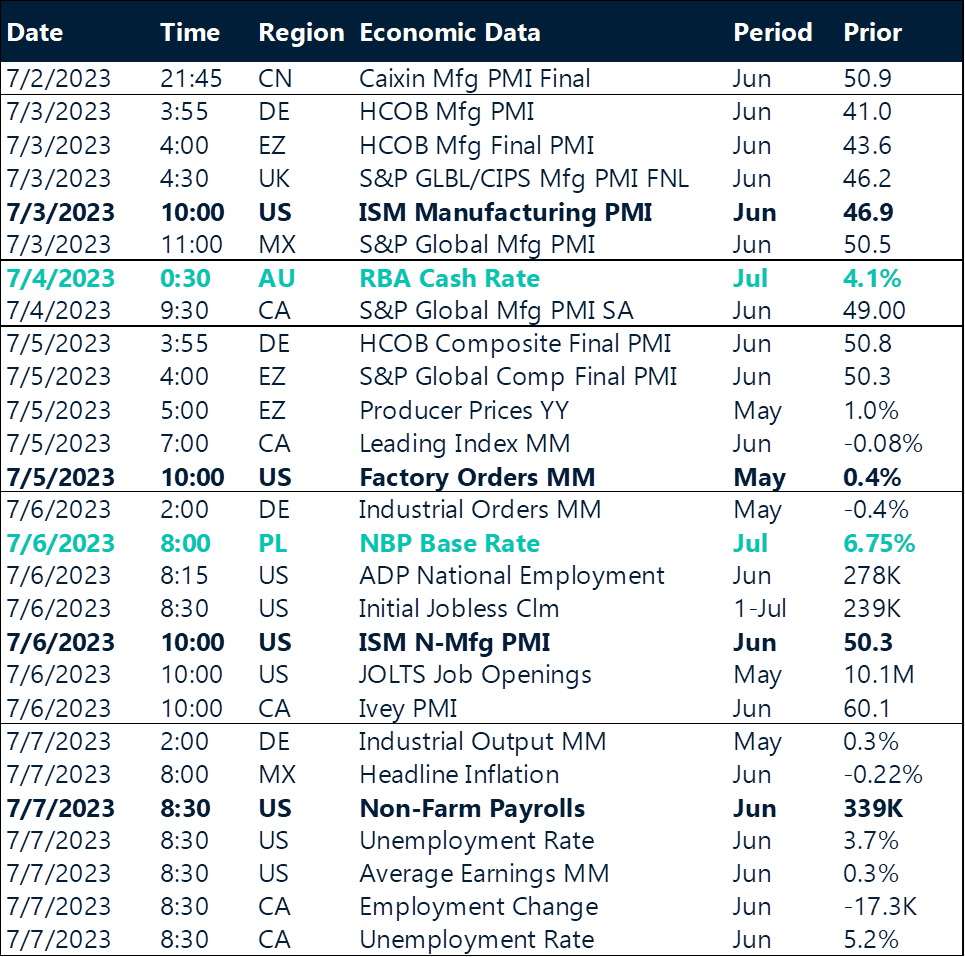

Calendar: July 3 – July 7

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.