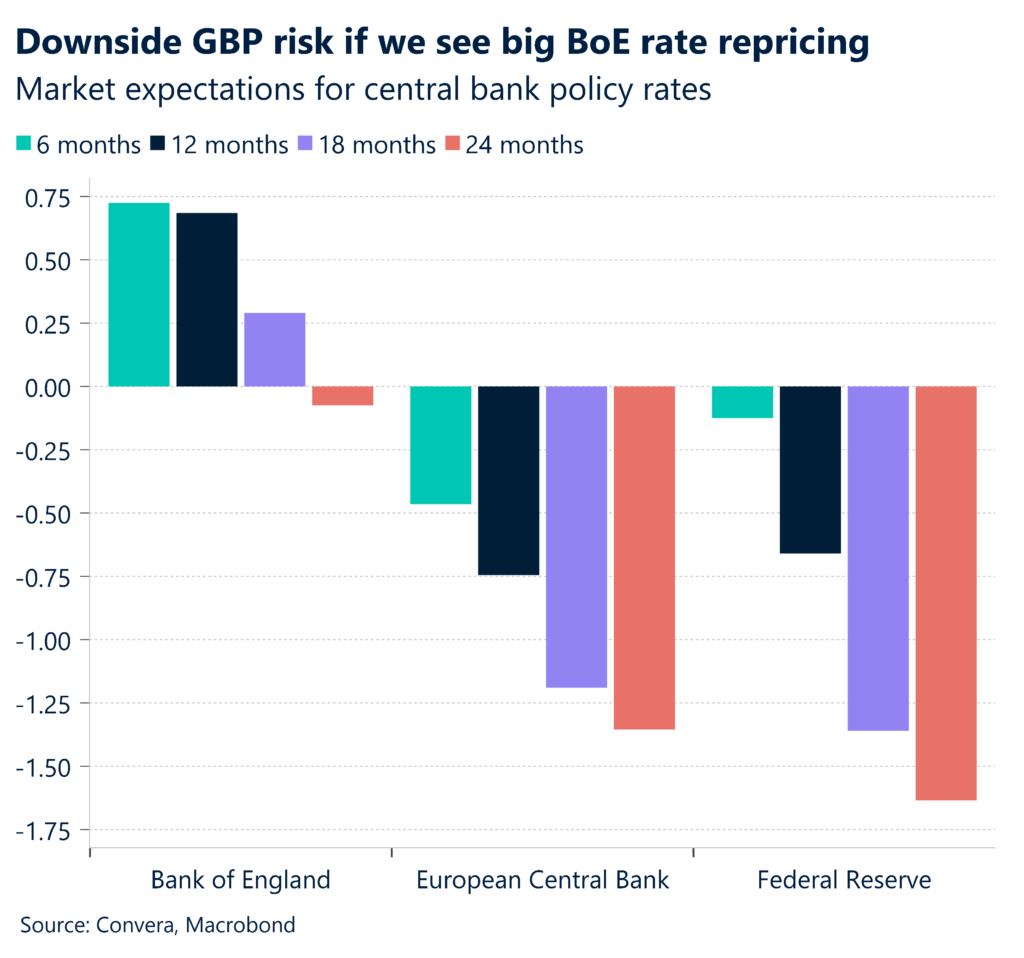

BoE hike expected, but what size?

Sterling fell to a circa 1-month low against the US dollar amid anticipation surrounding the Bank of England’s (BoE) widely expected 14th consecutive interest rate hike today. Money market pricing attaches a 60% probability of a 25-basis point rate hike. Another 50-basis rate hike wouldn’t be a big surprise but like markets we believe a hike from 5.00% to 5.25% is more likely. The vote split, press conference and Monetary Policy Report will also be closely eyed.

At the last BoE meeting, policymakers pledged to deliver further rate hikes if the ongoing inflationary pressures persisted. Since then, we’ve seen a downward surprise in the latest UK inflation data, with both core prices and services prices also rolling over. That said, consumer prices are still rising at the fastest pace amongst the G7, and strong wage growth and second-round inflation effects will remain a concern for the BoE. Hence, we still expect a hike, it’s just a matter of what size which could determine the reaction of the pound. We would have predicted the pound to weaken in the event of a smaller hike, but the depreciation over the last few days perhaps opens the door to a short-term rebound. Sterling has started August as it usually does, on the backfoot against the US dollar, but it is also weaker against the euro, Japanese yen and Swiss franc as demand for safer currencies increases, and demand for so called high-beta currencies (along with equities) decreases. Risk sentiment, therefore, remains another key driving force behind FX volatility too, but today, sterling will be dominated by the BoE.

Given the monetary transmission process is slower (meaning the desired impact of rate hikes is taking longer to hit the economy), the BoE may be reluctant to hike too much more from here to avoid a deeper economic downturn, but the pound remains exposed to the risk of a downsized rate repricing and narrowing yield spreads as a result. The 100-day moving average just under $1.26 could be a potential target.

Dollar governs safe haven demand

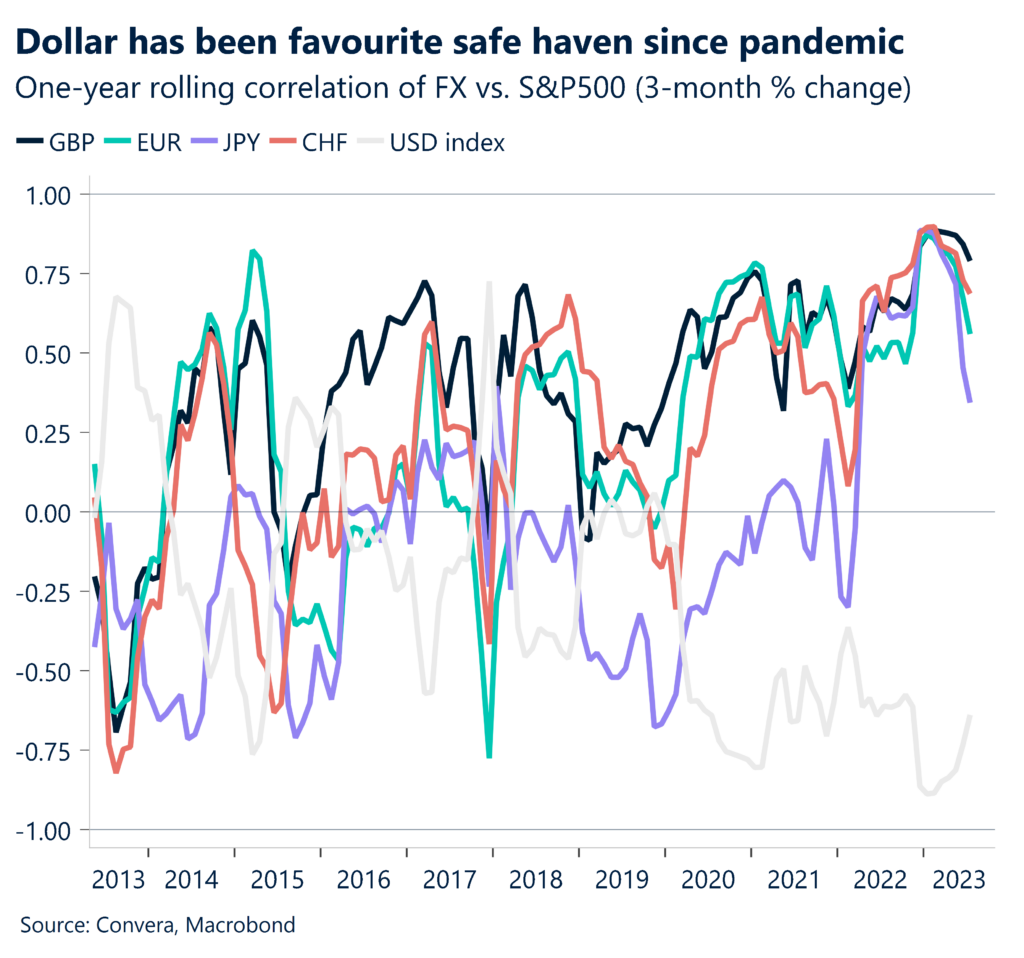

The US dollar advanced on strong US jobs data yesterday, but also thanks to safe haven flows despite the source of global risk aversion arising from a US credit rating downgrade. The US dollar index is on track for its third weekly gain in a row amounting to a 3% rise after rebounding from its lowest level since April 2022 midway through July.

Rattling global sentiment, rating agency Fitch downgraded the US to AA+ from AAA this week, and although the dollar initially took a knock with falling US Treasury yields, the safe haven status of the world’s reserve currency ended up attracting investor demand. To gauge the dollar’s haven status, we analysed the one-year rolling correlation of the annualised 3-month change in currencies, including the dollar index, against the US benchmark equity index. Interestingly, the traditional safe havens Japanese yen and Swiss franc have vastly underperformed the US dollar when equity markets have weakened, so yesterday’s FX gyrations made sense. Furthermore, we saw ADP’s private sector employment report once again surprise significantly to the upside, rising by 324k in July. This added to the dollar’s appeal ahead of the important non-farm payrolls report on Friday, though we remain cautious about this update given June’s sharp upside surprise was not matched by non-farm payrolls and the dollar suffered a deluge of selling pressure as a result.

Today we will also monitor the ISM non-manufacturing PMI, factory orders and initial jobless claims form the US, but if global risk sentiment continues to sour, expect the dollar to continue its advance.

Market and macro divergence

Excluding the recent slump this week, equity returns have defied expectations in the first half of 2023. Despite a backdrop of banking stress, rising recession risk, and materially tighter monetary policy than expected at the beginning of the year, equities have continued to march higher. Global manufacturing PMIs continue to fall though, creating a divergence that is surely due a correction.

Some equity markets have reached record highs recently, while others are close and most of the strong returns reflect a shift in market focus towards the AI theme, earnings, and growth potential over the inflation and rates narrative. However, in the US, for example, absent any pre-emptive Fed easing, we expect to see a more challenging macro backdrop for stocks in the second half of 2023. Moreover, amid this extreme divergence between equities and manufacturing PMIs, a significant correction for either could create market turmoil. It is true that we might see a big rebound for PMIs, spurring equities to new heights, but instead, we are still in the camp that economic slowdowns or recessions implied by PMIs will negatively impact currently inflated equity values.

Why does this matter? Risk sensitive currencies like the pound and euro have followed stocks higher this year, while the US dollar, which has a negative correlation with stocks, has depreciated. The recent souring of risk sentiment following the Fitch downgrade, has provided a glimpse of what a fall in equities might mean in the FX space.

Dollar dominates and risk aversion grips

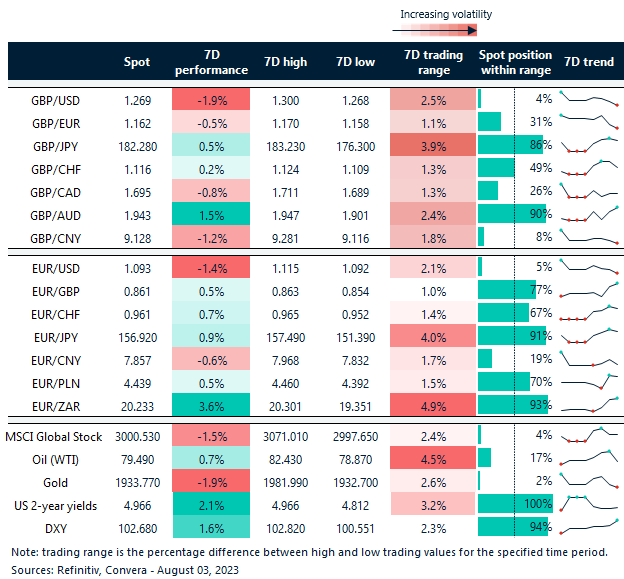

Table: 7-day currency trends and trading ranges

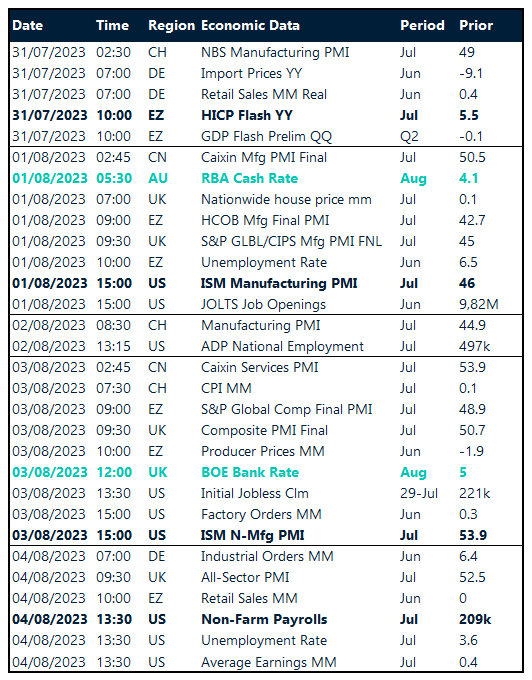

Key global risk events

Calendar: July 31- August 4

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.