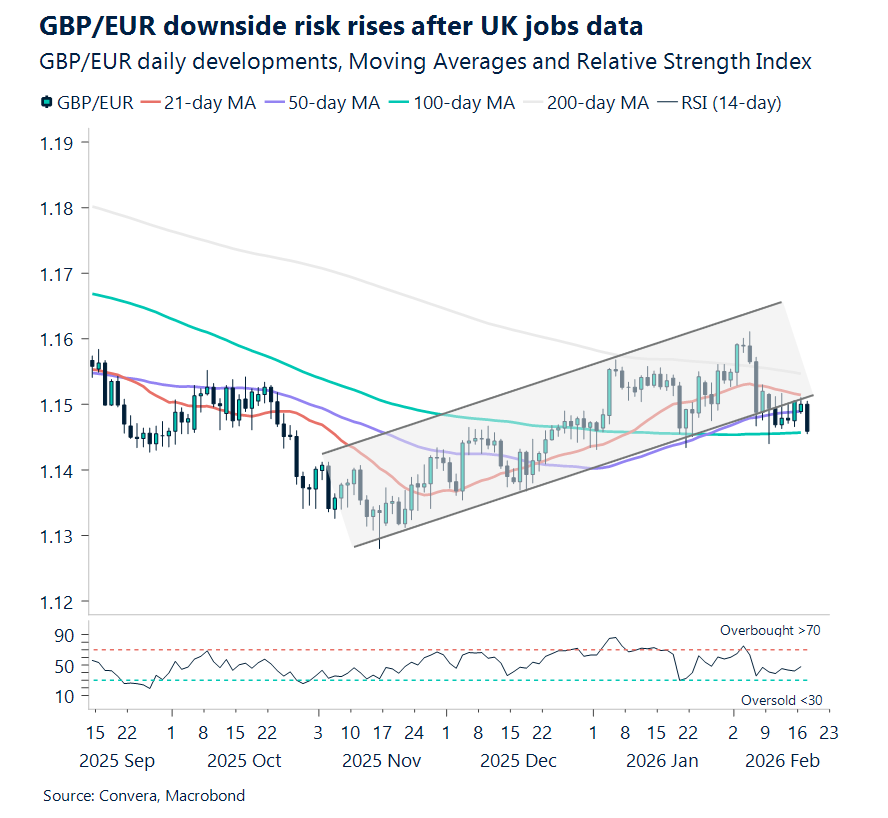

GBP: Sterling slides after dovish jobs report

Sterling is extending losses this morning after UK wage growth undershot expectations and the unemployment rate climbed to a near five‑year high. GBP/USD has slipped below its 21‑day moving average, putting the 50‑day near $1.3525 in view, while GBP/EUR is once again testing the key €1.1460 support zone we’ve highlighted for weeks.

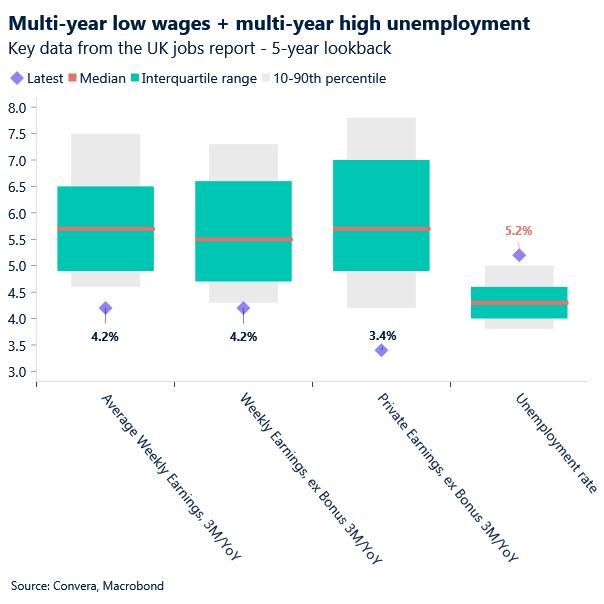

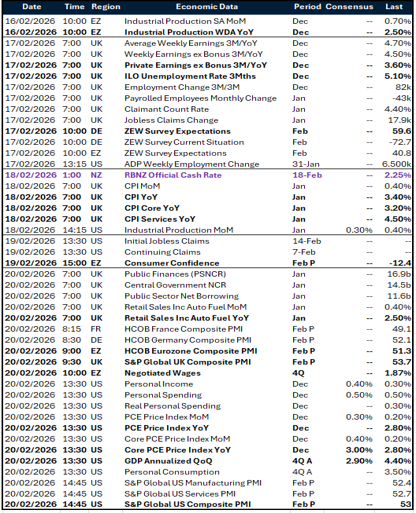

December’s weekly earnings rose 4.2% versus the 4.6% expected, while regular private‑sector pay — the BoE’s preferred gauge — slowed to 3.4%, its weakest pace in more than five years. With the Bank explicitly targeting a move toward 3.25% as consistent with 2% inflation, today’s print will be seen as progress.

The labour market is also loosening more visibly. Unemployment rose to 5.2% in the three months to December, the highest since early 2021, and payrolls fell by another 11,000 in January — taking the annual decline to 134,000. For policymakers already concerned about weak demand, this combination strengthens the case for further rate cuts.

Odds of a March BoE cut have climbed to roughly 80%, up from around 70% just a day ago. With expectations already leaning dovish, Wednesday’s inflation report doesn’t need to deliver much — simply showing that disinflation remains on track would be enough to lock in those views. Markets now fully price another cut before year‑end.

Against this backdrop, the bias for sterling remains to the downside — particularly as the currency has already shed much of its political risk premium ahead of next week’s by‑election, a vote likely to intensify pressure on Prime Minister Keir Starmer.

USD: Dollar finds a floor ahead of PCE

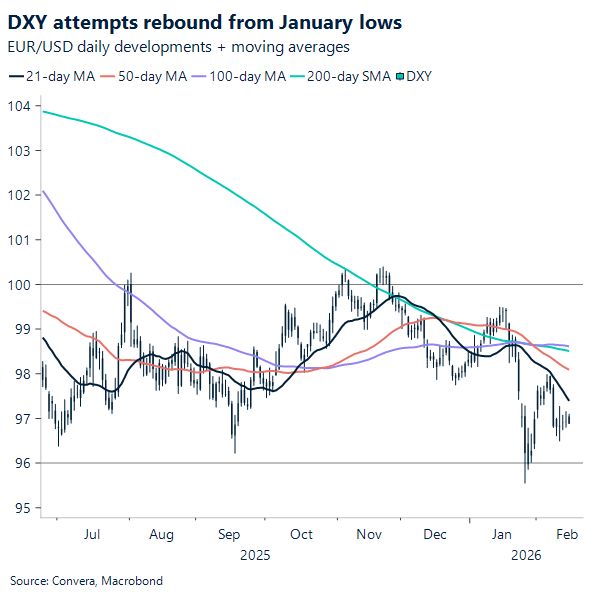

It was a quiet day for markets yesterday, with the US observing the Presidents’ Day holiday. US dollar’s price action was fairly muted, with its index edging back above the 97 level. The move looks justified: with the dollar still undervalued relative to macro‑warranted fair value, technical barriers lose robustness when encountered in such dislocated zones, and with no fresh catalysts to justify any imminent re‑widening of that divergence, mean reversion follows.

That said, sentiment toward the dollar, reminiscent of post-Liberation Day’s aftermath, remains soft. Recent eurozone discussions about strengthening the euro’s role in global markets and trade networks keep the USD diversification story alive in investors’ minds, making the dollar’s return to fundamentals more painful than anticipated. News over the weekend that the ECB expanded its EUREP repo lines from a narrow European audience to the global central bank community is a clear case in point.

The 21‑day moving average on the DXY appears fragile, with short‑squeezing flows likely to trigger a bullish crossover this week. While we do not expect much market reaction from the data, the Private Consumption Expenditure (PCE) deflator, the Fed’s preferred inflation gauge, due Friday, has its core component expected to tick higher on both a m/m and y/y basis from November’s figures. Barring a downside surprise, the release would help cement the index’s posture above the short‑term indicator. That said, we remain doubtful of any sustained move above 98 for now.

EUR: Risk reversals blink, trend holds

Amid growing interest in the euro’s internationalisation, euro‑area finance ministers met in Brussels yesterday to discuss ways to expand the single currency’s global role by promoting its use in both issuance and transactions, with the aim of diversifying away from US dollar. The meeting followed the ECB announcement over the weekend that it is prepared to offer euro liquidity to central banks around the world via EUR repo lines.

Such developments may not be persuading the euro to move higher against the dollar per se, but they would certainly lubricate bullishness in the event of further US‑led dollar weakness. In the short term, still sitting comfortably above fair value, the pair appears poised to drift lower in the absence of any imminent clear catalyst, although we have argued that with not‑so‑convincing US macro data, EUR/USD sellers have little to cling to when making the case for a sustained move lower. While a break below the 21‑day moving average at 1.1839 would be understandable this week, the bullish upside configuration should remain intact, with the February lows at 1.1766 acting as solid support for now. The options market captures the pair’s posture against these technical levels quite well: downside risk in the week ahead, with 1‑week risk reversals turning bearish for the first time since January, while further out, positioning appears more confidently bullish, persuading us away from calling the end of the euro’s ascent against the dollar since mid‑January.

For today, Germany’s and the eurozone’s ZEW surveys are due. The expectations sub‑index has accelerated from the April 2025 lows and now sits near the highs from 2021. It will be instructive to continue monitoring the series as 2026 brings less trade uncertainty and the much‑hoped‑for German fiscal stimulus.

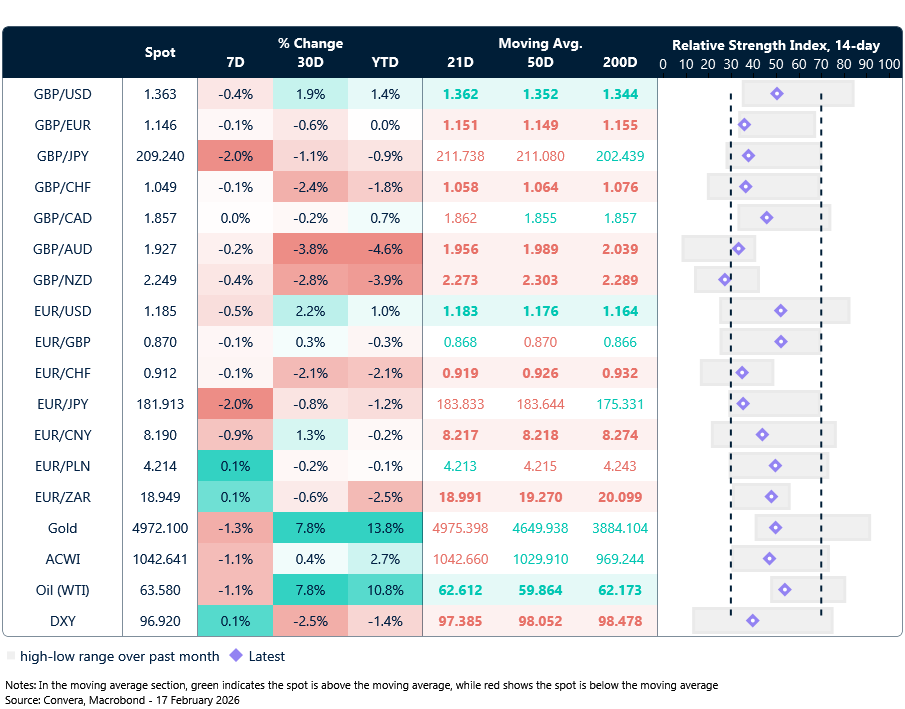

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

Calendar: February 16-20

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.