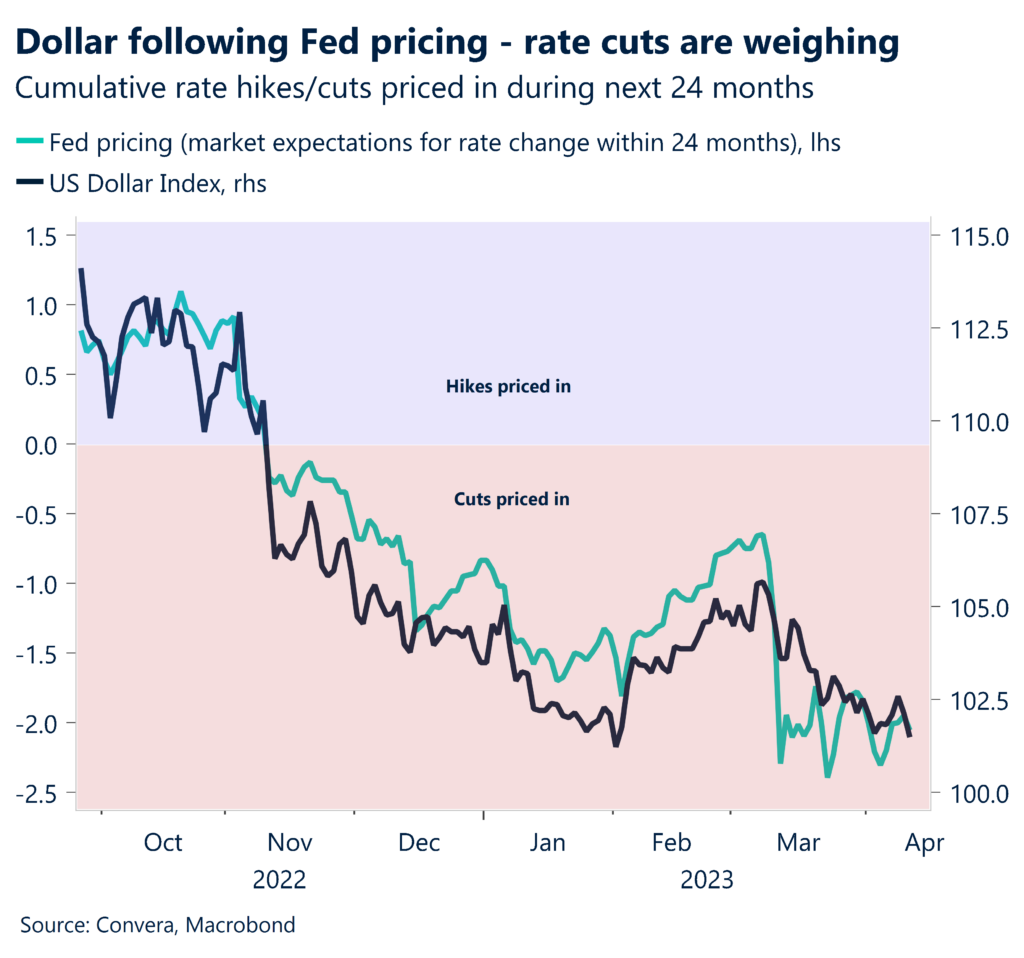

Dollar slumps after US inflation cools

US inflation eased last month to its lowest level in nearly two years, which sparked an uplift in market pricing of US Federal Reserve (Fed) rate cuts later this year. As a result, stocks and bonds rallied globally and the US dollar tumbled across the board with EUR/USD spiking to a fresh 2-month high just under $1.10.

Headline inflation has come down significantly since peaking in June last year, falling from 9.1% to 5% but core inflation remains highly elevated and even accelerated to 5.6% in March. However, prices excluding energy and food continue to be driven by the lagging housing component (shelter), which has reached another 40-year high, climbing to 8% during the last 12 months. Services inflation, excluding energy and excluding shelter, has started coming down from recent highs, which is another positive signal for the Fed and markets. This means that the trend of falling headline and rising core continues to play out, which might become a problem for the Fed given much weaker interest rate sensitivity of the services sector. Leaving the banking turmoil and lending uncertainties aside, the latest inflation print would still give the Fed strong arguments for continuing to raise interest rates. More than half of the items in the CPI basket still saw a price increase of above 5% during the last 12 months and wage growth continues to be elevated. However, given the lagged nature of monetary tightening on the real economy, hikes beyond May will be hard to justify with headline inflation slowing as significantly from month to month.

Before the CPI report, markets were pricing a 76% chance the Fed will hike by 25 basis points (bps) in May and then 39bps of cuts by year-end. Now, markets are pricing a 71% probability of a 25bps hike and over 50bps of cuts by year-end. So, while the odds of a May hike haven’t changed dramatically, the additional pricing of Fed cuts appears to be driving most of the dollar weakness. US producer inflation data today and retail sales on Friday are looming data risks to wary of.

Pound shrugs at no UK growth in February

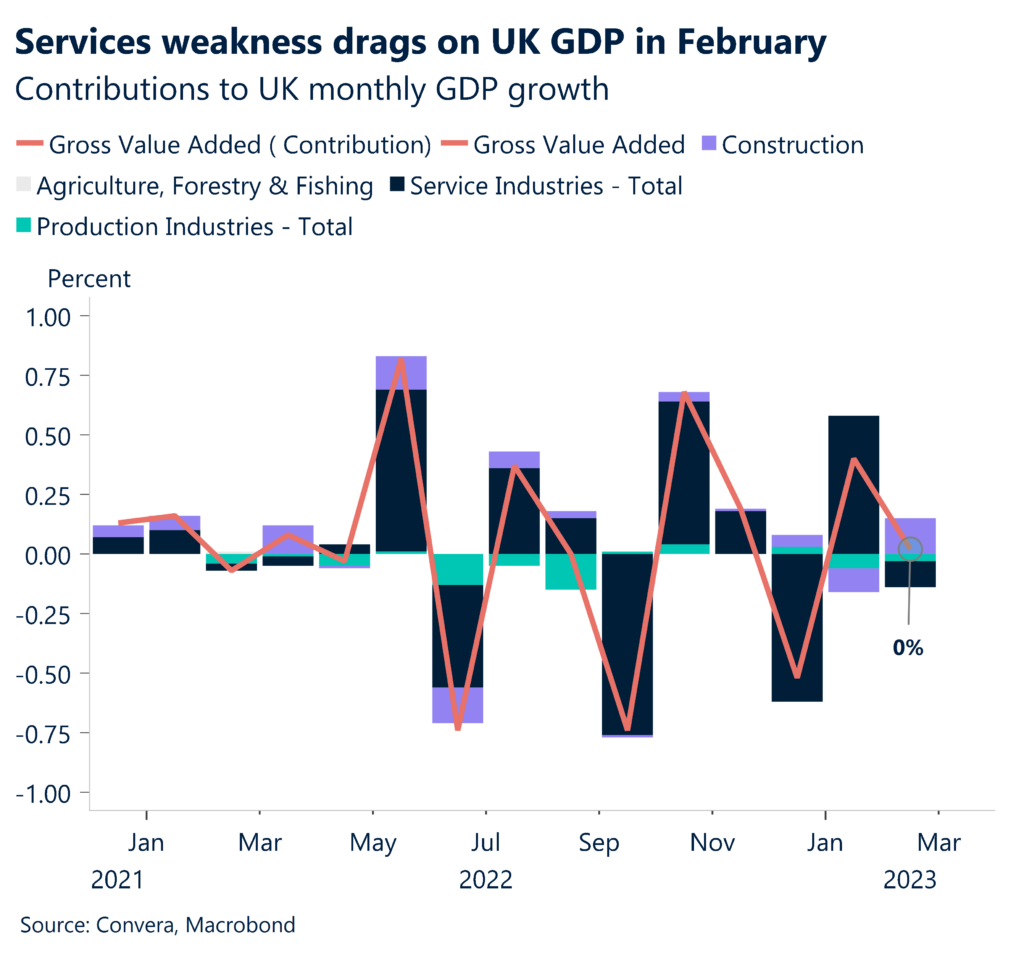

GBP/USD jumped from just under $1.24 to just below $1.25 in the immediate aftermath of the US inflation report yesterday. The pound, along with the FTSE 100 and UK gilts, rallied as slower US inflation points to the increasing possibility of the Fed pausing rate hikes. This morning, a mixed bag of UK GDP results has been largely overlooked by markets for now, but $1.25 has been reclaimed by sterling.

Strikes by civil servants and teachers held back growth in the UK economy in February according to the Office for National Statistics. UK GDP grew 0.1% in the three months to February and January’s growth was revised up a tick to 0.4%, however, the British economy stalled in February, with the services sector suffering the most. The largest contributor to the negative growth in services was education, which fell 1.7% due to teachers striking over pay. On a more positive note, the construction sector grew by 2.4% and UK GDP is now estimated to be 0.3% above its pre-coronavirus levels (at last). Although some forecasters are expecting the UK to avoid recession this year, it is still expected to be one of the weakest performing economies out of the G10. With UK inflation still in double digits, this makes for a difficult decision for the Bank of England in its upcoming meeting in May. If the BoE surprises by keeping rates on hold, the pound is likely to fold.

However, the technical picture appears more promising. GBP/USD is trading above all of its key daily moving averages and is supported by an upward sloping trendline developed since early March. GBP/USD is now circa 3% higher year-to-date and nearly 4% above its 1-year average rate. The big question is whether $1.30 trades this year or whether $1.25 is the new ceiling?

Euro zeroing in on $1.10

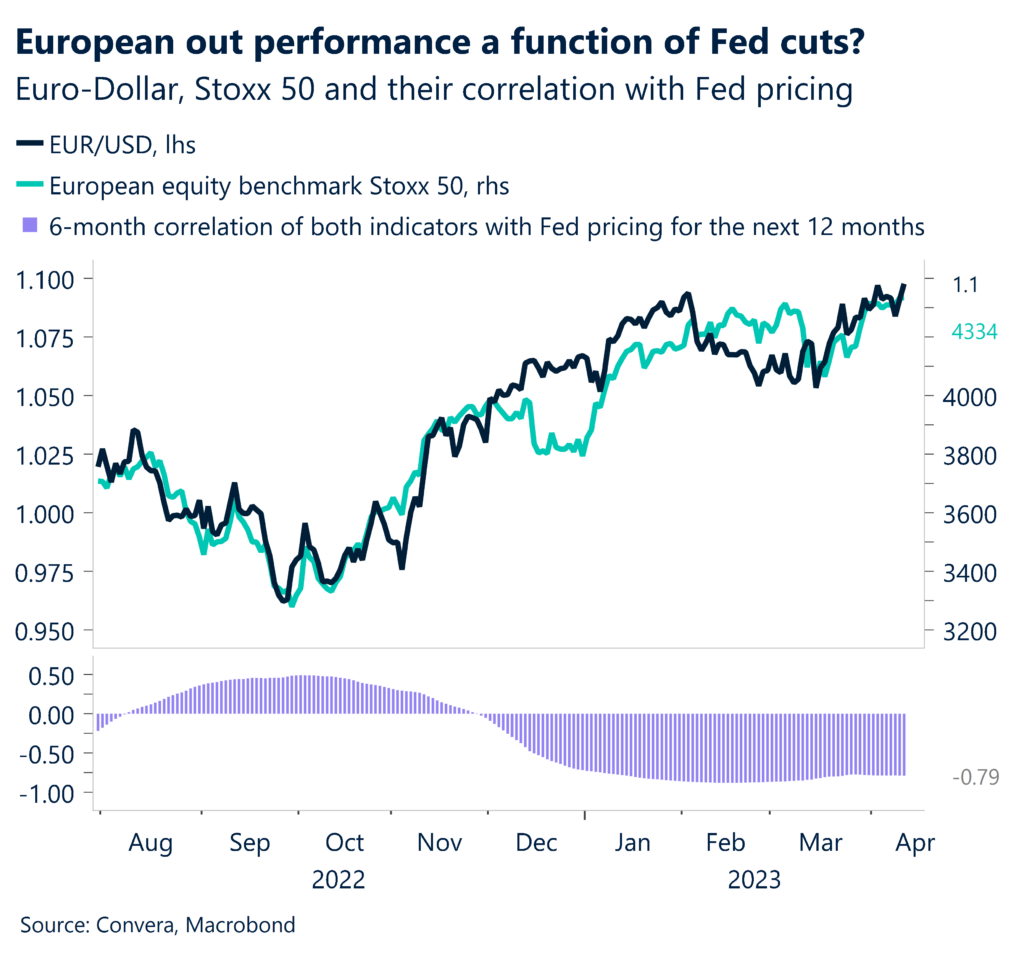

The euro brushed the $1.10 level against the US dollar yesterday, a fresh 2-month high, before modestly retracing. A close above this critical level this week could spur further upside into next week, potentially dragging GBP/EUR lower. Price action continues to be determined by global and US centric events as final German inflation data was shrugged off earlier this morning. Eurozone industrial production will be closely eyed later on though.

The failure to break above $1.10 against the US dollar may be concerning for traders betting on a stronger euro, but the softer US inflation print, increasing bets of US rates cuts, means interest rate differentials favour another leg higher in EUR/USD. It’s just a matter of timing. The common currency has climbed for seven weeks in a row – its longest winning streak since late 2020 – and with inflation pressures proving more persistent in Europe relative to the US, the European Central Bank (ECB) is expected to be more hawkish than the Fed. Most economists and investors expect another two hikes by the ECB this year before the cycle of monetary tightening comes to an end. This largely depends on the development of core inflation, which has been creeping higher even as the headline number retreats.

In the short-term, today’s Eurozone industrial production numbers will reveal whether new orders continue to suffer, leading to a continuation of the current trend of broad stagnation as the best bet for the months ahead. This could be a headwind for the euro today, but on the flipside, a brighter environment for industry could send help the euro hold above $1.10.

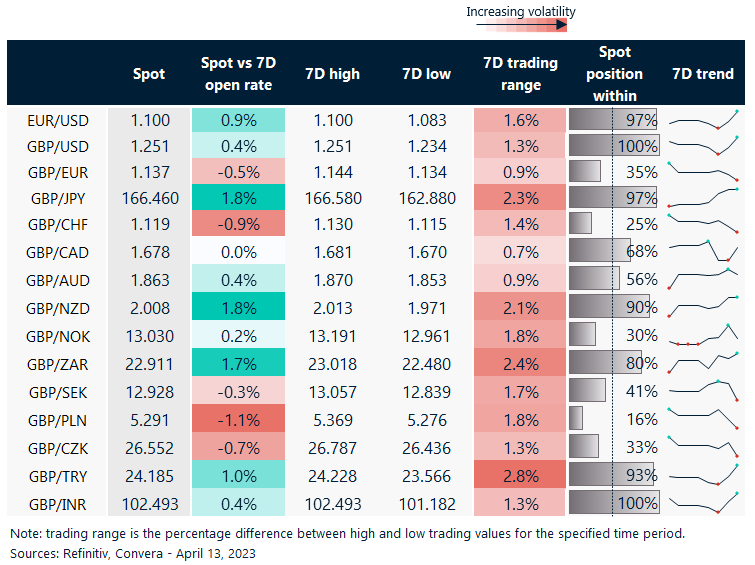

GBP/JPY up nearly 2% in a week

Table: 7-day currency trends and trading ranges

Key global risk events

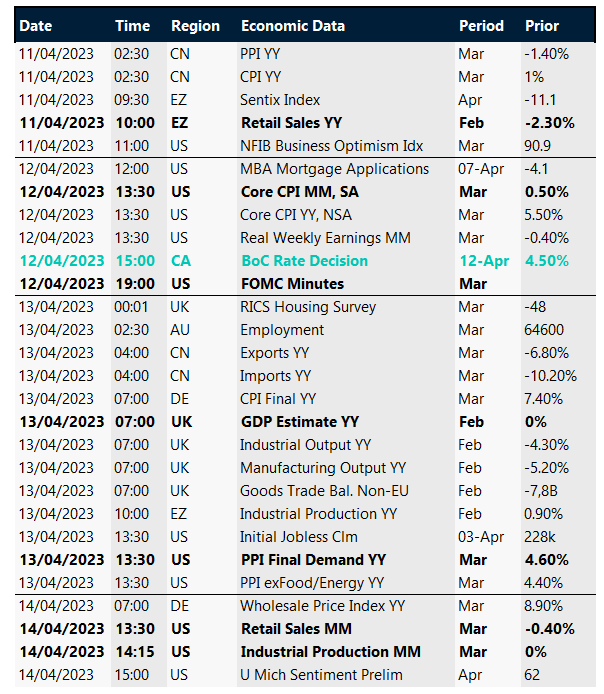

Calendar: Apr 10-14

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.