Written by Convera’s Market Insights team

Trump’s trifecta

George Vessey – Lead FX Strategist

It seems the early sense that US President-elect, Donald Trump, may be more pragmatic in power than on the campaign trail is being replaced by a more hawkish interpretation of his stance. Proposed tariffs and picks for key administration posts have begun to unnerve investors. European equity futures are pointing lower, tracking Asian benchmarks overnight, whilst the US dollar continues its onslaught – charging past 155 versus the yen and raising the risk that Japan will intervene to slow the depreciation.

As the US election outcome continues to reverberate across the globe, Republicans are projected to keep control of the House of Representatives, handing the party total control of Washington and delivering Trump a trifecta. The reaction across financial markets reflect the growing risk that Trump’s policies will prove inflationary and the US Federal Reserve (Fed) will have to delay or slow its easing cycle. Indeed, traders are now pricing in about two US rate cuts through June, against almost four seen at the start of last week. This is helping to drive the dollar higher given the rise in US yields to multi-month highs. But this positive USD bias extends beyond the US election – a reading within October’s NFIB small business survey regarding a positive outlook on the US economy rose to its highest level since November of 2020. The ongoing US exceptionalism narrative remains a bullish driver of the buck.

The next volatility catalyst will be the US inflation print due today. Core inflation is expected to have stagnated at 3.3% for a second month in a row in October, after bottoming at 3.2% in July. The Fed will pay attention to this first sign of a potential turnaround of the otherwise positive disinflation trend of the past 12 months or so.

European underperformance continues

Boris Kovacevic – Global Macro Strategist

European assets continue to be dragged lower by political uncertainty from abroad and at home as economic surveys start painting a subdued growth outlook once again. Investor confidence in Germany fell more than expected in November as participants weighed the risks of a collapsing coalition and Trump’s win of the White House.

Before the US election, around 44% of German industrial companies said that Trump would negatively impact their business. However, only around 4% had undertaken steps to mitigate risks, according to the Ifo Institute. Political risks are exacerbating a broad lack of demand as around half of German businesses report insufficient orders. Yesterday’s ZEW survey added pessimism to the already bleak picture as the current economic situation sub-index fell to the lowest level since the depth of the pandemic in early 2020. At -91.4 points, it is currently sitting at the fifth lowest level since 2005.

EUR/USD continued its descent for a third day in a row and is just holding on to the $1.06 handle. The currency pair is closing in on its yearly low as European equities continue to underperform their US peers. The Stoxx 600 year-to-date gain dropped below 5% for just the second time since April, while the S&P 500 remains around 25% higher than at the beginning of the year. This underperformance of European assets will weigh on sentiment as investors consider if US equity benchmarks might dominate the rest of the world for yet another 5-year period.

Pound under the pump

George Vessey – Lead FX Strategist

After breaking south of key support levels, including long-term moving averages, the British pound is consolidating at multi-month lows against the US dollar. The US dollar has enjoyed a fresh wave of demand this week, helped by president-elect Donald Trump’s appointments of trade ‘hawks’ to his top team that reinforces his commitment to significant import tariffs. But the pro-cyclical pound has come under broad-based selling pressure amidst question marks over the Bank of England’s (BoE) policy easing pace.

Despite the stronger-than-expected wage growth figures from the UK yesterday, there was a big surprise jump in the UK unemployment rate, which weighed on sterling. Given how far the jobs market has cooled, the BoE should be looking at cutting rates back to neutral level. However, the risk of inflation rebounding, aggravated by Trump’s victory, complicates the situation. The BoE has signalled a gradual reduction of interest rates, and as it stands, overnight index swaps show investors are pricing in 63 basis points of cuts from the BoE by December 2025. This is less than the 70 basis points priced in for the Fed. Given the economic situation in both countries, and the potential for higher inflation under a Trump presidency, that may prove to be a mismatch. Still, the 2-year UK-US real yield spread still favours sterling edging higher in the very near term. With GBP/USD trading close to oversold territory on the daily chart, downside pressure might start to cool from here.

Elsewhere, the pound is clutching onto the €1.20 mark versus the euro. The UK is likely less exposed to direct tariff risks than the Eurozone given its trade deficit in goods with the US.. Moreover, the UK’s healthier cyclical dynamics and fiscal-monetary policy mix are more bullish for sterling versus the euro too. As such, this arguably opens up a positive tailwind for GBP/EUR going into 2025.

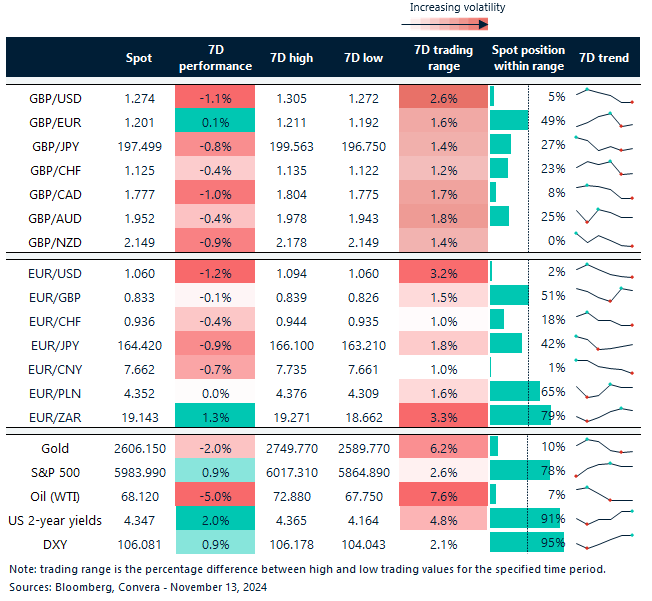

US yields and USD dominate post election

Table: 7-day currency trends and trading ranges

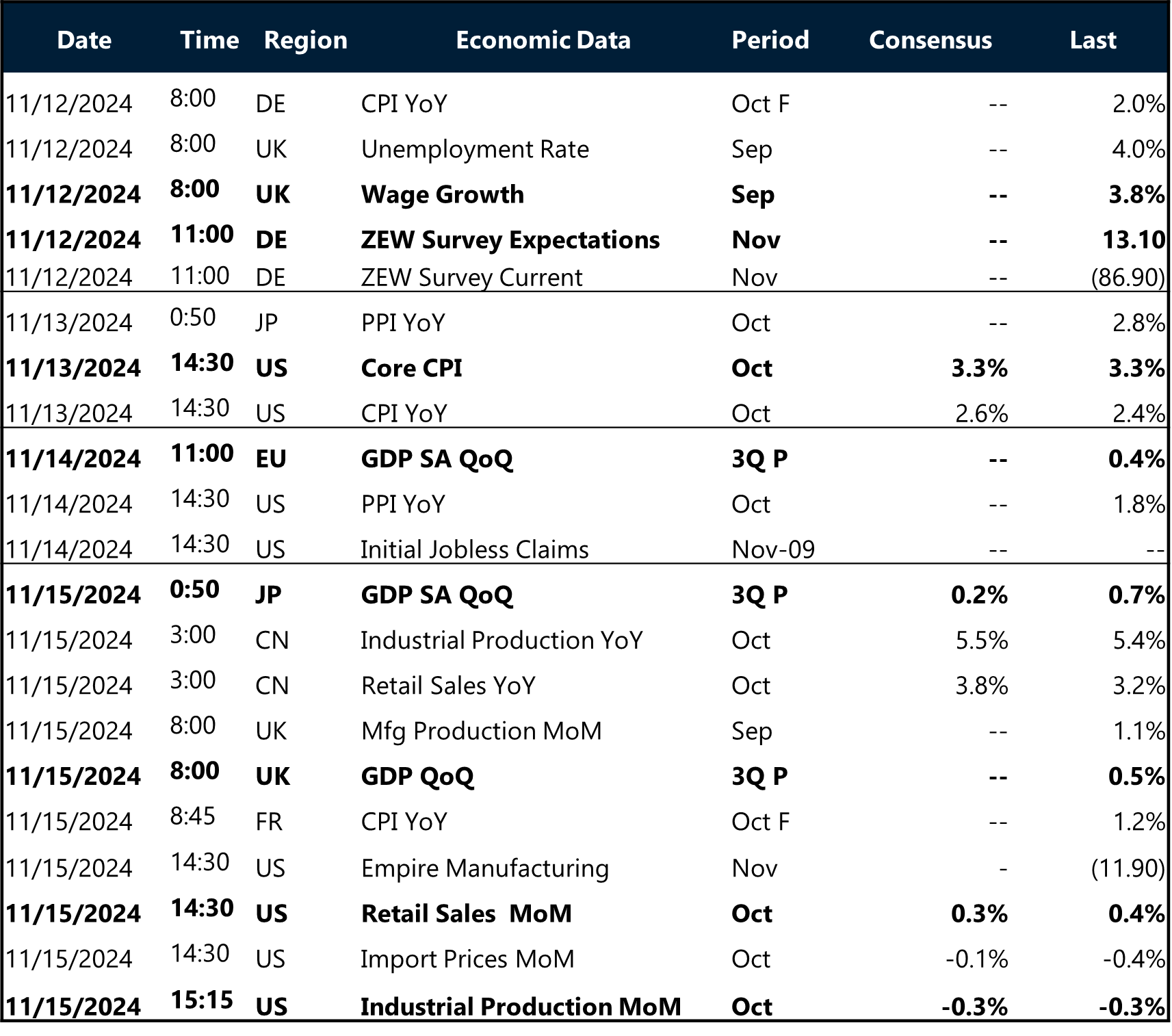

Key global risk events

Calendar: November 11-15

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.