Written by Convera’s Market Insights team

Ackman puts the lid on US yield surge

Boris Kovacevic – Global Macro Strategist

The 10-year government bond yield in the US has been front and center in recent weeks and has played a key role in determining the daily sentiment on global financial markets. Yesterday was no exception, which the volatility in the fixed income space once again making headlines.

Just hours after the 10-year yield reached the 5% level for the first time since 2007, Pershing Square’s billionaire hedge fund manager Bill Ackman’s tweet about closing his large short bond position triggered a yield collapse. Interest rates on the US 10-year government bond at one point fell by 20 basis points from 5.02% to 4.82%. This rally in long dated bonds eclipsed the flight to safety seen on the first trading day following the Hamas attack on Israel two weeks ago and was the largest since the collapse of the Silicon Valley Bank back in March.

The US dollar softened in yesterday’s trading against a basket of currencies, mirroring the dop in Treasury yields. Macro data will start to play an important role once again this week, beginning with today’s PMI numbers, followed by Thursday’s GDP print and Friday’s PCE inflation report. The consensus expects the US economy to have doubled its pace of growth from Q2 (2.1%) to Q3 (4.3%) on an annualized basis. Core inflation is expected to fall from 3.9% to 3.7%, continuing its slow but steady descent.

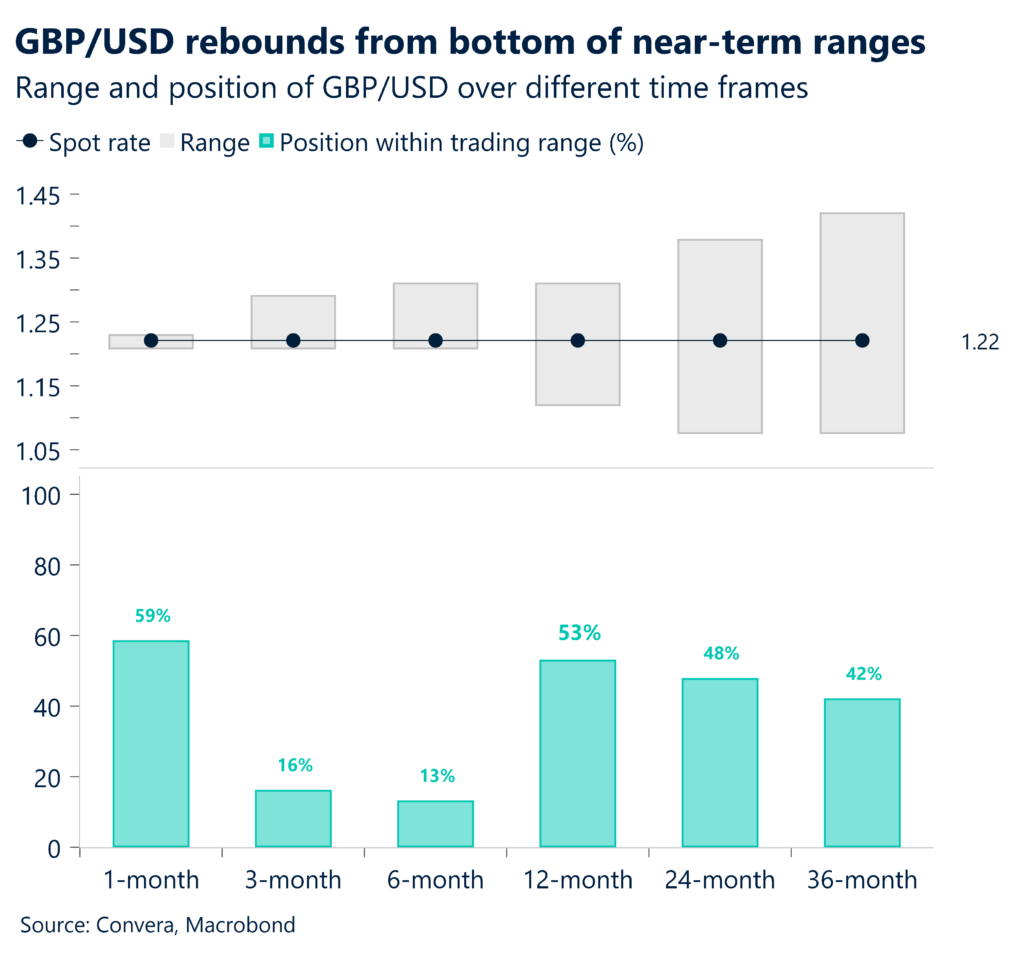

Pound surrenders early gains after pessimistic PMIs

George Vessey – Lead FX Strategist

The pound recorded its biggest daily rise against the US dollar since mid-July yesterday as the risk profile turned cheery and yields retreated sharply in the afternoon. GBP/USD looked poised to test fresh monthly highs after breaking above a downward sloping trendline that’s been in place since its 2023 peak of $1.3140 but gave up early gains following the release of the key activity data.

The pound has shrugged off the delayed UK jobs data this morning. The so-called adjusted experimental unemployment rate in the UK rose to 4.2% in the three months leading up to August 2023, up from 4.0% in the March to May period, whilst the inactivity rate continues to inch higher. However, the pound surrendered its recent gains as October’s UK flash services PMI remained unchanged at 49.2, undershooting the 49.5 consensus forecast. The PMIs have been increasingly important to the currency market, which is becoming more sensitive to relative economic growth rates due to their influence on how long interest rates will remain high. A print of below 50, which marks a contraction in activity, puts a damper on hawks advocating another Bank of England (BoE) interest rate rise, as the services sector is the dominant segment of the UK economy.

It should be noted that earlier this month, sterling strengthened after September’s UK services PMI was upwardly revised to 49.3 from a 47.2 flash estimate – an estimate which might have swayed one or more of the five BoE members who voted to keep rates unchanged last month.

Euro breaks above $1.06 on lower oil and US yields

Ruta Prieskienyte – FX Strategist

The fruitful diplomatic developments in the Israel-Hamas conflict on Monday managed to relieve price pressures on crude oil to an extent, providing a mild reprieve for the euro. The common currency benefited from the sharp negative repricing in US yields as well and closed the day 0.7% higher, hitting a fresh 1-month high at $1.0670. Yesterday’s surge ended the 12-week downward trend that had lasted from July, and which saw the currency pair fall by 6%.

The ECB meeting this Thursday should be a relatively mundane affair. The central bank is expected to hold its deposit and refinancing rates at 4.0% and 4.5%, respectively, and repeat the message that the terminal rate has been reached. The news on the inflation front has been generally positive, pointing to continued disinflation and a weakening economy suggests the need for further tightening is limited. The main question will now be regarding the magnitude and timing of ECB rate cuts. The markets are fully discounting a 25bps rate cut for July 2024. Oxford Economics is expecting rate cuts to come a touch sooner, while some hawkish ECB members voiced reservations about even talking about easing policy. Market participants will also focus on any discussion surrounding the end of PEPP reinvestments being brought forward from the end of 2024. However, with recent sharp moves higher in BTP yields should put such conversations on hold, at least until spring 2024.

Ahead of the decision, we will be closely monitoring PMIs and the Q3 bank lending survey to give better clues on the bloc’s economic health and financial tightening conditions. The takeaway from the ECB meeting might just be that the bar for further rate hikes remains high but even higher for rate cuts. This implies a continued policy pause over the coming meetings.

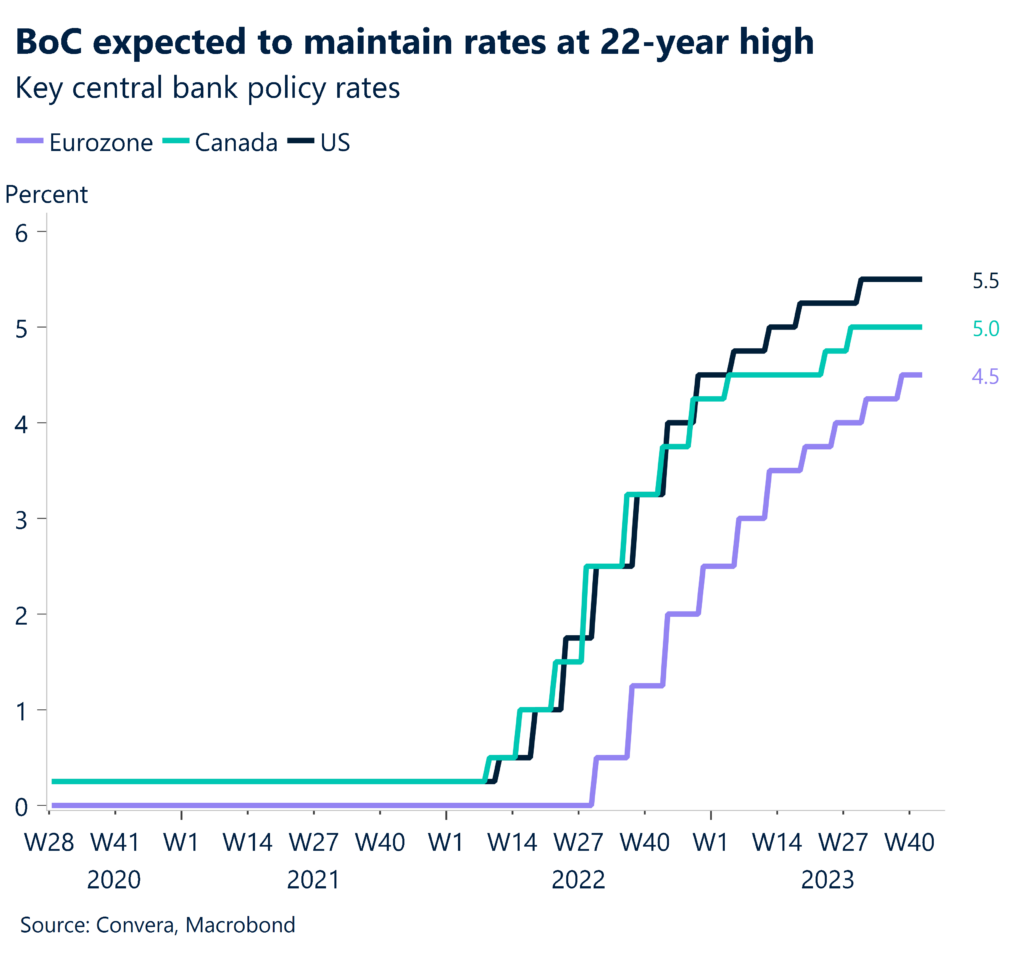

CAD holds steady in anticipation for BoC

Ruta Prieskienyte – FX Strategist

Despite a slight recovery in WTI crude above $86 per barrel on Tuesday, the Canadian dollar has yet to capitalise on the support provided by a rebound in oil prices, which it usually has a positive correlation to as a net energy exporter. USD/CAD continues to trade in a tight band of 1.36-1.37, which it has been stuck in since 13th October, ahead of the Bank of Canada rate decision this week.

However, BoC meeting tomorrow is set to be more of a formality, rather than a market driving event. The recently released CPI data for September confirmed a continuing disinflationary trend and cooling core inflation, thus reaffirming that BoC is well on track to restore price stability. The markets are now pricing an 87.5% probability that BoC will leave its benchmark rate on hold at a 22-year high of 5%. The focus will naturally turn to any forward guidance from BoC officials on Canadian growth and the prospects of rate cuts, though on the latter it seems unlikely that explicit commentary will be forthcoming. While there is still an interest in keeping a higher-for-longer narrative alive, the markets may start to shed some doubts on it. Despite strong labour market, the Canadian economy is beginning to buckle under tight monetary policy, with Oxford Economics forecasting a 0.3% q/q contraction in Q3. Mounting evidence of growing economic strain might prompt BoC to consider pivoting earlier than expected, which would not be beneficial for CAD via interest rate differential compared to US.

Given this and an otherwise light data calendar this week, the Canadian dollar is unlikely to pick up much support from domestic developments. The exchange rate movements will once again be driven by events in the Middle East, oil prices and US-centric narrative.

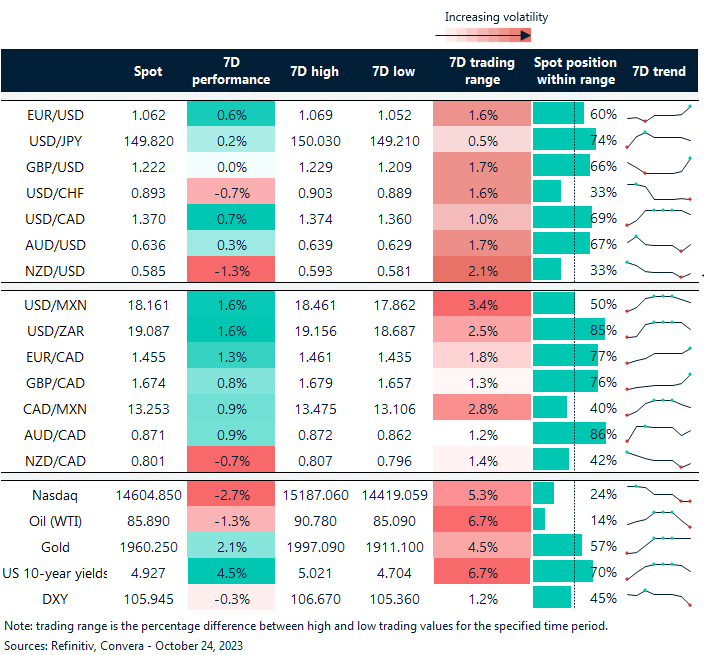

GBP & EUR shine on risk appetite rebound

Table: 7-day currency trends and trading ranges

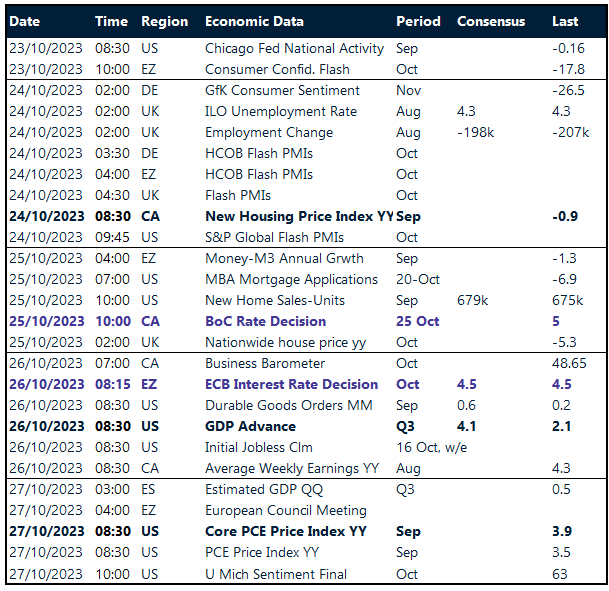

Key global risk events

Calendar: October 23-27

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.