USD: Dollar near 1-month lows

US and European equity futures advanced on Friday, with investors positioning ahead of the release of the Fed’s preferred inflation gauge. The US dollar index remains close to its weakest level since late October, as markets lean heavily into expectations of a Fed rate cut next week. Current pricing implies nearly a 90% probability of such a move, driven by mounting evidence of labour market weakness.

November’s Challenger survey showed layoffs rising over 71k, the highest for that month since 2022, pushing the year‑to‑date total to 1.1mln, the largest since 2020. This followed the ADP data earlier this week which showed a 32k decline in private payrolls, reinforcing concerns about slowing hiring momentum.

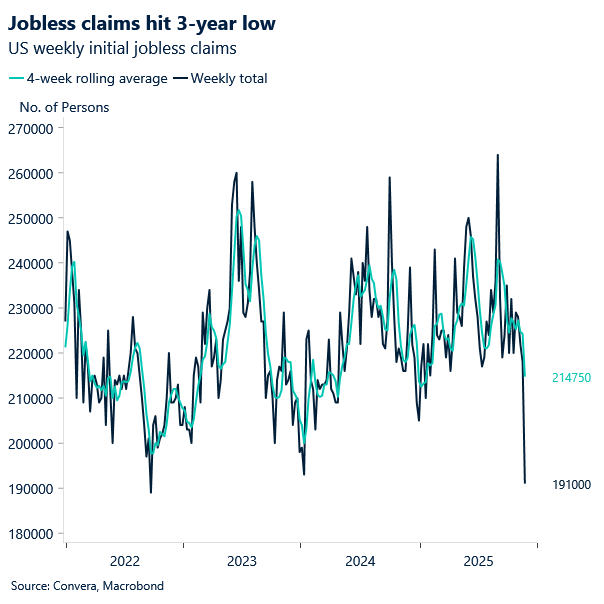

We did see initial jobless claims fell to 191k, the lowest in more than three years, though the Thanksgiving period likely distorted the figures. Even so, the four‑week average remains at its lowest this year. Investors appear to be discounting the claims data though, focusing instead on the broader trend of rising layoffs and weaker hiring intentions. That explains why the knee‑jerk reaction higher in US yields and the dollar quickly faded, with traders reverting to a dovish bias.

Still, we view the near‑90% probability of a December Fed cut as overstated given key data pieces are missing. The Fed may well deliver a cut, but packaged in hawkish messaging as seen in September and October. Such a move would temper expectations of aggressive easing and could ultimately prove dollar‑positive, especially if markets have over‑extended in pricing downside risks.

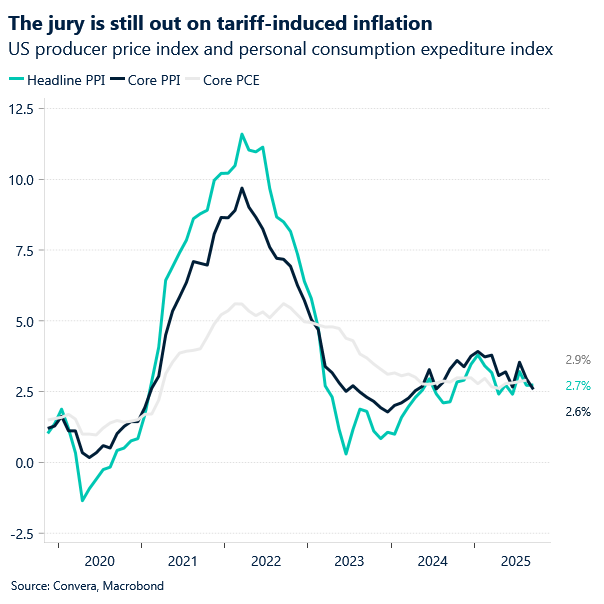

All eyes today are on the Fed’s preferred inflation gauge, the PCE price index, alongside the core measure that strips out food and energy. Consensus points to a third consecutive 0.2% monthly rise in the core index, which would leave the annual rate just under 3%. That outcome would reinforce the narrative of inflation that is no longer accelerating but remains stubbornly above target.

EUR: Euro rallies, but politics cloud the path

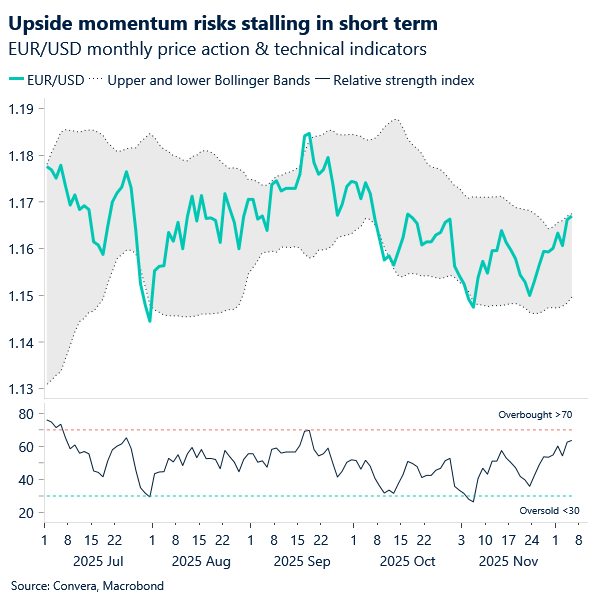

EUR/USD has staged a decisive bullish move, climbing above several key technical levels and holding above its 200‑day moving average. Options markets reflect this momentum, with positioning gauges at their most constructive in almost three weeks. The setup points to further upside potential, though a more stable risk environment is likely needed before the dollar weakens more convincingly against risk‑sensitive currencies. Sustainability will hinge on cohesive dovish messaging from the Fed, set against a still‑fractured US data backdrop.

Geopolitical developments remain a limiting factor. Witkoff’s visit to Moscow yielded no breakthrough, capping euro gains in the near term. Meanwhile, political risk is rising across Europe. In France, budget approval remains uncertain, while in Germany Chancellor Merz faces a rebellion within his party over a pension bill. A failure to pass the legislation could see the SPD withdraw from the coalition, raising the prospect of fresh elections. Such instability would jeopardize the rollout of Germany’s stimulus package and undermine efforts to restore competitiveness in Europe’s largest economy.

For traders, the risk is that optimism around the euro collides with renewed policy uncertainty. A weak German recovery, fiscal gridlock in France, and the possibility of a soft 2028 inflation projection from the ECB on December 18 could shift the conversation back toward rate cuts.

That leaves EUR/USD vulnerable to setbacks if political instability and dovish ECB signals converge, even as dollar softness provides tactical support.

GBP: Sterling bid, BoE dovishness debated

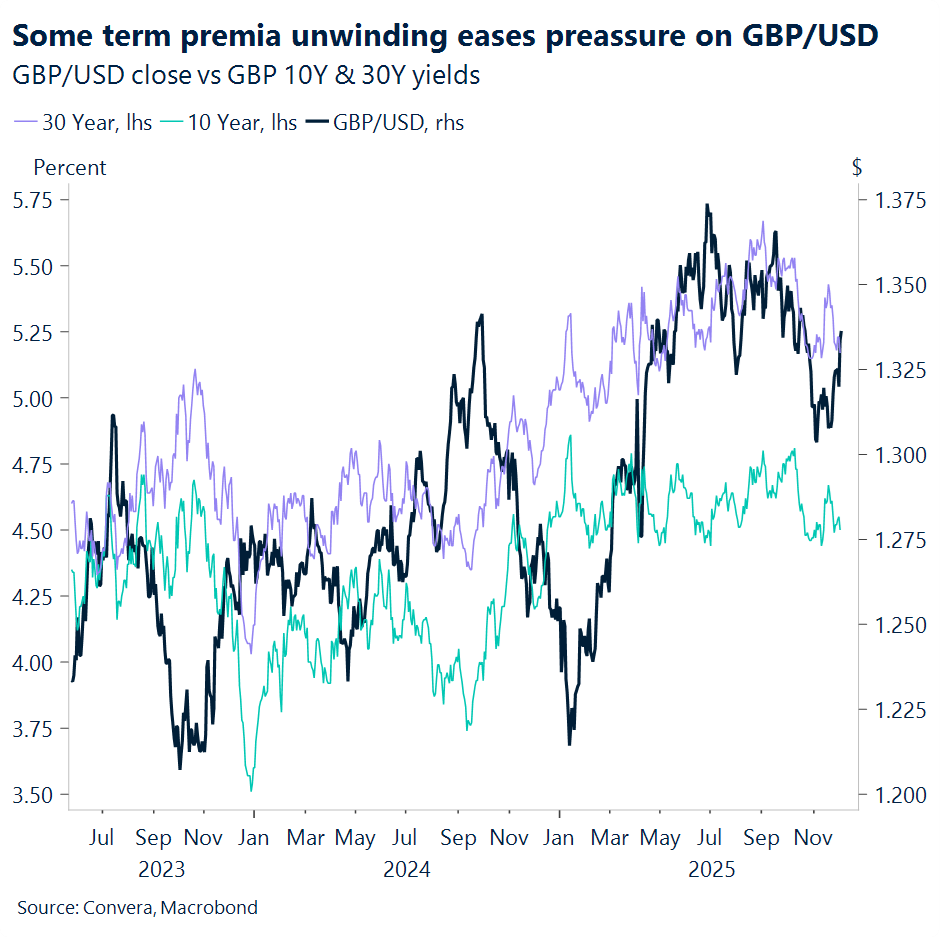

Sterling stays bid as broad‑based bearishness flattens, with gilt curve pressure easing post‑budget. This dynamic has granted BoE expectations greater influence over sterling’s price action, though the impact remains muted for now, with almost a full cut already priced in and markets unconvinced about how dovish the BoE can ultimately turn entering 2026.

The MPC stressed its data‑dependent approach, noting that a single month of softer inflation would not suffice to embed a more dovish policy path. A (second) lower‑than‑expected inflation print during the week of the meeting itself – 15 December – therefore could go a long way in shaping the Bank’s dovish bias, and push sterling lower.

Yesterday GBP/USD reached a one‑month high near 1.34, capped by the 100‑day moving average at 1.3369. The pair has technically disengaged from its downtrend since mid‑September, rebounding from seven‑month lows at 1.3010 in early November. Upside momentum has accelerated in recent weeks, with the pair still broadly discounted relative to fair value. With risk premium still elevated, room for upside in the inter‑key zones remains intact – even absent a decisive bullish catalyst.

With little UK data due today, focus shifts to the US PCE report. A notable miss would strengthen easing bets for the Fed next week and could see GBP/USD break through the 100-day moving average resistance level.

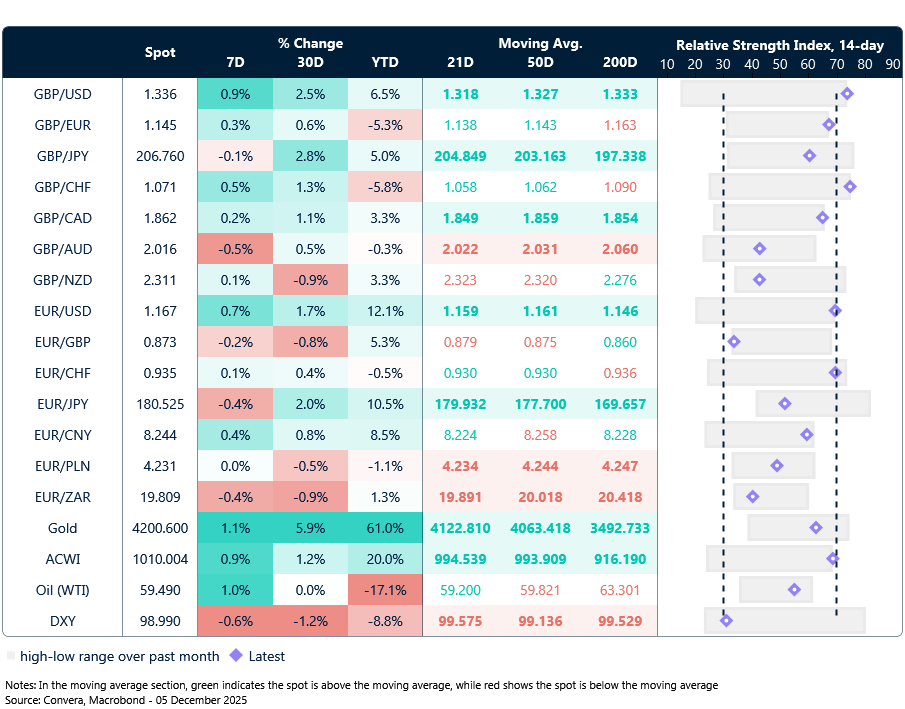

Market snapshot

Table: Currency trends, trading ranges and technical indicators

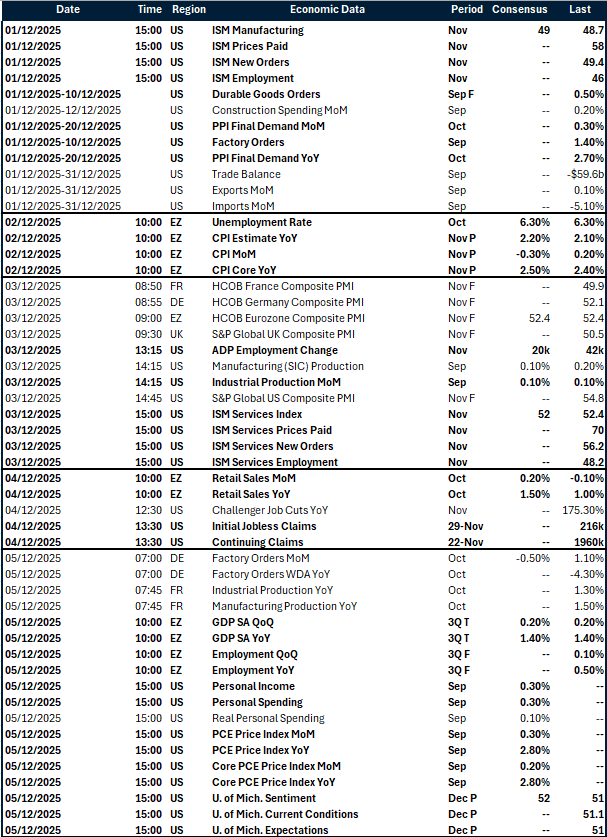

Key global risk events

Calendar: December 1-5

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.