USD: Signals beyond Venezuela

US actions in Venezuela are best read as a geopolitical signal rather than a market event, with negligible implications for oil or FX. Venezuela supplies barely 1% of global oil output, produces heavy crude the market is already well stocked with, and lacks the infrastructure or investment environment to shift supply in any meaningful timeframe. That keeps the energy channel muted and leaves the USD anchored to its usual macro drivers (see next section). The real relevance lies in what the move reveals about Washington’s risk appetite: a willingness to absorb geopolitical risk and deploy a wider range of tactics than previous administrations.

That behavioural shift inevitably sharpens market attention on other flashpoints. It could embolden tougher rhetoric or intervention threats toward Iran and has already reignited tensions over Greenland with Denmark and the EU. But a genuinely systemic risk sits in China–Taiwan, where any escalation would threaten semiconductor supply chains and global growth. In that sense, Venezuela matters not because of its barrels, but because it hints at a world where the boundaries of acceptable state behaviour feel looser, and the stakes at the major fault lines are far higher.

Digesting the US data deluge

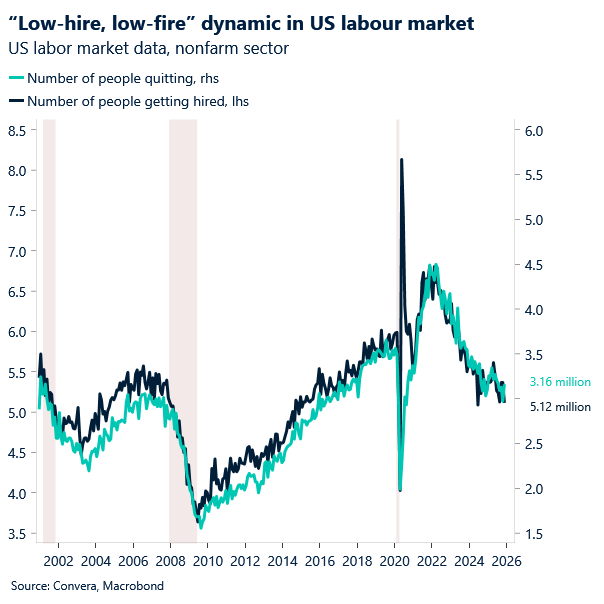

Shifting attention back to the economic data, we had a barrage from the US yesterday. ADP private‑sector payrolls undershot expectations at 41k versus 50k, while JOLTs showed a sharp drop in job openings — clear signs of cooling labour demand. But the layoff rate edged lower and the quit rate ticked up, reinforcing the “low‑hire, low‑fire” dynamic running through the labour market. All eyes now turn to Friday’s NFP, where consensus looks for 66k jobs and a dip in unemployment to 4.5%, a print that will help determine whether the Fed sees this slowdown as a controlled glide path or something requiring additional easing.

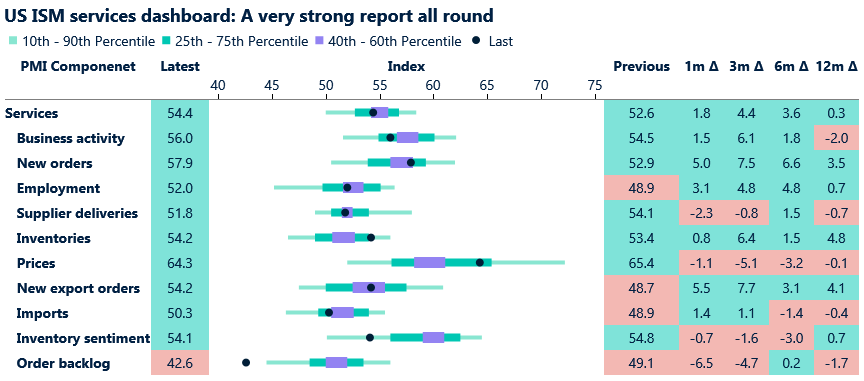

Activity data told a different story. The ISM services index jumped to a 14‑month high, with business activity, employment and new orders all firmly in expansion territory. The only soft spot was backlogs, while the elevated prices‑paid component suggests inflation pressures remain sticky in the sector. On its own, the report argues the Fed can stay patient with rate cuts.

Financial markets reacted defensively. Treasuries rallied across the curve and equities sold off, though the S&P 500 and Nasdaq Composite have still respectively tallied their best four-day starts to a new year since 2023 and 2019, up by 1.1% and 1.5%.

The dollar was broadly steady but remains firmer on the week, and positioning leaves room for more upside. Traders built up sizeable, short‑USD exposure into year‑end; if the dollar continues to grind higher and those shorts are forced to cover, positioning flows could add an extra tailwind.

EUR: Rate spread widens, jobs data holds the trigger

Yesterday eurozone inflation eased to 2% in December from 2.1% in November, driven primarily by lower energy prices. Meanwhile, sticky services inflation, which slipped to 3.4% from 3.5%, was largely the result of easing wage growth. The data is unlikely to prompt much reaction among ECB members for now, especially after the upward revisions to inflation forecasts in the December staff projections. That said, a move below the 2% target later in the year, driven by such factors as a stronger euro, lower energy prices, and easing wage growth, would strengthen the case for further easing in 2026.

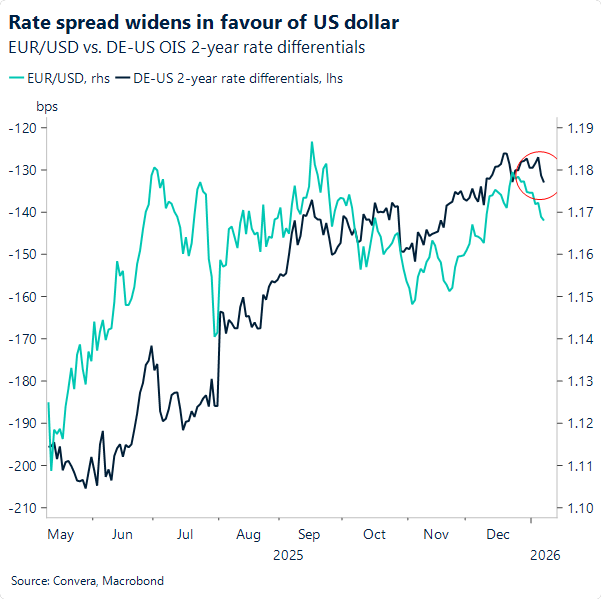

On the US side, the data flow was broadly positive, so all-in-all rate differentials widened in favour of the US dollar and caused EUR/USD to nudge lower. The US jobs report on Friday will offer clearer evidence on the state of the US labour market, either challenging or confirming the not‑so‑soft picture suggested by yesterday’s JOLTS data. The outcome may crystallise the widening rate spread, adding more meaningful bearish pressure on EUR/USD.

Technically, the pair has failed to reclaim the $1.17 zone since Tuesday. Repeated topside rejections point to reluctant buying flows, raising the risk of a deeper pullback if Friday’s US data reinforces the widening rate spread.

GBP: Softer amid risk off tone

Sterling has pulled back from over 3-month highs versus the US dollar and euro as global risk appetite stalls cools, with geopolitical tensions lifting safe‑haven demand. That dynamic leaves the pound firmer against higher‑beta peers like the Scandis and Antipodeans.

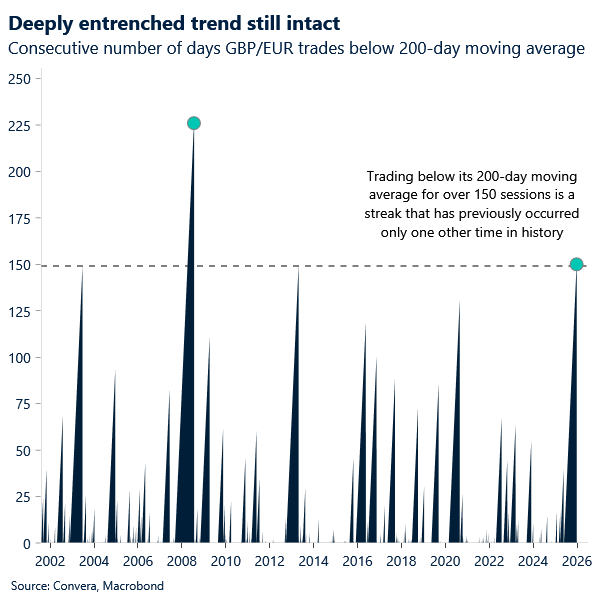

We had flagged that GBP/EUR’s rally looked stretched: the 200‑day moving average remains a clear resistance line, and the failure to break higher leaves the cross vulnerable to renewed downside risks. Sterling’s run below the 200‑day moving average has now passed 150 sessions, a feat matched only once in the historical record. Staying below it for that long shows the market has been consistently unwilling to price a sustained recovery. Moreover, the Relative Strength Index (RSI) hit 70, a level that typically marks overbought territory. Hence, the near‑term pullback is no surprise.

With no UK‑specific catalysts on the slate this week, sterling is largely trading off the global backdrop. Next week’s GDP release gives markets something domestic to chew on, but the real test comes the following week with labour market, inflation and PMI data — the first meaningful read‑across for the Bank of England’s February decision. Those prints will determine whether policymakers feel compelled to deliver another cut.

If the data softens, GBP/EUR likely drifts lower as rate‑cut expectations firm. But if inflation proves sticky, the recent recovery has room to extend into February.

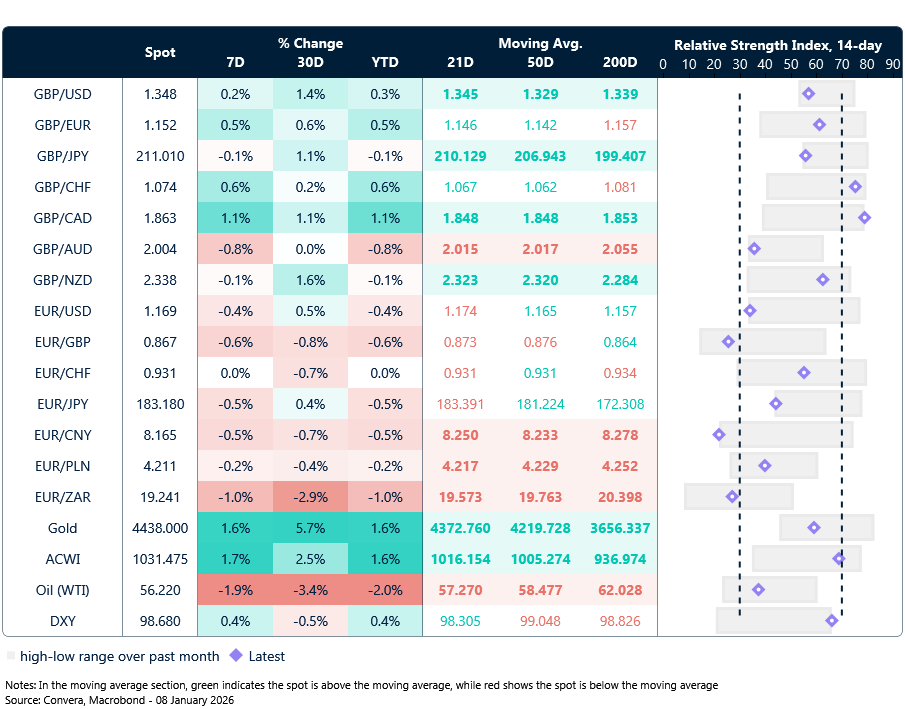

Market snapshot

Table: Currency trends, trading ranges & technical indicators

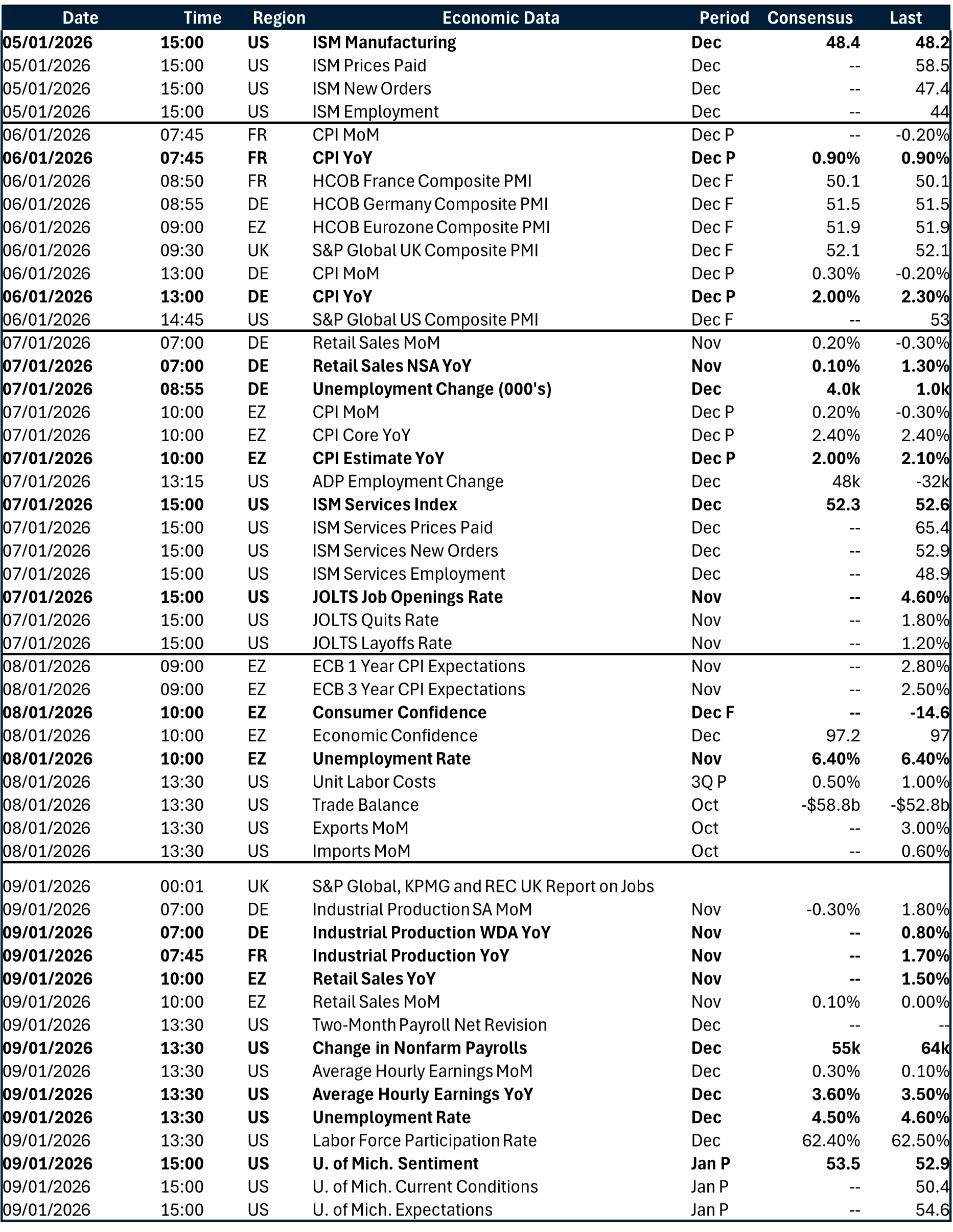

Key global risk events

Calendar: January 05-09

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.