Written by Convera’s Market Insights team

Yields and USD slide as retail sales slump

George Vessey – Lead FX Strategist

After beating estimates for six straight months, US retail sales declined in January by the most in nearly a year. Separate data showed US factory production fell for the first time in three months in January and a decline in US jobless claims. Treasuries climbed, yields fell, as the report soothed investors’ nerves about an overheated consumer segment. The US dollar suffered its second biggest daily decline of the month but is still on track for a weekly gain.

Recent economic data from the US exposes this dichotomy of weakening retail sales yet a strong labour market. Overall, we still expect slower growth as high borrowing costs, tight credit conditions and reduced support from pandemic-era accrued savings create a more challenging environment. That said, macro volatility is keeping market participants on their toes regarding the timing and pace of expected interest rate cuts by the Federal Reserve (Fed). After yesterday’s data, Fed swaps started pricing more easing in 2024 and fully implying a rate reduction in June. A hot US inflation print earlier this week led markets to trim bets on a Fed cut before June and the amount of easing expected for this year to fewer than four quarter-point rate cuts from almost five a week ago.

There appears to be a growing sensitivity to data misses, higher or lower, across financial markets because of how this plays into policymakers’ decisions. The divergence in policy rates, as central banks start cutting at different times and at different paces, could reignite cross-asset volatility, especially in the sleepy FX market.

UK retail sales beat, Tories lose, pound mixed

George Vessey – Lead FX Strategist

After yesterday’s data revealed the UK slipped into a technical recession at the end of last year, today’s upbeat retail sales data shows why the Bank of England (BoE) was unperturbed about the GDP figures. UK retail sales posted the biggest monthly rise in almost three years, increasing hopes that the economy has stabilised already. The pound’s reaction was modestly positive, but it remains mixed across the board on the week.

The volume of goods sold in stores and online in the UK gained 3.4% in January, the most since April 2021 when the economy was emerging from lockdown. This was more than double the 1.5% expected and also adds to recent survey evidence pointing to a pickup in economic momentum as the worst cost-of-living crisis in a generation eases. UK Prime Minister Rishi Sunak will welcome this good news following yesterday’s recession stories hitting the headlines. Problems for the Conservative Party have been mounting for some time, but hopes of staying in power this year are really dwindling after the opposition Labour Party overturned significant Tory majorities to win two parliamentary seats overnight.

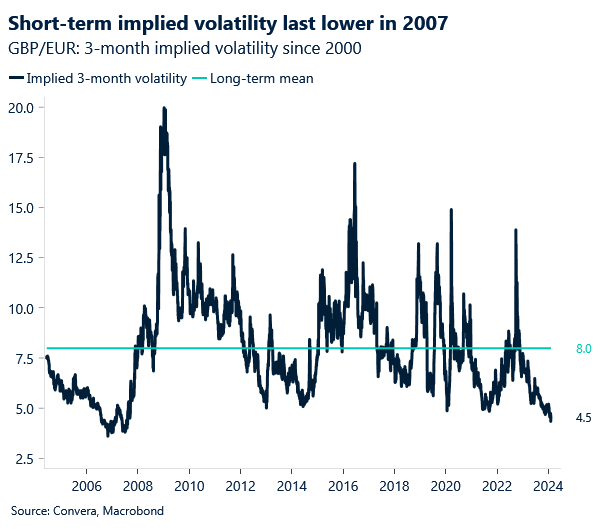

The reaction in financial markets and UK assets in particular has been relatively muted to all this though. Not a big surprise for GBP/EUR, which has seen implied volatility drop to its lowest level since 2007. The currency pair is up slightly to reclaim €1.17 and whilst volatility remains low, we should see the pound benefit from carry trades. Meanwhile. GBP/USD still hangs around the $1.26 mark after a modest knee-jerk bump higher. The pound is still primed for a weekly loss against the dollar after this week’s big data releases though, and this would mark its fifth weekly decline out of seven.

George Vessey – Lead FX Strategist

EUR/USD rose back into the higher realms of the $1.07-$1.08 range of this month as European Central Bank (ECB) policymakers continued to push back against rate cuts. Money markets are still pricing in a 54% probability of an April cut and 112 basis points of cuts by year-end, but this is down from 150 basis points just weeks ago.

The current disinflationary process in Europe is expected to continue, but the Governing Council needs to be confident that it will lead sustainably to its 2% target. One of the reasons the ECB keeps pushing back on rate cut bets, is the concern that relatively quick nominal wage growth will push up inflation as workers look to recoup incomes lost to quick price growth. We have also been touting the importance of wage growth as an increasingly significant driver of inflation dynamics this year and that wage divergence could be the driving force behind policy divergence as a result. While the US is seeing wages fall in line with inflation, Europe and the UK are seeing a different story, which may prove a greater risk to central banks and their fight against inflation.

Meanwhile this week though, data confirmed the Eurozone economy’s stagnation continued in the final quarter of 2023, meaning that the bloc has just avoided a recession, but has not shown any sign of life over the last year, contracting or growing by a slight 0.1% since the beginning of 2023. It is this growth divergence that has also played a role in currency trends, with the USD most attractive and EUR struggling. For now, we expect this trend to continue and see upside limited above $1.08 in the short-term.

Pound mixed across the board

Table: 7-day currency trends and trading ranges

Key global risk events

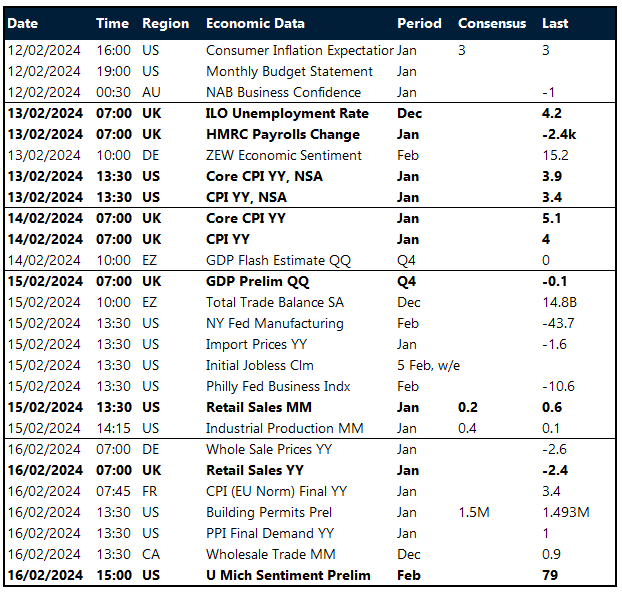

Calendar: February 12-16

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.