US macro data falls short

Yesterday’s session presented us with some data disappointments that had various impacts on markets. Weaker than expected inflation numbers out of China confirmed the view that the reopening of the second-largest economy has been stalling. With jobs and inflation data in the US also falling short of expectation, markets turned risk-off. Capital flight into safe havens remained contained, however, and is already dissipating in today’s early trading.

Factory gate inflation in the US slowed for the 10th consecutive month, with producer prices only rising by 2.3% during the last twelve months. This stands in stark contrast with the dynamic at the end of last year, when producer inflation reached a multi-decade high, topping 11%. The overall trend in the US has been a disinflationary one with consumer, wholesale, import and producer price growth normalising. In combination with the parallel rise in initial weekly jobless claims to 264 thousand, it seems that the Federal Reserve (Fed) has made a lot of progress in the fight against inflation.

The probability of a Fed rate hike at the June meeting did rise in yesterday’s session from 0% to 11% even against the backdrop of weaker macro data. One reason for the upward revision might be found in the geopolitical space. US National Security Adviser Jake Sullivan met with China’s top diplomat Wang Yi in an attempt to soften the tone between both countries. The US dollar index recorded the best daily session since the middle of March but has given up around 1/3 of yesterday’s gains in today’s early trading.

Pound drops after BoE hike again

The Bank of England (BoE) raised its key interest rate by 25 basis points to 4.5% yesterday, marking the twelfth consecutive rate increase, in line with market expectations. A UK recession is no longer expected, and the BoE upgraded its growth and inflation forecasts. However, the pound, as it typically has done in this tightening cycle, took a tumble after the policy decision, with GBP/USD falling back to $1.25 and GBP/EUR under €1.15.

After 440 basis points of rate hikes, borrowing costs are now at fresh highs not seen since 2008, as the BoE continues to battle double-digit inflation, with services inflation proving particularly stubborn. Two of the nine-member Monetary Policy Committee voted for no change once again, but the majority of the panel said repeated upside surprises in wage growth and economic activity have added to price pressures and required further monetary tightening. The central bank sees inflation falling to 5.1% in the fourth quarter of 2023, compared to 3.9% in the February forecast and to meet the 2% target by late 2024. Moreover, BoE officials delivered the biggest upgrade to growth projections on record, erasing a recession previously forecast. There wasn’t a big enough hawkish shift to support sterling further though, and as investors also digested soft China price data as well as resurgent US regional bank fears, the pound was sold off in favour of safe haven currencies, with GBP/JPY falling around 1% yesterday.

This morning, UK GDP data showed the British economy expanded 0.1% in the first quarter, the same as in the previous period, and matching market forecasts, despite shrinking by 0.2% in March. Although interest rate differentials are a key driver in currency markets, interest rate increases will also drag on economic growth, and this weighed on sterling yesterday too.

Growth fears starting to weigh on euro

The euro has slumped from 1-year highs against the US dollar to around the lowest level in three weeks as investors refocus on the weakening global growth outlook following China demand concerns, banking sector worries, and uncertainty over the US debt ceiling. Domestically, European data has also surprised to the downside, which has likely restricted the euro’s ability to stretch higher.

The economic surprise differential (EZ-US) has fallen to the lowest level since the middle of last year, and although EUR/USD has decoupled from its correlation with this differential, the gap could soon close, especially if risk aversion continues to prompt demand for safe havens like the dollar. The euro has recently been supported by US inflation slowing faster than expected, leading to hopes of a smaller interest rate gap between the US and the Eurozone and for now, the market is still pricing one to two more European Central Bank hikes by September. However, from there on, the chances for rate cuts are increasing alongside US markets as global growth concerns gain more attention. The latest spike in dollar demand hasn’t been strong enough to drag EUR/USD below $1.09 yet, but the common currency remains vulnerable amidst a quiet data docket today and attention turning to the US debt limit saga.

In terms of positioning, speculators the euro is the most overbought currency in G10 according to CFTC data, with net long positions of euros worth 22% of open interest, which is the highest since January 2021. Although this paints a positive view of the euro, it also increases the risk of corrections lower in EUR/USD in the short term.

Dollar firms amid risk-off market conditions

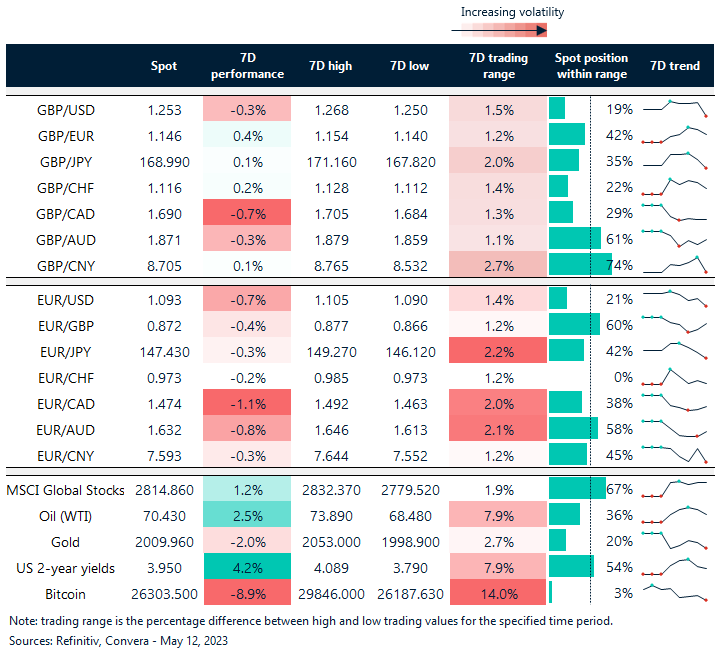

Table: 7-day currency trends and trading ranges

Key global risk events

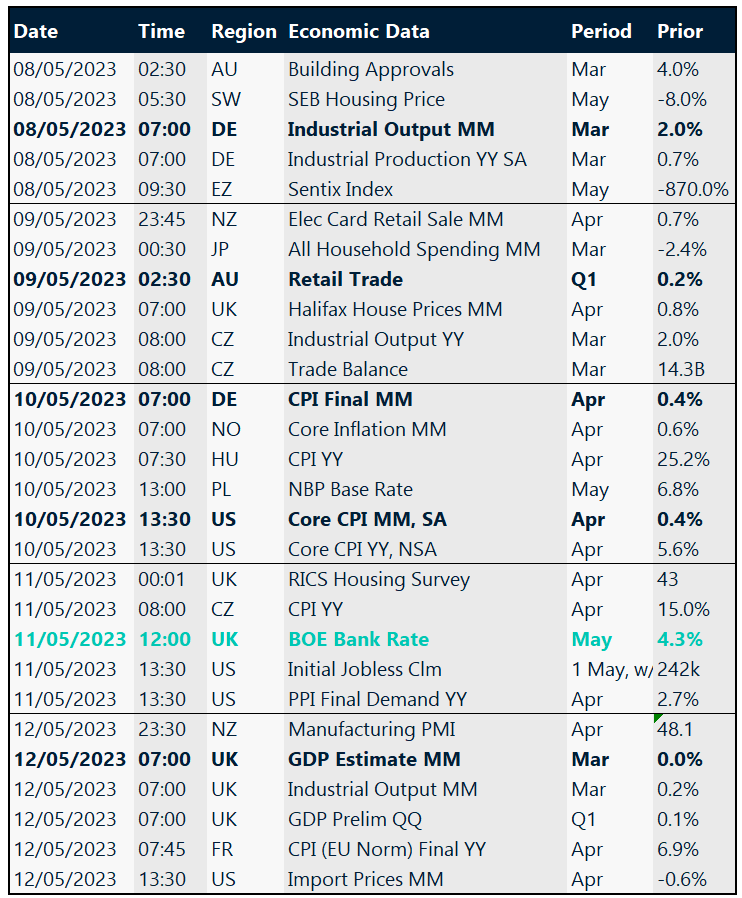

Calendar: May 8-12

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.