Written by Convera’s Market Insights team

A strong US labor report

Boris Kovacevic – Global Macro Strategist

A patch of strong macro data out of the United States has reversed last week’s trend of falling equity prices and government bond yields. The US economy added more people to its workforce than expected and consumer sentiment brightened up a bit in November. While those two data points have dampened investors hopes of an early rate cut from the Federal Reserve in the first quarter of next year, the maintenance of the soft-landing scenario has supported both US equities and the Greenback.

The US added 199 thousand people to its workforce and therefore more than the 190 thousand economists had expected. The biggest surprise came with the release of the unemployment rate, which fell from 3.9% to 3.7%. The non-farm payrolls report is at odds with other macro data released last week. Job openings, the ADP private employment report and the earlier released S&P PMI survey signaled a cooling of the US labor market. However, the solid jobs growth number has added enough ambiguity to the data for the Federal Reserve to not lean into the markets rate cutting speculation. Momentum in US hiring is weakening but not enough to signal a clear pivot from policy makers.

Still, the November print has not changed our overall view on the labor market. The totality of data has been confirming the weakening trend in hiring and it is likely for the number to be revised down. Eight out of the last nine non-farm payrolls prints in 2023 have been revised to the downside, meaning that the US economy has added 400 thousand jobs less to its workforce than the first estimate would have suggested.

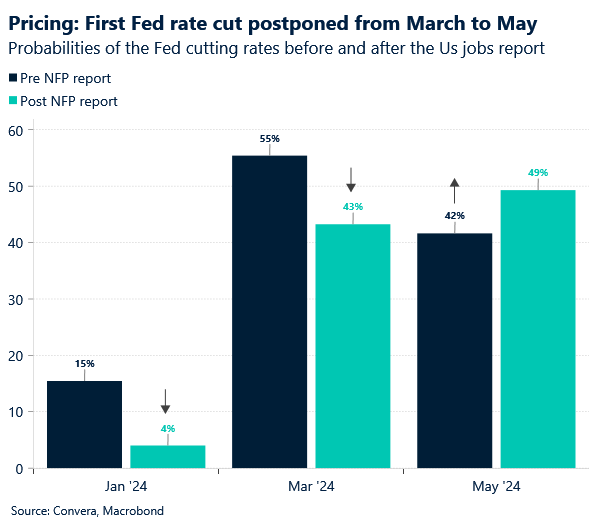

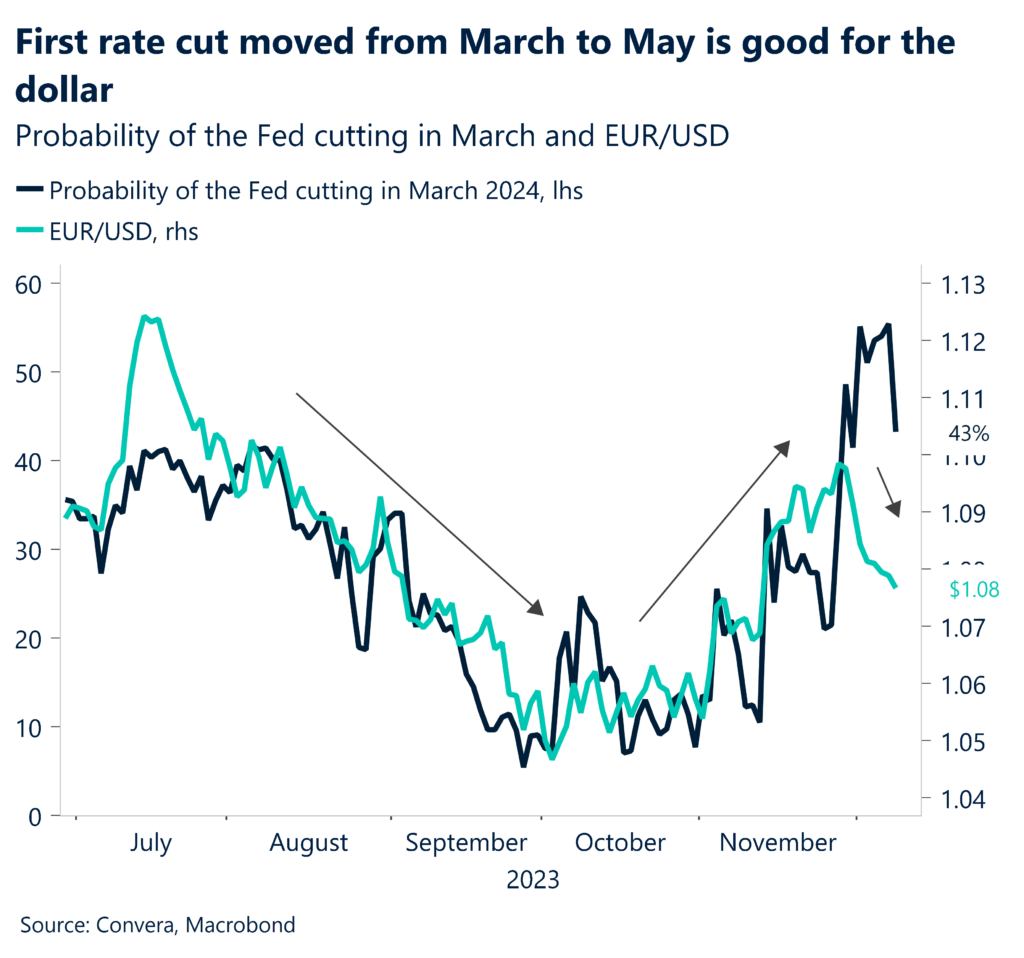

Investors have pushed their expectations for the first rate cut from the Fed from March to May 2024. The number of cumulative cuts (5) for the whole of the next year has remained the same. The US Dollar Index recorded its first weekly rise in a month as the strong US jobs print and dovish comments from ECB policy makers supported the Greenback. DXY (103.90) is now around 4% up from its July low and is 3% below its October high, establishing a short-term trading range between 100.00 and 107.00

Copy, paste. BoE to repeat its last meeting?

Boris Kovacevic – Global Macro Strategist

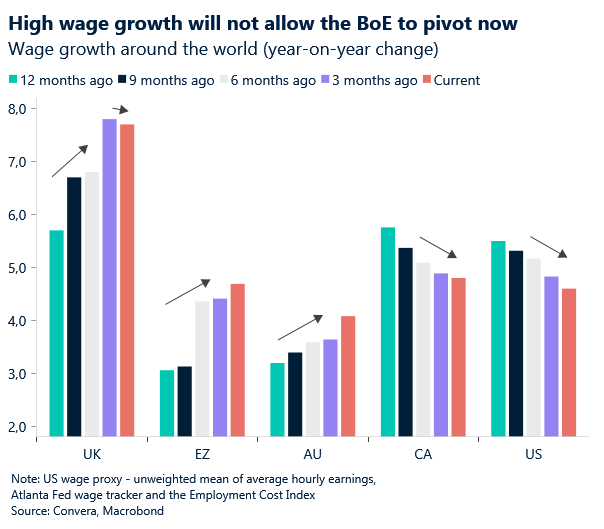

The Bank of England remained on hold for a second consecutive time at the November meeting, after having raised its policy rate to a 15-year high of 5.25% in July. Recent comments from British policy makers suggest that the 6:3 (six members voting for a hold and three for a hike) will be replicated on Thursday. This could, at least for now, solidify the BoE as the most hawkish central bank within the G3 space and limit the markets resolve to price in more rate cuts for 2024. Both Governor Andrew Bailey and Deputy Dave Ramsden have recently said that (1) market pricing on cuts remains too optimistic and that (2) services inflation remains too high to consider policy easing. While we do see these stances easing early next year, this hawkish rhetoric could be enough to fend off investors for now.

One reason for pausing its tightening cycle will be the slowdown of headline inflation from 6.7% to 4.6% and core inflation from 6.1% to 5.7% in November. The overall trend in the survey data looks promising, but not enough to fully convince the BoE of leaning into rate cutting speculations. The British Retail Consortiums retail survey showed shop prices continue falling on a year-on-year basis, coming down from 15% in April to 7.7% in November. The same holds true for price pressures in the services sector, according to the survey from the Confederation of British Industry. However, the prices charged component of the UK services PMI survey jumped up to the highest level in four months, dampening the near-term optimism. National wide pay negotiations will be completed in Q1 next year with the approved 10% rise in the national living wage (nlw) getting implemented.

Continued selling momentum saw cable ($1.2540) lose 1.2% of its value this week as the pound retreated from overbought territory and the ongoing price dynamics continue to be largely driven by US developments. The favourable expected interest rate differential and a recent dovish ECB tilt had sterling testing fresh four-month high against the euro around the $1.6900 level earlier last week but the pair gave back some of its gains and is now trading at $1.1650.

Euro suffers third worst week in 2023

Ruta Prieskienyte – FX Strategist

An unexpectedly dovish European Central Bank (ECB) tilt ignited a euro selloff, in what was the third worst weekly performance against the US dollar in 2023. EUR/USD fell by over 1.1% w/w and touched at fresh 3-week low. Meanwhile, a strong US NFP print on Friday pushed back Fed rate cut expectations, further weaking the EUR/USD pair.

Going into the final rate decision meeting of the year, the ECB has been dealt with a tricky hand when it comes to keeping their options open without sounding too detached from reality. On one hand, inflation continues to fall at a faster pace than previously anticipated, and the latest headline CPI for November slowed to 2.4%. However, wage growth remains one of the key concerns regarding the future evolution of inflation. The indicator has been on an upward trajectory since June 2022 across the bloc. Specifically, real negotiated wage growth in Netherlands is at 9% y/y – the fastest growth since 1998. To add to the headache, the real economy is feeling the strain of the ECB’s cumulative tightening campaign. Eurozone GDP declined for Q3 declined for the first time since 2020 and German industrial production is at 13-year low when discounting the pandemic effect. The European business cycle is bottoming based on the improvement of leading indicators, but the lagging data continues to point to a negative Q4 GDP print and a technical recession call.

The main question for the ECB remains: is the central bank willing to sacrifice economic growth at the expense of waiting to confirm that the job is done taming inflation? Remarks from the officials have been mixed, but with a clear dovish tilt. As of last week, three policymakers confirmed rates shall not be hikes further and some opened a door for rate cuts in no earlier than H2 2024. Meanwhile, markets attach a 70% probability for such an outcome as early as March. While we agree that ECB is likely to be the first to cut rates across the G3 banks, we do not think that the first rate cut shall come sooner than the April meeting. Overall, the expected rate differential outlook remains euro non-supportive going into the decision week and the start of 2024.

Strong NFPs support US dollar

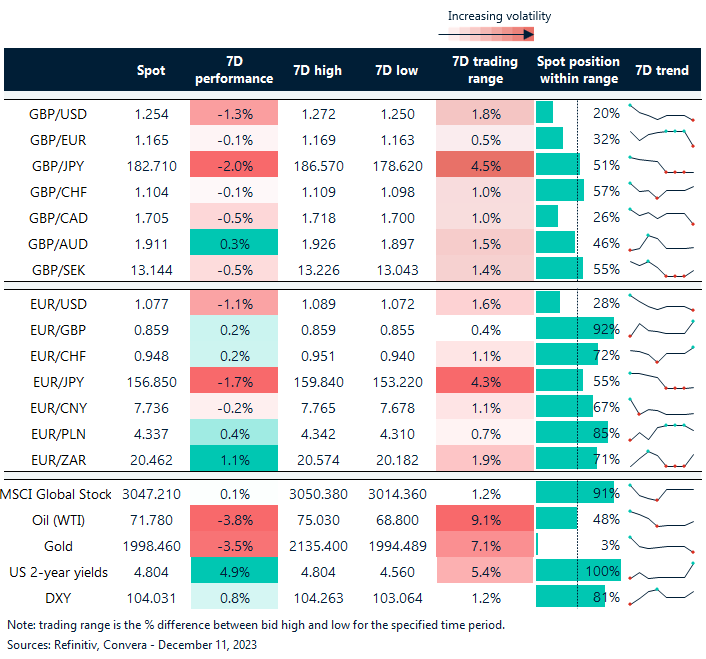

Table: 7-day currency trends and trading ranges

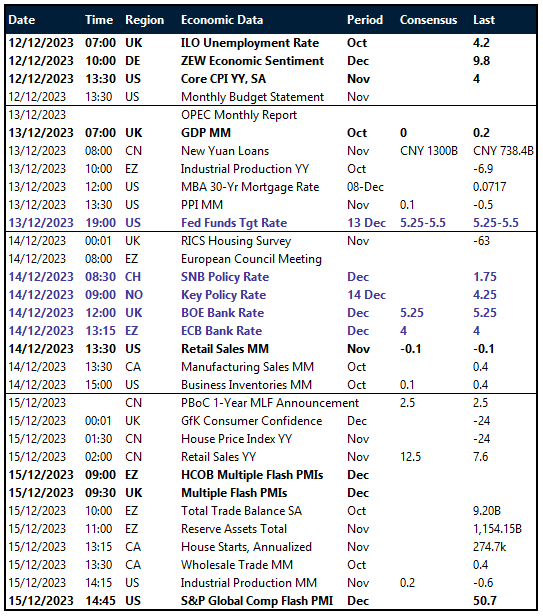

Key global risk events

Calendar: November 04 December