Written by Convera’s Market Insights team

Five questions going into the week

Boris Kovacevic – Global Macro Strategist

Global investors have been facing multiple headwinds in recent weeks with the US earnings season in full swing, treasury volatility remaining at elevated levels and geopolitical developments being monitored on a daily basis. At the same time, investors have continued gauging the impact of tighter financial conditions on consumers and companies with the incoming data as a guide. The verdict so far has been that pro cyclical and rates sensitive industries (housing, manufacturing) and countries (Europe) have fallen into recession. The global manufacturing sector has been contracting for eleven consecutive months now with home prices falling in most countries in the developed world. The US dollar has remained strong amid all the market uncertainty.

At the same time, the US continues to defy calls for a slowing economy as most lagging indicators have been coming in strong. Last week showed the US economy expanding by 4.9% in the third quarter, beating expectations of a 4.3% increase and recording the strongest growth rate in more than two years. Consumer spending remains resilient as well and has risen by 0.7% in the month of September, as highlighted by Friday’s PCE report. However, the slowdown of leading indicators has been gaining attention in recent months. The US ISM PMI for the manufacturing sector has been in negative territory for 11 consecutive months now, the longest streak since 2009. The Conference Board’s CEO Confidence Index has been contracting for 21 months.

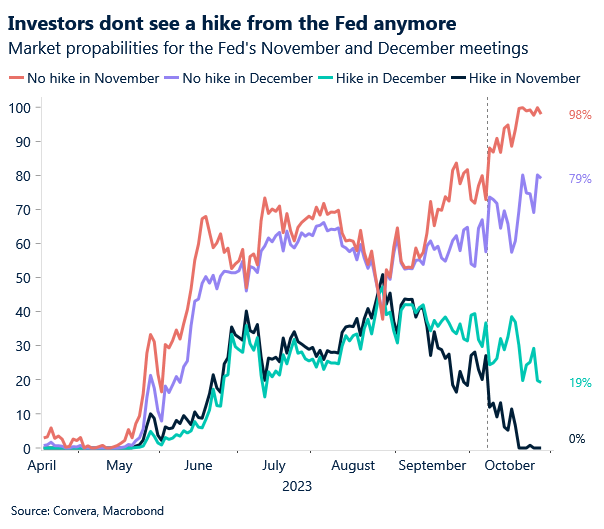

The upcoming week will be highly important to sense-check the preexisting narratives driving markets today. Going into the week, we are looking for clues to answer five key questions. (1) Is the disinflationary trend going to continue in Europe? (2) How soon will the Bank of Japan pivot from its position as the last dove standing in the G10 space? (3) How will the Fed react to the recent strengthening of US economic data? (4) Will the Bank of England follow in the ECB’s footsteps and leave policy rates unchanged? (5) And, has the US labour market resilience continued in October?

Macro data to drive FX this week

Boris Kovacevic – Global Macro Strategist

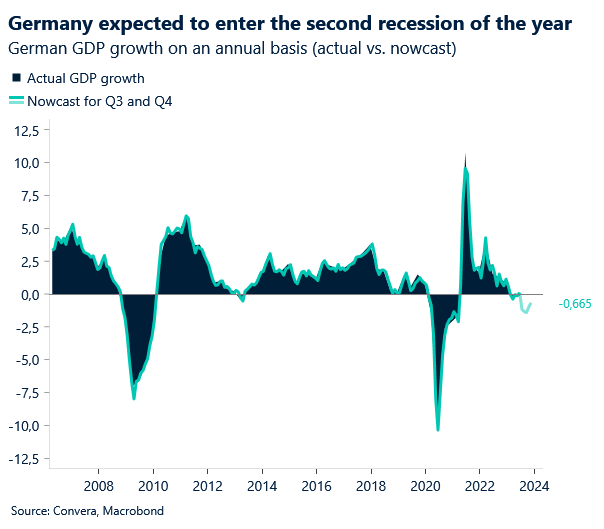

The European picture is much clearer to interpret. The most aggressive tightening cycle in the ECB’s history and the energy crisis have led to the manufacturing sector falling into recession, money supply shrinking at a record pace and demand for new loans contracting at levels not seen since the Global Financial Crisis. We are forecasting a negative German GDP for Q3 this week and continue to believe that the ECB’s projection of inflation not returning to the 2% target by 2025 remains too pessimistic. We see the European Central Bank as the most likely to start easing policy next year, followed by the Federal Reserve. The two rate decisions will give us more insights into the thinking of both the Fed and BoE.

Our short-term bearish bias on EUR/USD ($1.0550) remains intact amidst the plethora of weak European economic data last week including dismal PMIs and weak loan demand. This preceded the ECB holding interest rates steady for the first time since June last year. The economic situation in the Eurozone is deteriorating stronger and faster than the ECB had anticipated, thus it was no surprise that the meeting was marginally on the dovish side of expectations and led to a minor dovish market reaction. EUR/USD failed to break above its 100-week moving average and remains anchored below all its key long-term daily and weekly rolling averages and almost 6% below its 2023 peak.

Unless the Eurozone economy miraculously rebounds in the coming weeks, the ECB has probably finished hiking in this cycle, and we expect next week’s flash inflation prints to reaffirm this notion. As we draw nearer to European peak pessimism though, we still hold a more bullish view on EUR/USD going into 2024. The European inflation and GDP data will be closely watched as investors continue to gauge how likely the Eurozone is from bottoming in terms of its economic momentum.

No hike, but “high for longer” message expected

George Vessey – Lead FX Strategist

The pound fell to a 3-week low under $1.21 versus the US dollar last week as focus shifted to rate and growth fundamentals. GBP/USD has managed to reclaim the $1.21 handle but is lacking upside momentum as a plethora of risk events loom, including the Bank of England’s (BoE) rate decision and Monetary Policy Report on Thursday.

We expect the BoE to keep Bank Rate unchanged at 5.25%, which is in line with current market pricing. Markets have substantially scaled back tightening expectations from a 50% chance of a hike to less than 10% following a slew of weaker activity, consumer spending and labour market data recently. Some of the minority on the MPC who supported a rate hike in September will probably stick to their guns, but their number could shrink due to data developments, and this could weigh on the pound. However, it’s unlikely the BoE will want to close the door to further tightening, so the MPC will likely want to ensure that its previous ‘high-for-longer’ message is the key takeaway from November’s policy statement. Such a message should provide sterling some support, but as ever, the UK currency will also remain vulnerable to the global risk profile, which makes forecasting its direction even more unpredictable.

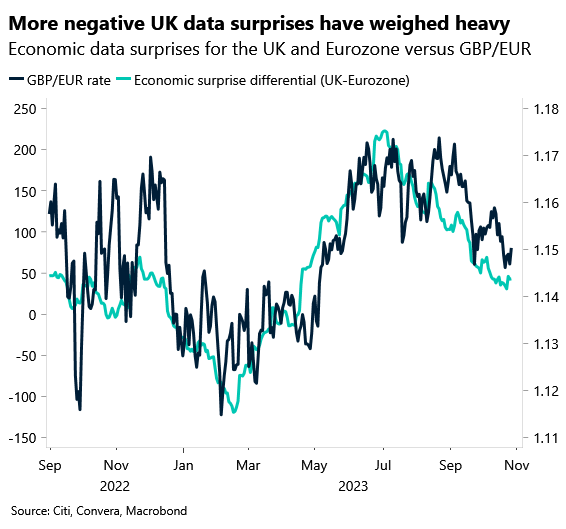

One area of surprise lately has been the downtrend in GBP/EUR. The currency pair has drifted into the bottom 10% of its 3-month range, breaking south of €1.15 (its 2023 average) and remains bearish below its 200-day and week moving averages. Although yield differentials favour the pound, the economic surprise differential does not. Markets may be coming around to the fact that the UK economy is struggling much like Europe and recession risks are on the rise.

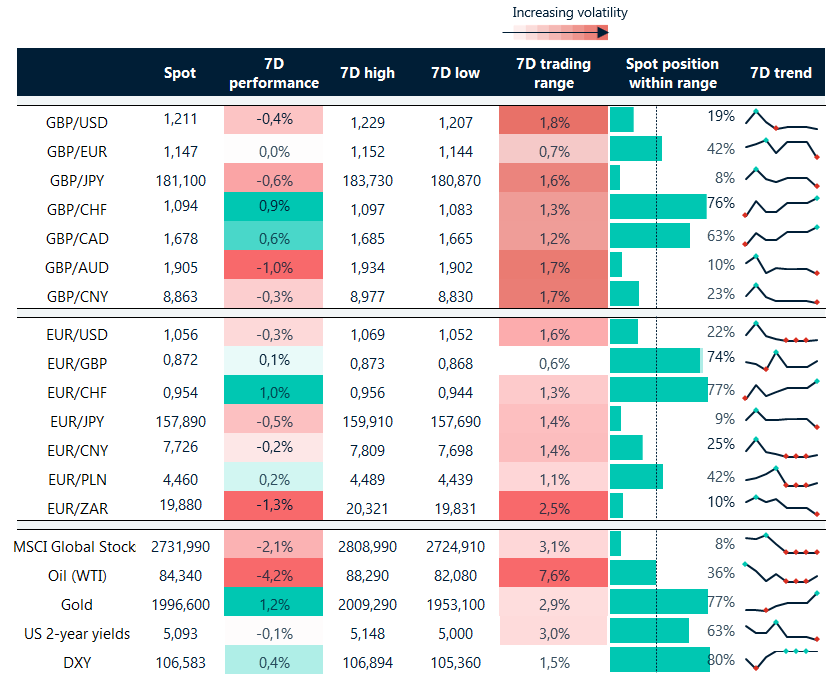

USD drags EUR & GBP into bottom 20% of weekly range

Table: 7-day currency trends and trading ranges

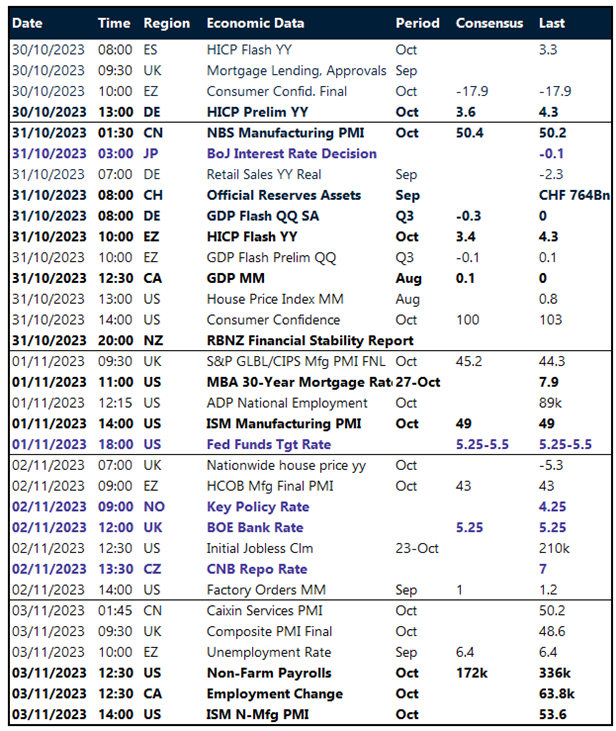

Key global risk events

Calendar: October 30 – November 03

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.