Written by Steven Dooley and Shier Lee Lim

Key markets ease from highs

Global markets remained mostly upbeat over the Christmas-New Year period with US sharemarkets higher for the ninth-consecutive week and other key markets taking this lead.

The Dow Jones and Nasdaq both made new all-time highs while the S&P 500 has also neared a new record high.

In other markets, the US ten-year bond yield fell to a five-month low over the break while copper reached a five-month high. Iron ore hit an 18-month high.

In FX markets, the US dollar continued to weaken.

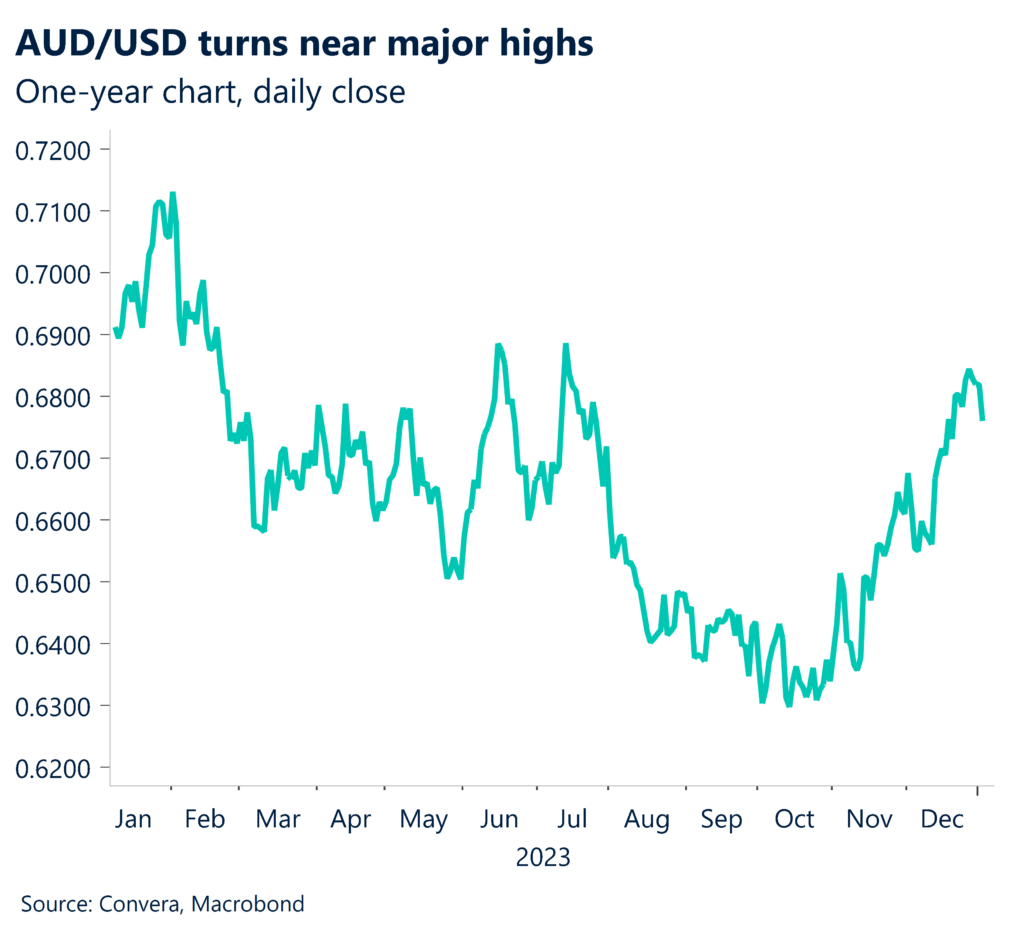

The AUD was the stand-out performer with the AUD/USD hitting a five-month high last week before easing. The NZD/USD also hit a five-month high before easing.

The USD/SGD fell to 11-month lows before rebounding while the USD/CNH fell to seven-month lows.

Overnight, however, markets saw losses, with US shares leading other markets lower. The USD rebounded close to 1.0% as it extended gains from five-month highs.

Fed starts pushing back

To little effect, Federal Reserve officials in mid-December 2023 kept downplaying the likelihood of a massive sequence of rate cuts. For example, Alanta Fed president Rapheal Bostic said on 20 December that he expects only two rate cuts in 2024.

The economic evidence was contradictory, but not insufficient to support a dramatic reversal of course. The risk remains that the market’s rate cut predictions – looking for 150bps or cuts – are overly optimistic and a recalibration of expectations sees the USD lift.

Nevertheless, we will be constantly monitoring to see whether there are any changes in the rising trajectory of inflation expectations and the commodities market, a leading source of information about the changes. Any rebound in inflation expectations or commodities could lift the USD.

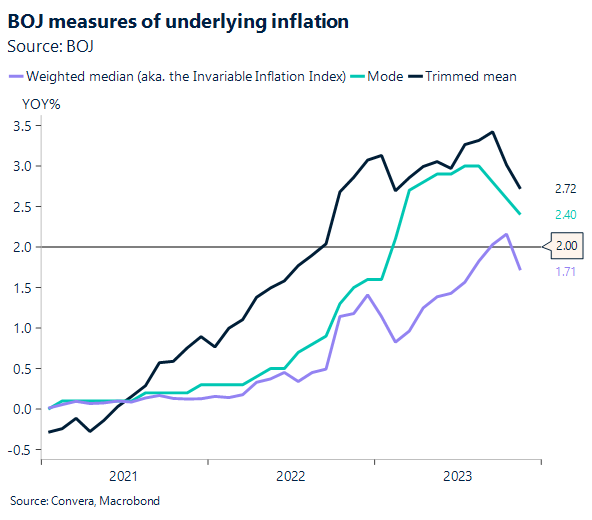

Japan in focus for potential shift

Although the Bank of Japan meeting on 18-19 Dec saw no change in policy, the BOJ has not committed to delaying rate increases until after the labour talks in April, and it may yet decide to do so at the January meeting.

The BOJ’s reluctance to make a firm announcement last month may not be due so much to the state of the Japanese economy or wage developments. There was a sense even during Governor Ueda’s post-meeting news conference that the policy board is becoming more certain that wages and prices are in a healthy cycle and that the BOJ is reaching an agreement on rate increases.

The market’s enthusiasm to price in rate reduction that go beyond the Fed’s abrupt dovish turn at the December FOMC may have turned off the BOJ. To put it another way, the strong USD/weak JPY trend might reverse as the BOJ steps up its efforts to set the stage for rate hikes through the media and other channels.

We think that as expectations for Fed rate cuts build and FX volatility increases, risks grow that the USD/JPY may drop to the 130–140 region in the first half of 2024.

Aussie, kiwi turn from highs

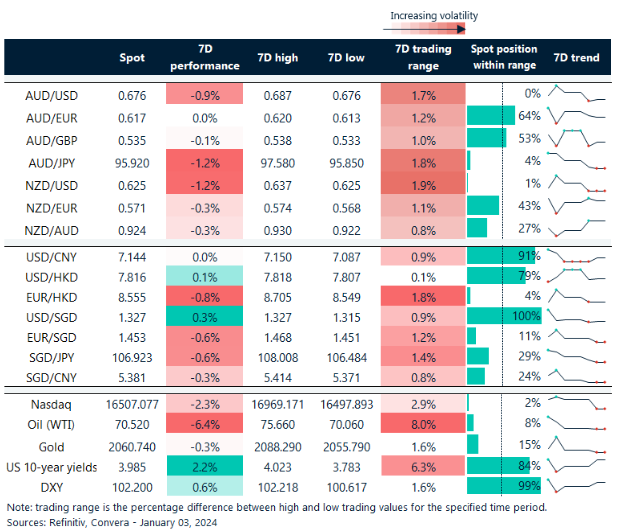

Table: seven-day rolling currency trends and trading ranges

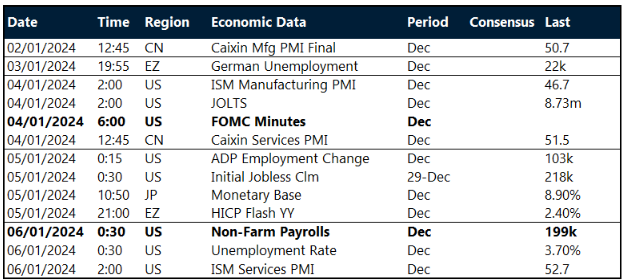

Key global risk events

Calendar: 1 – 6 January

All times AEDT

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.