USD: Stagnation with a price twist

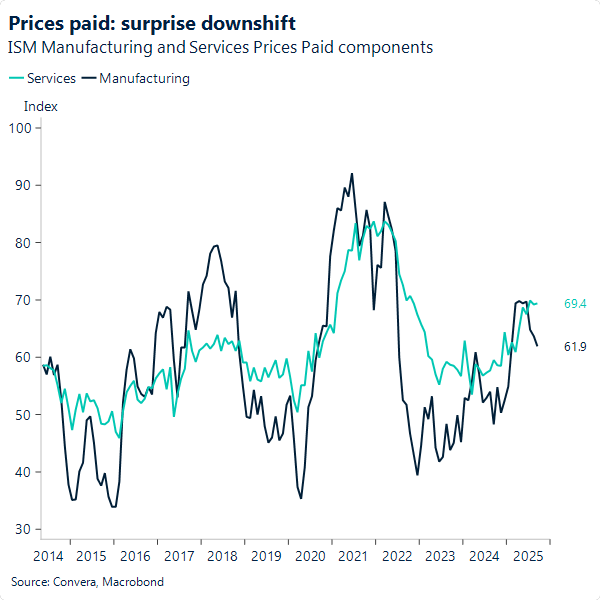

ISM Services and Manufacturing PMIs last week were weak. Manufacturing contracted for a seventh consecutive month (49.1), while the services index – released Friday – fell 2 points to 50, a level that signals stagnation. Notably, the prices paid component in services rose to 69.4, one of the highest readings in three years. In contrast, manufacturing prices paid – where inflationary pressure from tariffs is typically expected – actually declined from 63.7 to 61.9, pointing to eased price pressures. The PMIs add to a fragmented set of labour market indicators from private data providers last week, collectively depicting a stagnant labour market, despite some improvement in September relative to August.

Nonetheless, it’s hard to argue the greenback reacted meaningfully to these often-overlooked data points. Investors may be discounting the severity of the shutdown, opting to wait for more substantive directional cues – namely, the release of non-farm payrolls. While the impact has been muted so far, the release of Fed minutes this week and hard macro data from public sources – once the shutdown is lifted – could lend more cohesive meaning to last week’s fragmented broader data landscape.

Our expectation is for a continued cautious tone from the Fed, likely to be reflected in this week’s minutes (Wednesday). Currently, nearly half of the FOMC sees just one or no further cuts by year-end, while the median projection remains at two. With one full cut priced in for October, we expect a near-term lift in the dollar – to strengthen if NFP shows signs of recovery.

EUR: No break without payrolls

EUR/USD attempted once again to break above resistance at 1.1750 on Friday, with greater conviction following the weak ISM Services release. Nonetheless, it failed to clear the level, leaving the non-farm payrolls report as the next potential catalyst to make the break a reality.

The euro may have also benefited from modest upside momentum following an interview with President Lagarde, in which she stated she is comfortable with current policy settings, citing broadly stable inflation in the euro area. These remarks contrasted with the more dovish tone she struck earlier in the week at the Bank of Finland’s 4th International Monetary Policy Conference.

Overall, we maintain that the pair continues to show fatigue in pushing higher, trading in a tight and directionless range between 1.1720 and 1.1750 last week, despite several soft US data prints. Had sentiment toward the USD been as negative as it was in the spring, weaker indicators – amplified by the silence surrounding the shutdown – might have generated stronger bullish momentum for EUR/USD.

Looking ahead, a batch of eurozone macro indicators – namely Germany’s industrial production and factory orders, along with eurozone retail sales – will help gauge the region’s economic pulse. Recent data continues to suggest stagnant momentum. Given the ECB’s just re-affirmed hawkish tone, however, only significant downside surprises may prompt a meaningful re-pricing of easing expectations, weighing on the euro. Nonetheless, we expect bearish pressure to build ahead of the FOMC meeting minutes this Wednesday.

EUR/USD begins the week on the soft side, breaking below support at 1.17 as the lack of US data releases further suffocates momentum.

GBP: A tricky Q4 awaits sterling

Sterling’s struggle to build momentum beyond $1.35 against the US dollar and €1.15 versus the euro reflects a market still grappling with multiple headwinds. While the pound has shown resilience at times, its rallies continue to stall at familiar resistance levels, capped by a mix of macro uncertainty, policy risk, and technical fatigue.

Heading into the UK’s Nov. 26 Budget, traders are quietly bracing for potential trouble. While the fiscal premium appears largely priced in, if the event delivers a more negative outcome than expected, the pound will weaken. That said, if the Budget passes without major surprises, attention will shift back to the UK’s growth outlook and monetary policy, though neither are exactly screaming a positive bias for GBP.

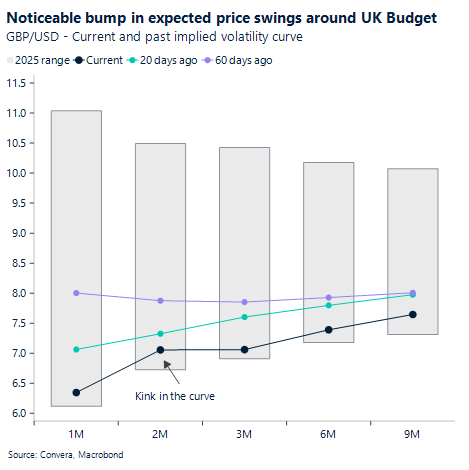

Sterling volatility has been steadily declining in recent months, mirroring broader trends across major currencies. But the two-month maturity – covering the Budget – stands out. It shows a clear kink higher in the curve, signalling that traders expect a pickup in price swings around the event. That bump suggests the Budget is being viewed as a potential flashpoint for GBP.

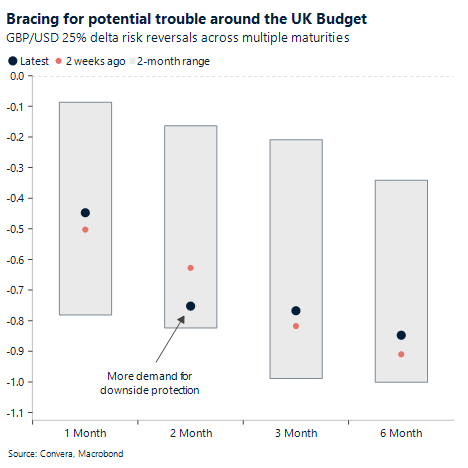

Another way to measure market nerves is through “risk reversals” – a tool that shows whether investors prefer protection against a currency rising or falling. Again, the two-month tenor is the only one showing increased demand for downside protection compared to two weeks ago – a subtle but telling shift. While broader bearish positioning has been unwound, traders are selectively adding cover against sterling weakness around the Budget risk event.

Of course, the Budget might come and go without shaking markets. If it lands broadly in line with expectations, the pound could quickly refocus on other drivers like growth and rate policy. An earlier-than-expected Bank of England (BoE) rate cut, triggered by deteriorating economic conditions, would weigh heavily on the pound – especially against the euro, where the ECB is expected to hold rates steady well into 2026. With money markets pricing just one full BoE cut by end-March, any shift toward a more dovish path could trigger a sharp repricing and renewed pressure on the pound.

Euro crosses lack clear direction

Table: Currency trends, trading ranges and technical indicators

Key global risk events

Calendar: October 6-10

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.