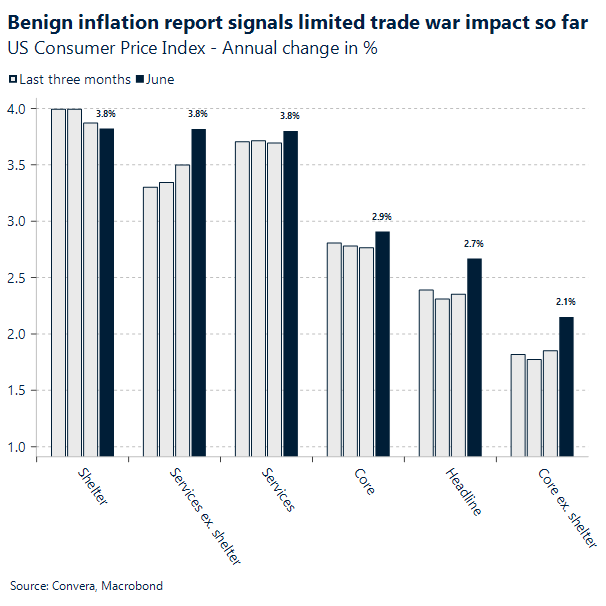

Very modest tariff impact on inflation

Very modest tariff impact on inflation. The June inflation report showed headline consumer prices rising 2.7% year-over-year, just above the forecast, while core CPI matched expectations at 2.9%, up slightly from 2.8% in previous months. On a monthly basis, core inflation rose 0.2%, coming in under the 0.3% estimate and well within the Federal Reserve’s target range. One of the factors behind this moderation was a decline in prices for used cars and trucks, new vehicles, and airfares, all of which pulled down the core index for the month. On the other hand, categories most exposed to higher import taxes, such as furniture, appliances, apparel had faster price increases during June, signaling tariff impact has indeed appear, but very modest thus far.

Though the data supports a cooling inflation trend, it’s unlikely to prompt a policy shift at the Fed’s next meeting in two weeks. A repeat of this subdued performance in July, however, could build a stronger case for a rate cut in the fall. Investors were quick to react, futures for the S&P 500 and Nasdaq 100 rose to session highs, showing renewed confidence that the inflation trajectory is improving. Treasury yields fell broadly, and the two-year note, which is especially sensitive to rate expectations, dropped to its daily low and now trades a basis point lower at 3.90%.

Futures pricing suggests a 59% chance of a rate cut by the September FOMC meeting. Even though tariff-driven price increases haven’t surfaced clearly in the CPI yet, concerns over future trade-related pressures are influencing how markets view Fed policy. That anticipation is helping temper the usual knee-jerk rally in longer-term Treasuries, creating a more balanced market response.

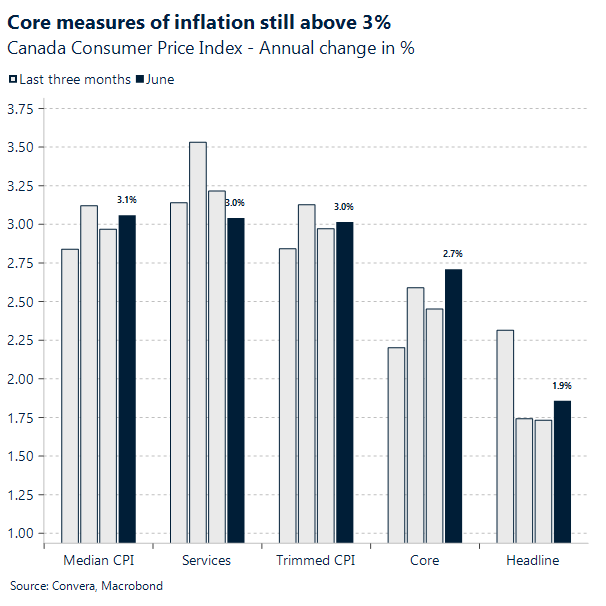

Sticky inflation means no rate cuts this year

Canadian consumer prices picked up in June, marking the first acceleration in four months and clouding prospects for a rate cut by the Bank of Canada later this month. Headline inflation rose to an annual pace of 1.9%, while the central bank’s two preferred core measures edged up to 3.05%, pointing to continued underlying price pressures. The proportion of components in the CPI basket increasing at a rate of 3% or more climbed to 39.1%, up from 37.3% in May, reflecting a broader firming in inflation across categories. Given this backdrop, futures markets are now pricing in no rate cuts for the remainder of the year, signaling a shift in expectations as the inflation narrative remains more resilient than anticipated.

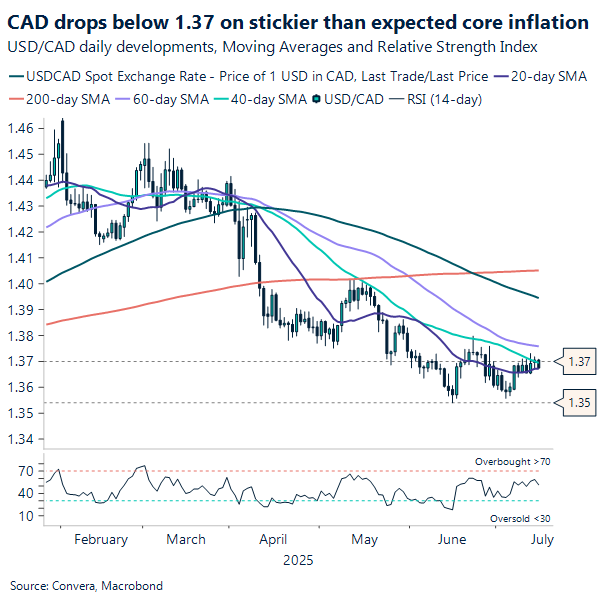

The Canadian dollar fell to 1.367 amid expectations that the Bank of Canada will hold rates steady for the rest of the year. However, the decline was short-lived, as markets absorbed the latest U.S. inflation data and demand for the dollar surged on speculation that the Federal Reserve may keep rates unchanged beyond September.

U.S. inflation in focus

The dollar index (DXY) has traded between 97.800 and 98.100, indecisive on whether to break into the 98 zone amid a lack of macro data releases.

Beyond the US CPI inflation, another catalyst for DXY will be Thursday’s retail sales report. Markets are increasingly attuned to any disappointing data that could lend weight to a more bearish outlook for the US economy – one backed by hard data rather than sentiment alone.

On the trade front, more threats and possibly preliminary deals can be expected this week. However, such threats continue to have muted effects on DXY and its components, with markets largely viewing them as part of a broader negotiation strategy rather than imminent policy changes.

That said, here’s the caveat: while threats may have lost their initial market-moving potency, the US administration remains as unpredictable as ever. Trump may feel emboldened by the US economy’s resilience, with the S&P 500 hitting an all-time high despite widespread uncertainty—and this may well just reinforce the magnitude and breadth of the proposed tariffs.

As we approach the August 1 deadline, if tariffs are indeed imposed, we’re likely to see a reversion to the trends that prevailed until recently – namely, dollar weakness, with the euro standing out as the primary beneficiary. Should the renewed scare be complemented by hardline evidence that the U.S. economy is suffering because of tariffs, markets will most certainly respond with more severe sell-offs, sending the dollar into a sharper decline.

Brussels builds bridges amid tariff heat

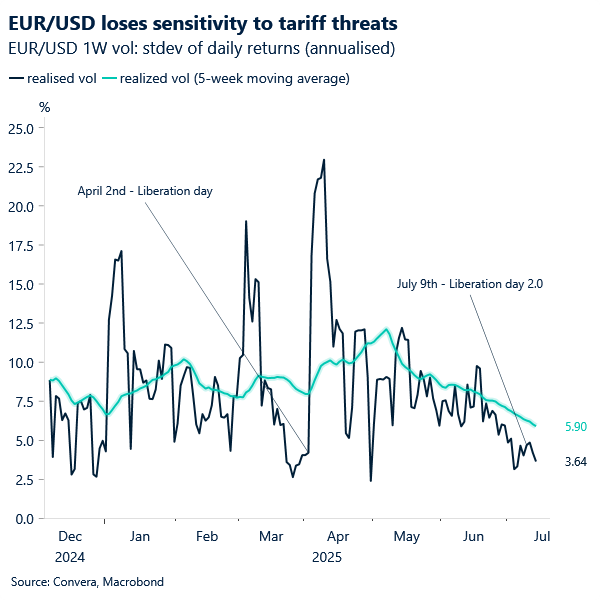

Over the past month, EUR/USD has faced more of a moderate decline, rather than an outright drop, down almost 0.9%. Despite the recent 30% tariff threat on EU imports at the weekend, the euro traded little changed – just below $1.17 – after paring an earlier slide of as much as 0.3% to $1.1651 last week, its lowest level in nearly three weeks. Since then, EUR/USD has found support at $1.1660.

The gentle decline has been driven predominantly by a re-pricing of sentiment, carving out some risk premium from the dollar as tariff threats carry less weight with investors. After all, back in May, Trump threatened the EU with a 50% tariff on all EU goods amid stalled trade negotiations. A 30% threat, ironically, marks a substantial reduction.

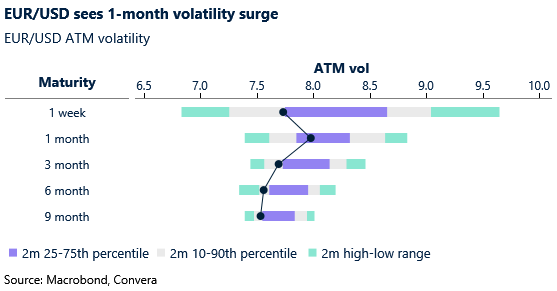

Had markets been more sensitive to the 30% threat, the euro’s drop would likely have been sharper, aggravated by increased expectations of an additional rate cut by year-end. Instead, swaps are pricing in a 90% chance of a cut today, down from fully pricing a 25-basis-point cut earlier in July. Meanwhile, implied at-the-money volatility—which captures expected fluctuations in the pair—shows a spike only at the 1-month maturity. This aligns roughly with the extended tariffs deadline and its imminent aftermath. The relatively muted volatility across the rest of the maturity curve—ranking in the lowest 10% over the past two months—suggests that markets have largely priced in the risk from tariff threats.

With little new data from either Europe or the U.S. yesterday, the key event was the European Commission’s renewed interest in stepping up engagement with other countries affected by Trump’s tariffs, such as Canada and Japan.

These almost vindictive, intensified talks underscore global frustration with the escalating trade war—and signal, even if reluctantly, preparation in case threats turn into reality.

Over the weekend, the EU reached—perhaps not coincidentally—a tentative economic agreement with Indonesia, a country facing a 32% US tariff despite ongoing negotiations to lower that rate. Indonesian President Prabowo Subianto called the outcome with the EU a “breakthrough” after 10 years of trade discussions, expressing hopes to return to Brussels for the formal signing of the accord, known as the Comprehensive Economic Partnership Agreement.

The reignited trade war may have served as the catalyst that pushed both sides to finalize this long-awaited deal.

Later yesterday, European Commission President Ursula von der Leyen spoke with Canadian Prime Minister Mark Carney—a step widely seen as part of a growing effort to envision a new trade reality, one less reliant on the U.S.

However, these developments alone were not sufficient to drive price action, with EUR/USD consolidating below $1.17 over the past few days. Having said that, should U.S. CPI come in below expectations, you can expect expect this newly-formed resistance to be breached.

Sterling tumbles as rate cuts fear mount

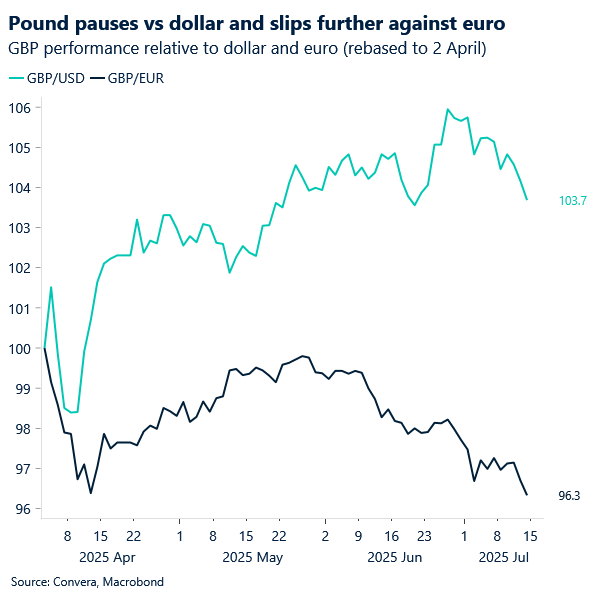

While the pound’s impressive rally against the dollar is showing signs of slowing, hitting a new three-week low of $1.3422 this morning (Tokyo session); against the euro—the key beneficiary of 2025’s structural dollar weakness, sterling continues its downtrend, now down just over 4.5% year-to-date. The pair reached a new three-month low of $1.1499, today, during Asia trading hours.

Bearish pressure on sterling has mounted amid concerns about a faster pace of UK interest rate cuts driven by a cooling job market and timid growth prospects. Bank of England Governor Andrew Bailey told The Times yesterday that more aggressive rate cuts could be possible if the jobs market slows too quickly. Markets currently anticipate a 50-basis-point BoE rate cut by year-end.

Thursday’s UK employment data, if it disappoints to the downside, will solidify those expectations and add further downward pressure on the currency. GBP/USD may then test its June 23rd low of 1.3371, marking the pair’s lowest level in one month.

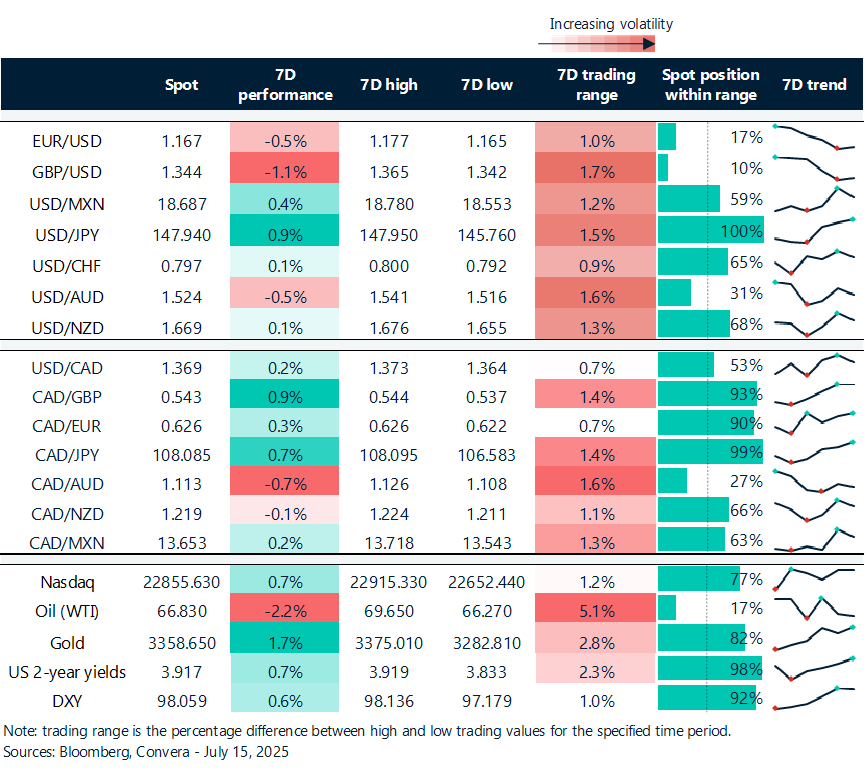

Sterling drops across the board

Table: 7-day currency trends and trading ranges

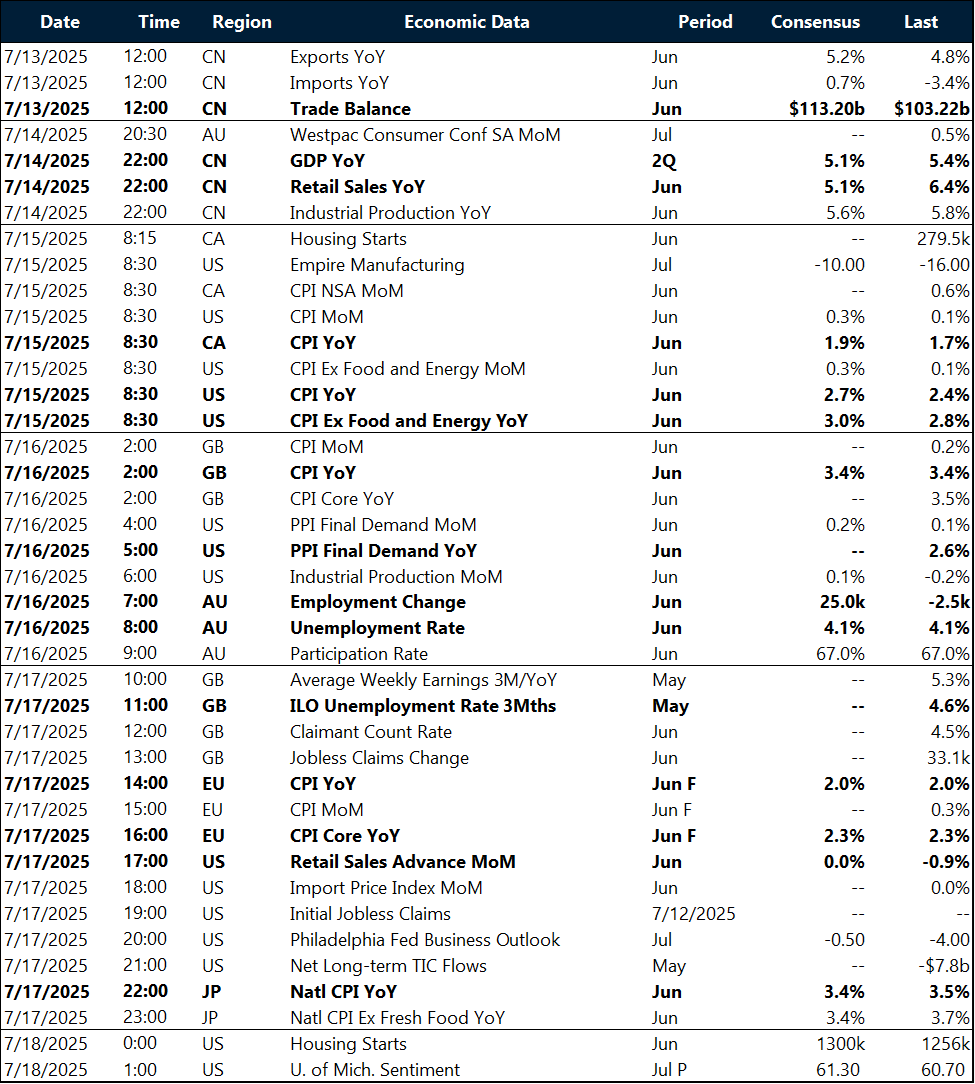

Key global risk events

Calendar: July 14-18

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.