USD: Strong dollar, shaky foundations

The upheaval in the Middle East, now in its tenth day, shows no sign of easing as it continues to roil energy markets. Brent broke the psychologically important 100‑dollar‑per‑barrel level in the Asia session today, briefly surging toward 120 dollars in a 28% intraday jump, the largest since April 2020. The UAE and Kuwait have joined Iraq in reducing oil production as storage capacity thins due to the blocked passage through the Strait of Hormuz, helping drive the latest the leg higher. In Iran, the appointment of the late Ayatollah Ali Khamenei’s son as the new supreme leader has added to geopolitical uncertainty, with President Trump calling the move “unacceptable.”

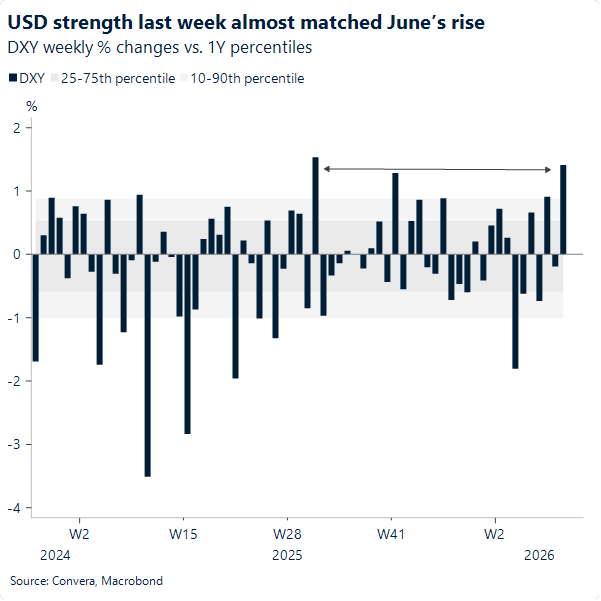

The US dollar has mirrored the bullish tone in oil, kicking off a leg higher in the Asia session and rising 1.4% last week. Friday did see the currency pare some gains after a dismal US jobs report. The economy shed 86k jobs in February while the unemployment rate ticked up to 4.4% from 4.3%. While the weak outcome may have been largely due to severe weather disruptions, strike actions and base effects after January’s strong gains, investors are questioning the stability of the labour market that the Fed has highlighted. The dollar’s bearish reaction was also telling. The DXY fell 0.3% on the day despite support from surging oil prices. The move highlights the currency’s sensitivity to the US macro narrative, which continues to intertwine with a still-present Trump-related bearish bias toward the greenback.

We believe that while the conflict may support the dollar in the near term, the medium-term outlook could look far less favourable. The conflict has already pushed gasoline, diesel and jet fuel prices higher, worsening an already delicate cost-of-living backdrop. That dynamic could hurt Republicans in May’s mid-term elections and reignite a political risk premium that weighs on the greenback.

On the Fed outlook, 2026 may end up resembling 2025, when the Fed maintained a cautious stance as Trump’s sweeping tariff agenda stoked fears of a high-inflation, weak-growth scenario, a classic stagflation risk. Now, the conflict in the Middle East early in 2026 is raising similar concerns. Unlike in 2025, however, the Fed will also face a leadership transition. In May, Trump’s expected pick, Kevin Warsh, is widely anticipated to replace Jerome Powell as Fed chair. Markets tend to react nervously to such changes, as investors must reassess how new leadership will interact with the FOMC and how the policy outlook may shift. At a time when markets already fear a more dovish, Trump-aligned Warsh, the dollar may lose the stabilising support that a relatively predictable Fed framework provided in the second half of 2025, when tariff tensions began to settle.

This week, February’s CPI and January’s PCE price index reports are due. An orderly release is expected, with headline inflation at 2.4% in January. Markets may nonetheless discount the figures, given the inflation risk the conflict has brought squarely into view. We expect the dollar to continue grinding higher this week, possibly testing the 100 line, as the lack of de-escalation leaves oil price upside largely uncapped.

EUR: Hawkish repricing ignites as inflation risks rise

EUR/USD held above 1.16 last week after shedding 1.6%, as the conflict continues to exert heavy selling pressure on the pair. Markets may have been hoping for swifter de‑escalation, especially after the US floated measures aimed at limiting disruptions to oil flows, including naval escorts and revisited tanker‑insurance arrangements. But the ferocious escalation is unlikely to give these proposals real traction, they are seen as temporary fixes that do little to offset broader safety concerns. Sub‑1.16 downside this week – as today’s session suggests – is therefore expected.

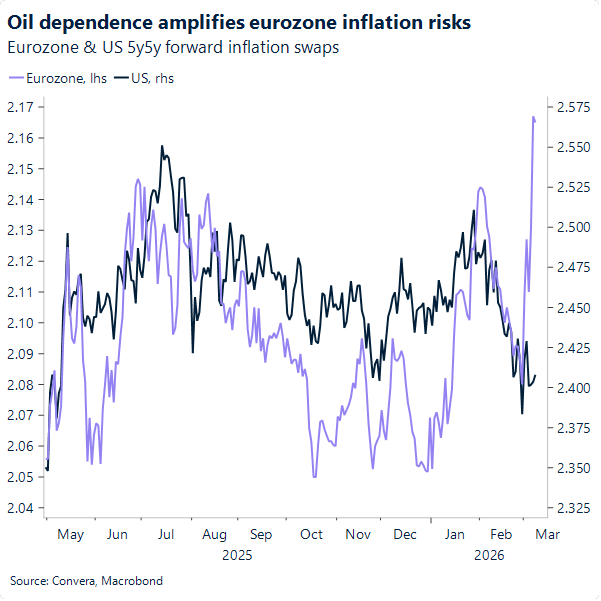

Against a backdrop of deep bearishness, EUR/USD rate differentials have turned more supportive for the common currency. Investors increasingly recognise that the eurozone is more likely than the US to import inflation from higher energy prices. The US still relies on Middle Eastern oil, but strong domestic production provides a meaningful buffer. Europe lacks that cushion, and its structural exposure leaves investors more concerned about the eurozone inflation outlook, which in turn triggers more aggressive hawkish repricing in euro rates.

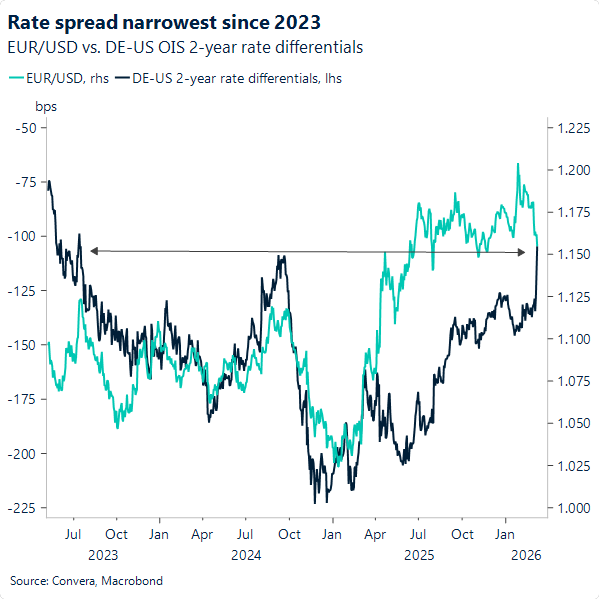

EUR/USD rate differentials are in fact now the narrowest since 2024, with markets pricing ~50 basis points of tightening by end-2026. The backdrop may offer medium‑term support for the euro, and perhaps more cleanly than for the US dollar (see USD section above). In the near term, though, unless clear signs of de‑escalation emerge, a sustained break below 1.16 looks warranted, with 1.15 the next level to watch.

On the data front, there isn’t much on the calendar this week – although we were just greeted with a disappointing German industrial production and orders prints, showing activity fell 1.2% y/y in January. That setback dents hopes for a much‑anticipated rebound – not this quarter at least – while the ongoing conflict poses a clear risk to any meaningful recovery materialising at all.

GBP: Stagflation fears are back on the agenda

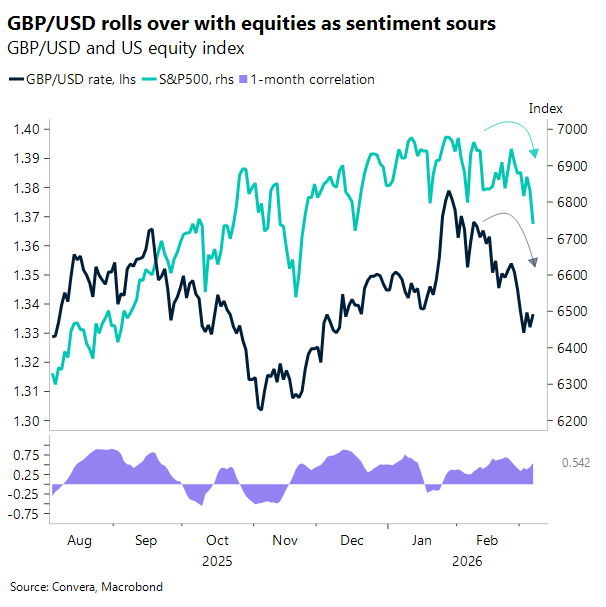

Sterling is trading in the cross‑currents of the latest Middle East shock, with FX markets digesting events through two dominant channels: a broad rise in global risk aversion and a sharp repricing in oil and gas. The configuration is uncomfortable for currencies like GBP given its sensitivity to higher US rates with meaningful exposure to weaker equity markets. It’s a mix that aligns uncomfortably well with a stagflation‑tilted backdrop.

Brent crude is now roughly 50% higher than when the Iran conflict began, and the longer the war drags on, the more entrenched these elevated price levels become relative to central banks’ assumptions. The UK may be less dependent on imported oil than the euro area, but the gilt market faces a tougher inflation profile. Eurozone inflation was well‑anchored heading into the conflict; the UK’s wasn’t. Headline CPI was expected to briefly hit target this spring, yet services inflation — the clearest gauge of domestic pressure — was still running at 4.4%. The ingredients are in place for UK inflation to rebound off its expected lows and potentially ignite a second‑round price spiral before the first one has fully faded.

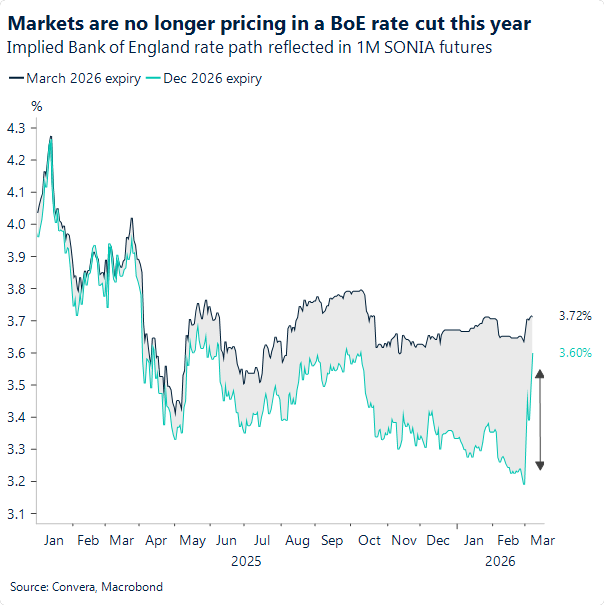

Markets are already adjusting. UK OIS has nearly priced out another BoE cut for 2026, and if energy‑driven inflation persists, the curve will eventually need to entertain the possibility of a hike — a scenario that would unsettle gilts and tighten financial conditions just as growth momentum softens.

This week’s domestic catalysts — Governor Bailey’s speech on Thursday and January GDP on Friday — matter, but they are secondary. For now, sterling’s path is being set by geopolitics, energy markets and the risk that the UK edges back toward a stagflationary mix that is rarely kind to the currency.

Market snapshot

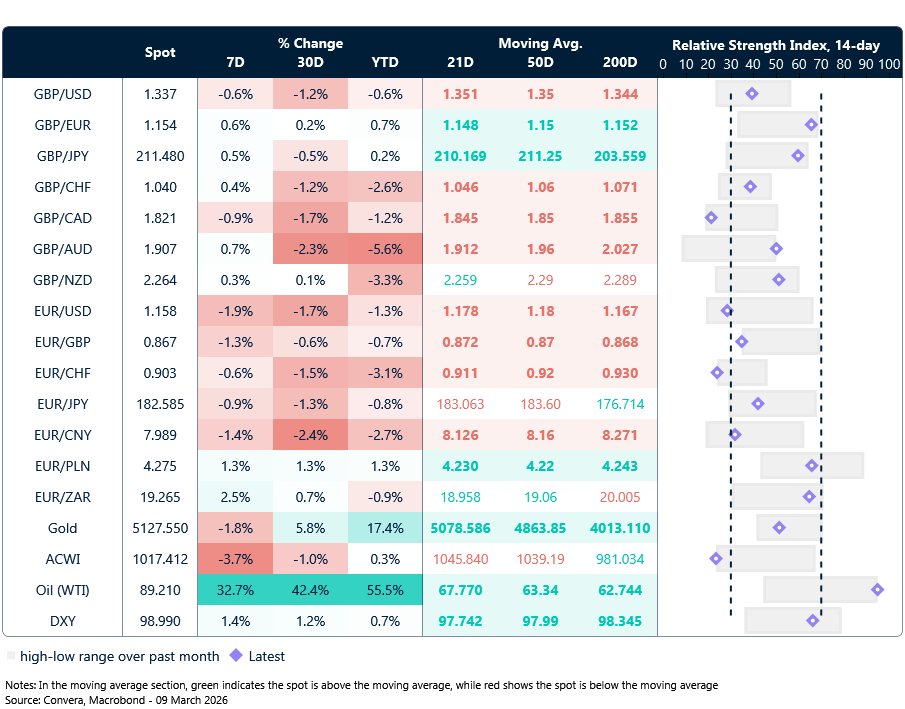

Table: Currency trends, trading ranges & technical indicators

Key global risk events

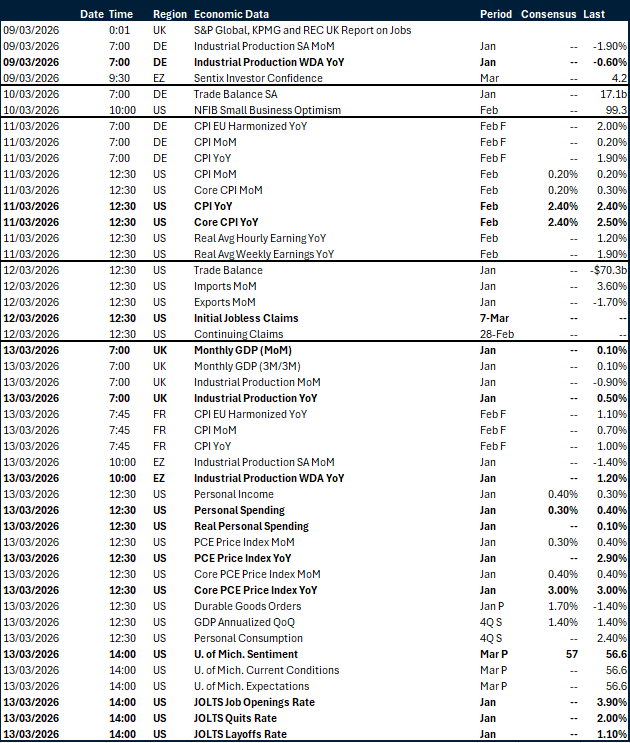

Calendar: March 9-13

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.