Dollar struggles to make headway

The US dollar started August on the front foot, rising against a basket of currencies, dragging EUR/USD under $1.10 and lifting USD/JPY beyond ¥143 for the first time in almost a month. The US dollar index usually appreciates in the month of August, with our seasonality study showing a modest 0.3% average rise when analysing the Augusts going back to 1971.

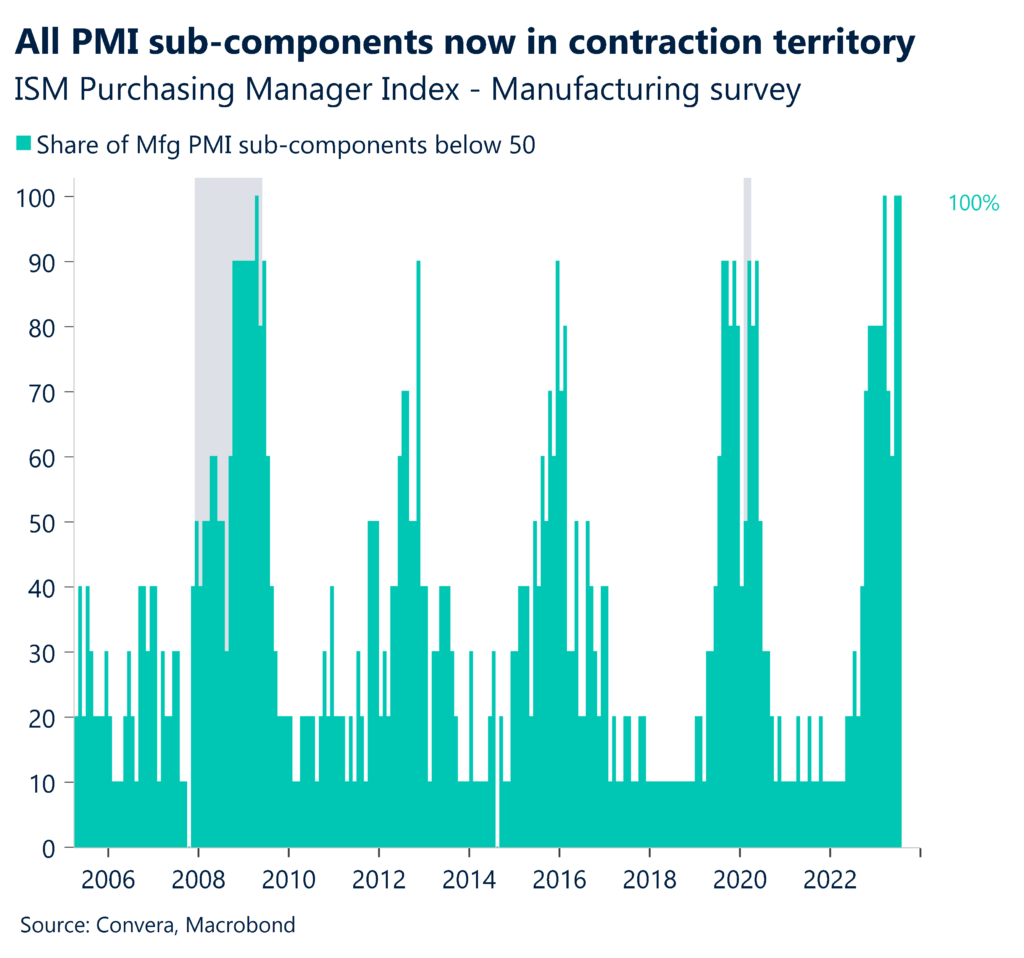

The dollar’s upbeat start to the new month, following its worst monthly performance in three in July, came to an sudden halt though after Fitch removed its top tier rating for US sovereign credit. The credit assessor downgraded the US to AA+ from AAA, due to the repeated debt limit standoffs and expected fiscal deterioration over the next three years. The controversial move was met with an angry response from the White House and surprised market participants, triggering a wave of demand for safe havens assets, particularly Gold and US Treasuries, whilst riskier assets, like equities, softened. Meanwhile, in the macro space, US job openings fell in June to 9.6 million, the lowest level since April 2021, but remained at levels consistent with tight labour market conditions. The ISM factory index contracted for a ninth straight month, and construction spending rose less than expected. Although there were signs that the US manufacturing sector might be stabilising amid the improvement in new orders, all sub-components of the ISM remain in contraction territory.

This is one reason why we are still in the camp that the US is headed for recession. The Fed’s Senior Loan Officer Opinion Survey (SLOOS) this week also showed banks are being increasingly restrictive in their lending practices while households and businesses are wary of taking on additional borrowing, adding to the credit squeeze and recession risk. However, we cannot rule out what a growing number of economists are conceding – that the US economy is headed for a soft landing, largely due to its resilient labour market.

Pound usually has an awful August

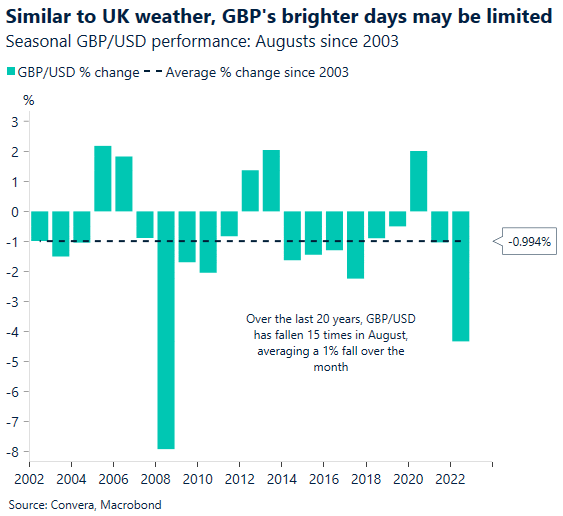

August has kicked off on a sombre note for the pound, particularly against US dollar, but looking back at the past 20 years, this may not come as a big surprise. Seasonality trends show that GBP/USD tends to fall in August, and since 2003 the average decline has been about 1%.

One of the world’s most traded currency pairs just notched its eighth monthly gain in ten and climbed 3.2% through June and July, rising as high as 6.3% from its June low of $1.2366 to its July high of $1.3144, a 16-month peak. After ending its longest ever stint below $1.30 though, the pound failed to hold its grip on this key psychological level, slipping back towards $1.28, and closing below a long-term upward sloping trendline yesterday. Final July PMI prints published yesterday revealed shrinking factory activity in the UK, whilst house prices slumped at the fastest pace since 2009, under pressure from higher interest rates. This knocked sterling ahead of the Bank of England’s (BoE) policy decision on Thursday. Money market pricing attaches a 60% probability of a 25-basis point rate hike by the BoE and a modest 40% chance of a 50-basis point hike. Given the incoming UK economic data of late (cooling inflation and weaker economic activity) the smaller hike appears most likely, but strong wage growth and second-round inflation effects means a larger hike cannot be ruled out.

But how will the pound react? Higher interest rates usually benefit a currency, but the pound has mostly weakened in the aftermath of each BoE rate hike during this tightening cycle. Moreover, while seasonality should not be used in isolation, it can be helpful in gauging where the path of least resistance may be, and that path tends to be lower in August.

Global manufacturing recession continues

Global risk sentiment took a dive at the weekly open yesterday, following weaker than expected manufacturing data out of Europe and China. The Stoxx 600 fell by the most in a single day (-0.9%) in more than a month with the euro struggling to get back up above the important $1.10 mark. As no important data releases are scheduled for the Eurozone today, market drivers will come from elsewhere.

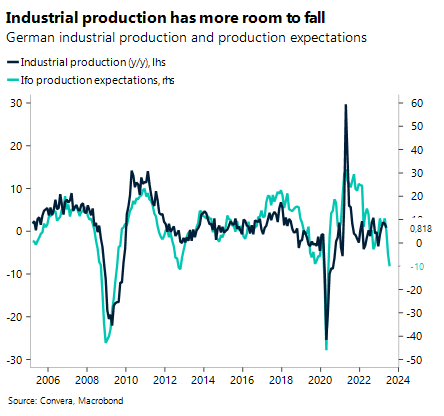

The global manufacturing sector remains pressured by high interest rates, falling pricing power and weak demand. The Eurozone factory activity contracted by the most since the onset of the pandemic in July, with the purchasing manager index falling to 42.7 from the previous 43.4. The composite PMI is expected to be released on Thursday. However, with the recent trend of the weakening services sector, the overall index might trend lower as well. The ugly outlier in the data was once again Europe’s largest economy. Germanys PMI tumbled to below 40 in June, recording the largest monthly contraction since May 2020.

The next important data releases will be German new orders on Friday and industrial production on Monday. For the latter, we are currently forecasting a stronger fall compared to consensus (-0.4% vs. -0.3%) as most leading survey indicators point to weakness in June. EUR/USD had fallen in yesterday’s trading but bounced following the credit downgrade of the US by Fitch, highlighting how the currency pair is driven by factors not limited to the Eurozone.

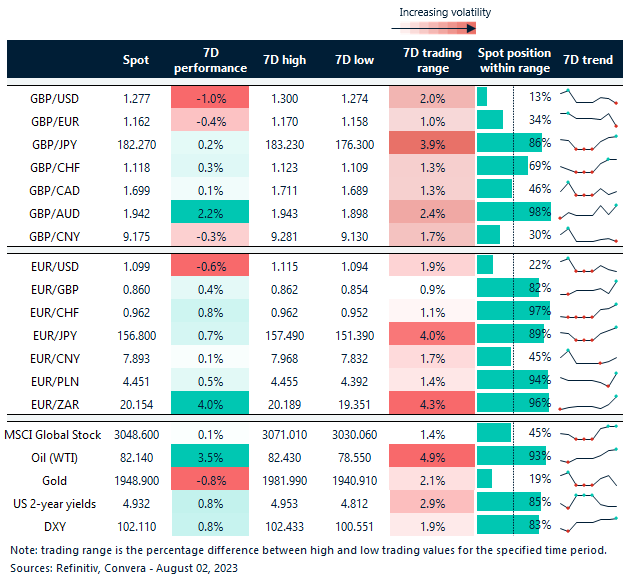

Cable falls 1% in a week

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: July 31- August 4

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.