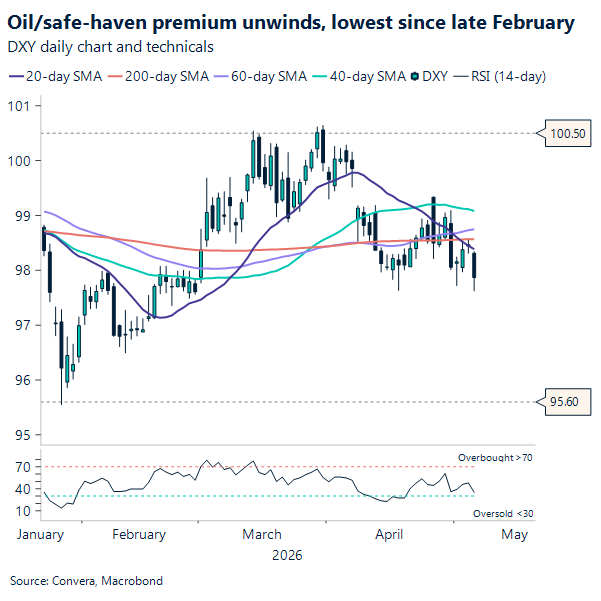

USD: Geopolitical tensions ease, risk rally continues

Markets opening point to a continuation of the risk-rally seen in April as optimism takes hold. WTI oil prices have fallen to $92 a barrel while the dollar reached an eleven-week low. The move follows reports that the US and Iran are nearing an agreement to end their conflict. Consequently, the USD DXY Index has trade closer to levels seen before the February tensions began.

Iran is currently reviewing a new one-page memorandum from Washington to resolve the standoff. This proposal outlines a gradual reopening of the Strait of Hormuz and the removal of American blockades on Iranian ports. Furthermore, the plan requires Iran to pause nuclear enrichment while both sides negotiate a permanent deal later. These developments have helped push Brent crude prices significantly lower.

These headlines provide a fresh jolt of adrenaline for global risk assets today. Investors expect chipmakers and AI stocks to lead the way as the narrative shifts toward stability. In addition, emerging markets FX are seeing significant gains especially for oil importing nations like Mexico. This newfound positive sentiment suggests that a more stable market environment could return to finally stay, as many were expecting since the ceasefire was declared back in early April

On the macro side, US companies added a solid 109,000 jobs in April providing further evidence of a stabilizing labor market. This private sector growth follows a revised 61,000 advance in the prior month according to recent ADP Research. While the results came in lower than the 120,000 increase expected by economists the trend remains positive. It is important to remember that ADP data rarely predicts the outcome of the later NFP report accurately.

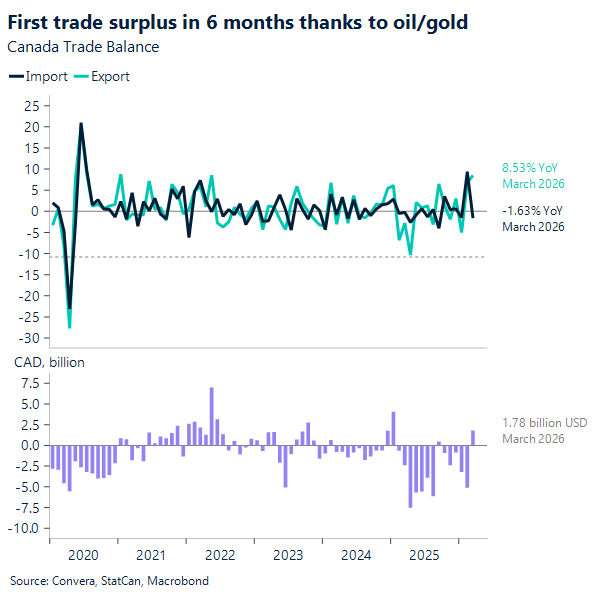

CAD: Canada trade swings positive

Statistics Canada released the international trade balance figures for the month of March. Canada posted a C$1.78bn merchandise trade surplus in March, a sharp turnaround driven by higher energy prices and a surge in gold shipments. Exports jumped 8.5% to C$72.8bn, the second-highest level on record, while imports fell 1.6%. That shift pushed the trade balance from a sizable deficit in February to the first surplus since September 2025.

The export story was largely about prices rather than volumes. Energy exports rose 15.6% as crude prices climbed amid Middle East tensions, while metal and mineral exports surged 24%, led by strong gold shipments to the UK. Strip out energy and metals, and export growth was far more modest, underscoring how concentrated the gains were.

Trade dynamics also improved geographically. Canada’s surplus with the U.S. widened to C$7.1bn as exports rose and imports eased, while the deficit with other trading partners narrowed to the smallest since early 2021. Still, with quarterly volumes telling a softer story, March looks more like a favourable price shock than a step-change in underlying growth.

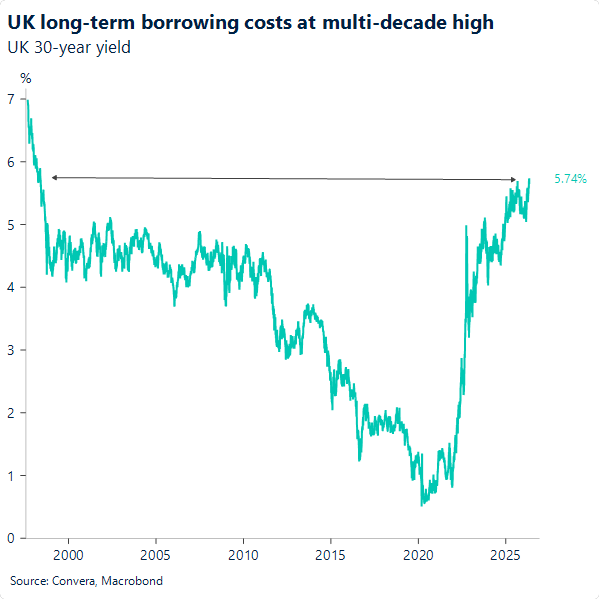

GBP: UK risk premium builds

UK bonds sold off across the curve yesterday as they caught up with moves in peer markets following Monday’s Bank Holiday closure, amid renewed tensions in the Middle East. There is more to the move, however. With UK local elections approaching on Thursday, a domestic risk premium is also contributing to higher yields, particularly at the long end, where the 30‑year yield reached its highest level since 1998.

Nonetheless, sterling managed to hold on to its daily gains, suggesting markets may have grown more tolerant of higher yields. Even in normal times, elevated gilt term premia tend to reflect increased fiscal risk relative to peers such as the US and the euro area. At the same time, markets have had time to price in a degree of political instability in the UK, effectively raising the bar for more meaningful sterling sell‑offs, despite the elevated yield environment. This tolerance is further underpinned by rising Bank of England hiking expectations, with markets now pricing in three quarter‑point rate hikes this year, up from two last week, thereby keeping sterling’s carry appeal intact. Together, these factors have cushioned sterling against immediate downside, though they may also be laying the groundwork for more pronounced bearish pressure over the medium term.

Ultimately, backlash against Keir Starmer’s leadership has been largely sidelined since the escalation of the conflict in the Middle East, masking the full implications of an increasingly hawkish Bank of England. Thursday’s election results could serve as the catalyst that brings these strands together: a significant defeat would further undermine confidence in the government’s self‑imposed fiscal rules at a time of fragile economic growth and rising conflict‑driven inflation pressures. In such a scenario, a hawkish BoE could become increasingly unfriendly for sterling, as markets may begin to interpret further tightening as exacerbating the macro backdrop, ultimately adding to strains on public finances.

That said, expectations for a worse‑case outcome appear quite entrenched, effectively widening the scope for “positive” surprises from the election result. A less‑severe outcome would likely postpone the sterling‑negative shift in market interpretation outlined above, while keeping sterling’s carry appeal intact, provided rate volatility is not reignited by a material geopolitical re‑escalation. In a scenario where political turmoil remains relatively contained following a benign outcome, we would continue to favour a mildly bullish bias on sterling.

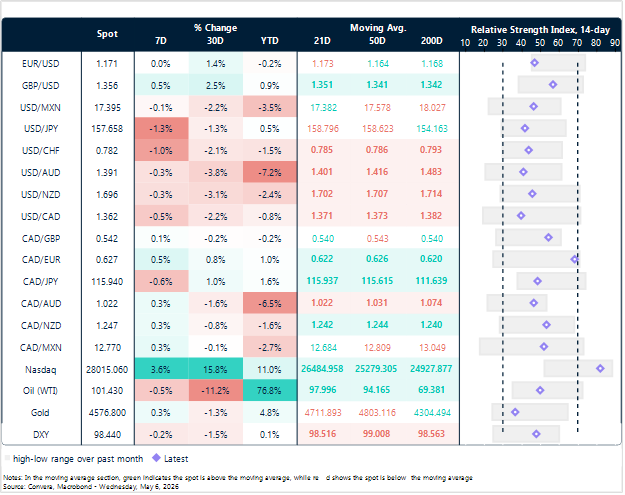

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

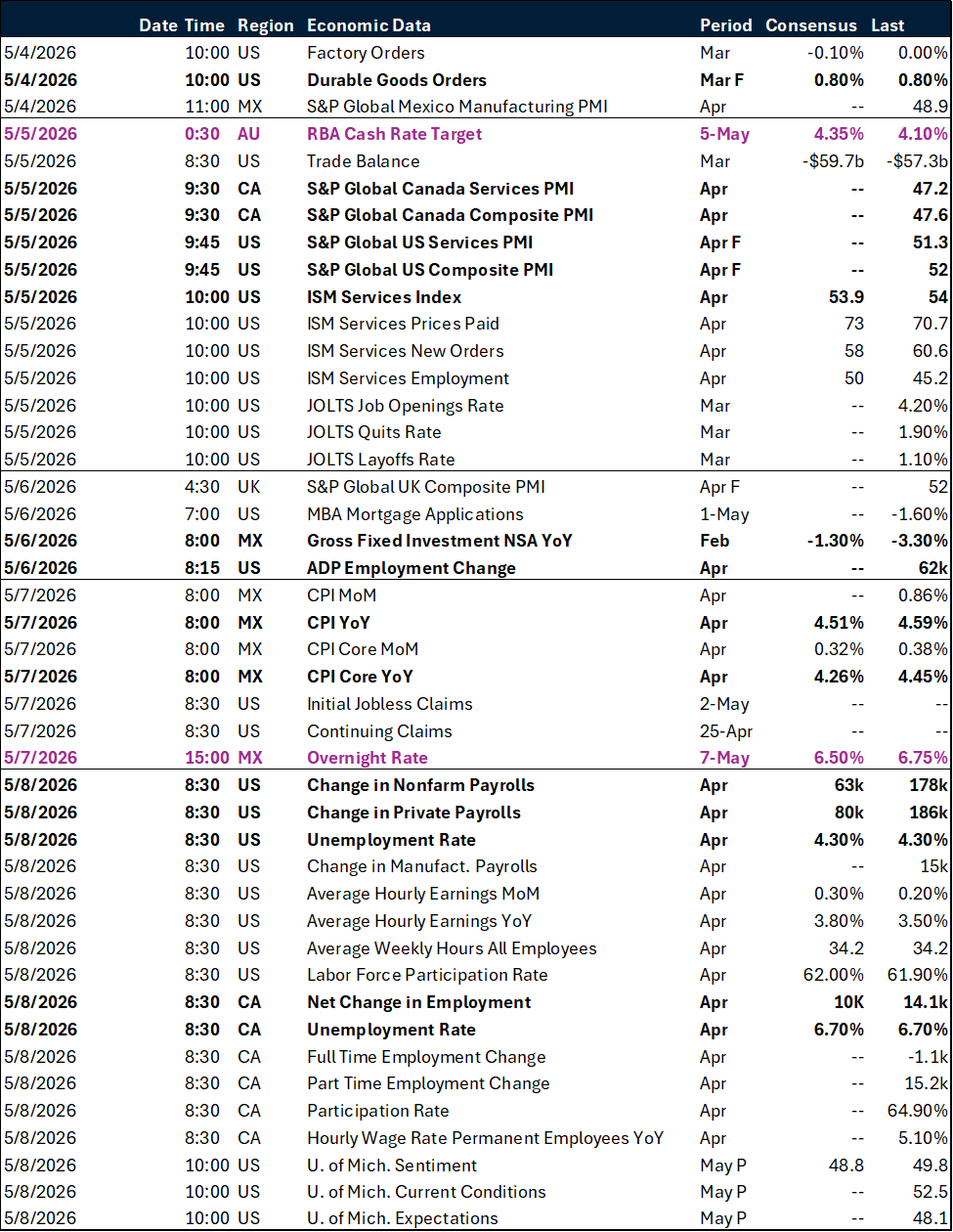

Calendar: May 04 – 08

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.