Written by Convera’s Market Insights team

US economy slows but inflation jumps

Boris Kovacevic – Global Macro Strategist

Global markets jolted yesterday with equities tumbling, bond yields rising and the US dollar index rebounding before then reversing to hit fresh 2-week lows. USD/JPY, however, has hit a new 34-year high. Investors winced at the double whammy of a significant miss in the first quarter US GDP print coupled with a significant beat in the core PCE inflation print. US 10-year yields rose to the highest since early November as traders pushed back the timing of the first Federal Reserve (Fed) rate cut until December and priced in around 33 basis points of cuts by year-end, down from over 40 at the start of the week.

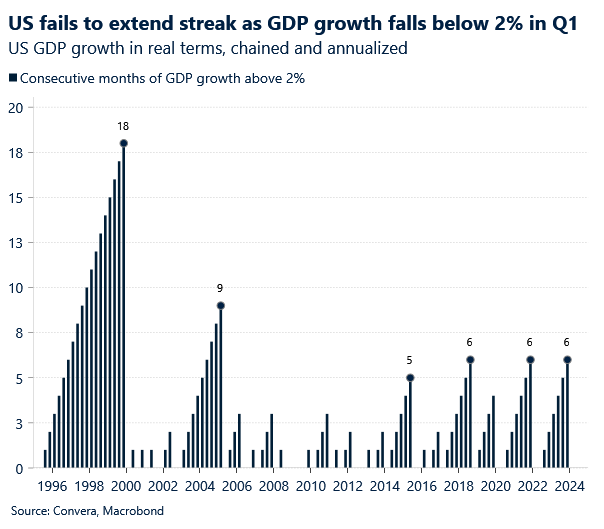

The hard (lagging) data continues to come in strong in the US, as the country closes out the first quarter on a positive note. However, the upside surprises on retail sales, industrial production, inflation, and durable goods did not culminate into a strong GDP print. The US economy failed to extend its positive streak to seven consecutive months of above 2% growth, which would have been the longest in 19 years. Instead, US activity expanded by 1.6% in the three months till March. However, the price component (PCE) came in much hotter than expected, beating the 3.4% estimate with a 3.7% growth rate – the highest since the early 1990s excluding the pandemic years. This confirms our thesis of US exceptionalism having peaked in light of the recent PMI, NFIB and GDP prints and that inflation is stickier than expected.

The US currency has ignored the deterioration of leading indicators, which have been responsible for lifting implied recession probabilities higher in recent times. Going forward, it seems more likely that US growth will moderate and converge back to the soft data given the current duration of US outperformance. Thus, the USD might lose its high growth position over the coming quarters and if inflation eventually starts cooling as well, the Fed could cut interest rates more than currently priced in by year end, further weakening the dollar. The next key risk event ahead of the Fed meeting and jobs data next week, is today’s monthly PCE print.

Pound mixed as consumer morale improves

George Vessey – Lead FX Strategist

Despite pulling back from a fresh 1-week high above $1.25 yesterday, GBP/USD is still primed to register its biggest weekly gain in seven. More balanced commentary this week from Bank of England (BoE) policymakers, coupled with the a slew of stronger-than-expected UK economic data, including consumer confidence this morning, have helped support sterling across the board.

The GfK consumer confidence indicator in the UK rose to a higher-than-expected -19 in April from -21 in March. The overall index has been bouncing between -24 and -19 for the last six months, indicating slow progress as economic uncertainties weighed heavily. However, despite the recent rise in the UK unemployment rate to a 6-month high, the UK inflation rate has fallen from near 9% to near 3% in a year, which has seen the UK Misery Index (unemployment + inflation) fall to its lowest level since 2021. Consumer confidence has a strong correlation with the Misery Index, and we therefore expect morale to keep improving, especially once the BoE starts cutting interest rates.

Markets continue to price in just 40 basis point of rate cuts by the BoE this year, with the first move expected in August. We wouldn’t be surprised to see a June cut though and 75 basis points of cuts in total this year, which is likely to limit any GBP upside due to unfavourable yield differentials. Nevertheless, absent any intervention from Japanese officials, GBP/JPY may continue stretching to new 2015 highs. The Bank of Japan left rates unchanged this morning after Japanese inflation unexpectedly fell, hitting the yen across the board.

Stars align for German recovery

Ruta Prieskienyte – FX Strategist

The euro managed to hold above $1.07, a 2-week high, despite heightened intraday volatility threatening to extinguish recovery momentum as the latest US data reinforced the belief that the Fed will keep rates higher for longer. Upbeat Eurozone sentiment data and hawkish statements from ECB policymakers kept the common currency supported. Although an ECB June rate cut is most likely a sealed deal, the rate path in H2 remains highly contested. ECB’s Nagel said that services inflation remains high and until inflation fell in a sustainable manner, he could not pre-commit to a particular rate path. His views were echoed by other ECB officials, namely Schnabel and Muller, who said he was not comfortable committing to “back-to-back cuts”. Market implied cumulative rate cut expectations dropped to 66bps (-8bps) by year end, while front end expectations remain largely stable.

On the macro front, a string of business surveys this week are suggesting that Germany may be tentatively bouncing back. The forward looking Gfk consumer confidence index rose to -24.2 – its highest level since May 2022, beating market expectations. The stronger increase in consumer sentiment was mainly due to a boost in income expectations. Rising wages and salaries combined with a recent decline in the inflation improves real purchasing power among households, leading to increased willingness to spend. While overall sentiment has improved, it remains at a subdued level, with a sustained economic recovery still sometime away. Earlier this week, the German government published forecasts expect the economy to grow just 0.3% in 2024. For now, upbeat macro data acts as a support function for the euro currency, as the focus remains firmly on the monetary policy developments.

In FX options market, EUR/USD overnight implied volatility, a gauge of expected realised volatility, rose above 9% as traders position ahead of US core PCE print today. EUR/USD 1-month. EUR/USD 1-week 25 delta risk reversal rises to 0.23% in favour of euro puts, suggesting markets are positioning to protect against further euro downside in the short term.

Yen extends declines after BoJ holds rates steady

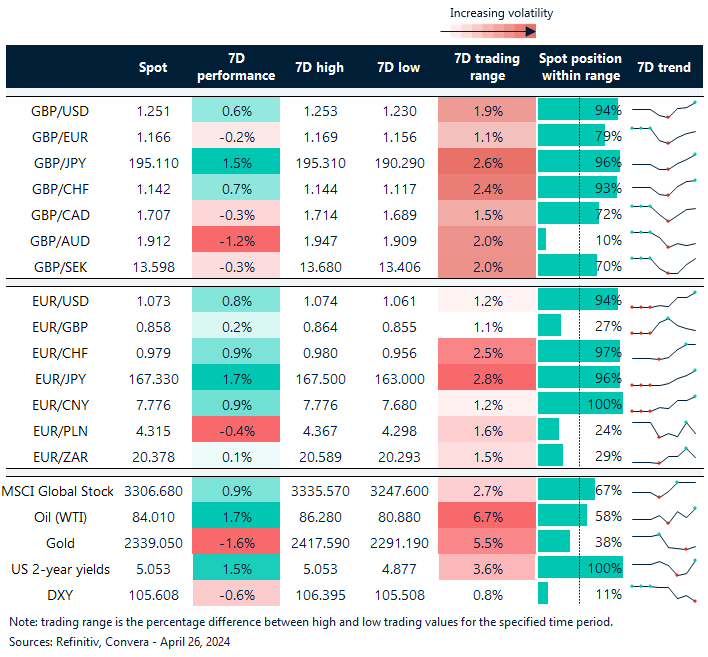

Table: 7-day currency trends and trading ranges

Key global risk events

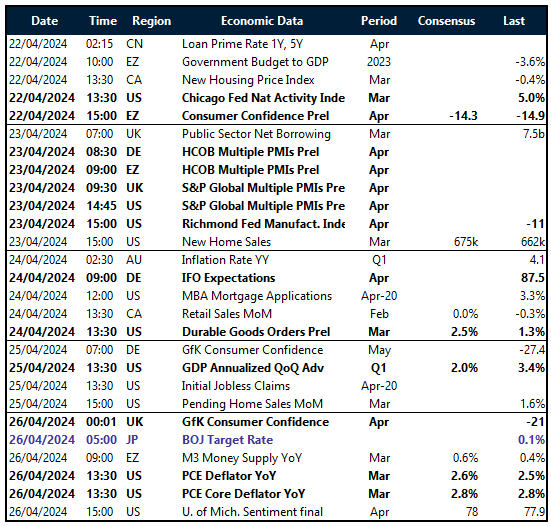

Calendar: April 22-26

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.